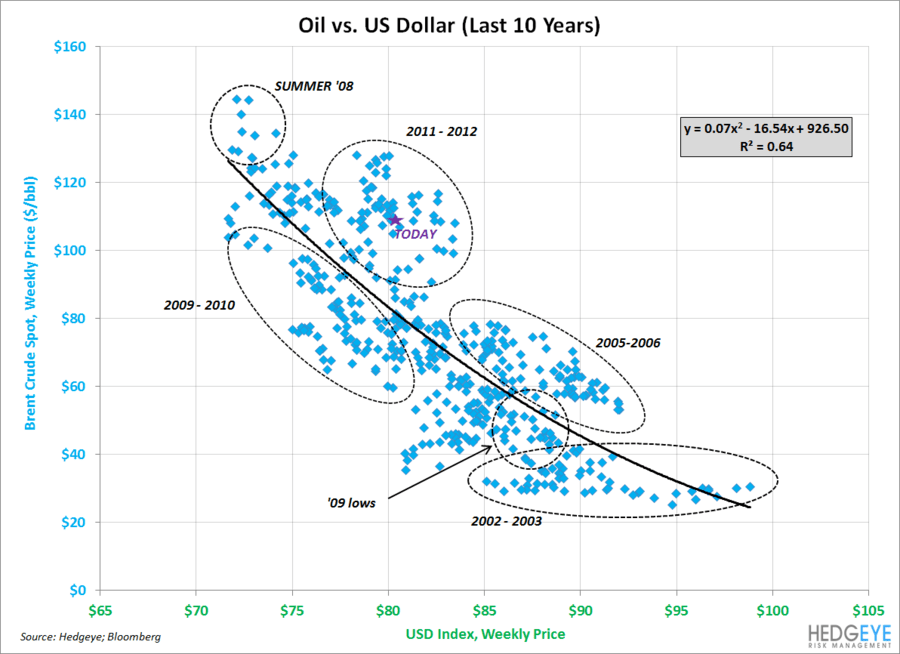

We’ve said it before and we’ll say it again: a Romney win is bullish for the US dollar. Dollar up, commodities down; that puts pressure on crude oil and will drive it lower accordingly. The inverse correlation between the US dollar and Brent crude oil has strengthened to -0.82 over the last 15 days versus +0.27 over the last 60 days. On the long-term scale of things, the relationship has legs. It all comes down to who takes the White House at the end of today.