This note was originally published November 06, 2012 at 08:43 in Early Look

“The Democracy will cease to exist when you take away from those who are willing to work and give to those who are not.”

-Thomas Jefferson

Game day is here. In what will likely go down as the most expensive campaign season in history, it has all come down to today. For partisans on both sides, the quote above from Thomas Jefferson is what this election has been about: should the government do less or more? Based on the current national polls, it is not clear either side really won that argument.

As I wrote yesterday in a note, the consensus view of the expert pollster is that President Obama has this election won. He currently leads, albeit very slightly, in the national polls and he has a slightly higher edge in the swing state polls which should give him the Electoral College votes he needs to win. This is all reflected in the probability markets as websites like Intrade have Obama at an almost 68% probability of winning.

Now, if I were content in believing the national polls, I could probably stop the note here and get on to something more interesting, like telling you that you should dial into our call with Neil Barofsky, the former Inspector General of TARP, tomorrow morning (if you don’t have the dial-in information ping sales@hedgeye.com). The key pushback on the story the polls are telling us is that almost all economic models suggest that President Obama should not get re-elected. These models, like polls, also have a very strong track record predicting Presidential election results.

In addition, the polls generally appear to show a much higher sample of Democrats by ID than would be expected in a race this close. This doesn’t mean the polls are wrong, of course, it may well mean there is a reason more people are indentifying as Democrats than ever before. Currently, it is a margin of +7 for Democrats in the recent national polls that I reviewed. It could also be a systemic error, which may give Romney the ultimate edge.

Regardless, by tomorrow we will know who is right and wrong in terms or predicting the outcome of the election. We will also know who is going to be the President for the next four years. Or will we? This year more than other, there is also a strong case for an outcome that is undecided on Election Day.

Specifically, in Ohio voters that have requested ballots to vote early, can also go to the polls on Election Day and vote. In this scenario, the Ohio voters would be given provisional ballots that could not be counted for ten days until it was determined that voter had not voted twice. In Ohio, a recount is triggered if the vote is within 0.5% and then the recount would have to wait ten days for the provisional ballots to be legitimized.

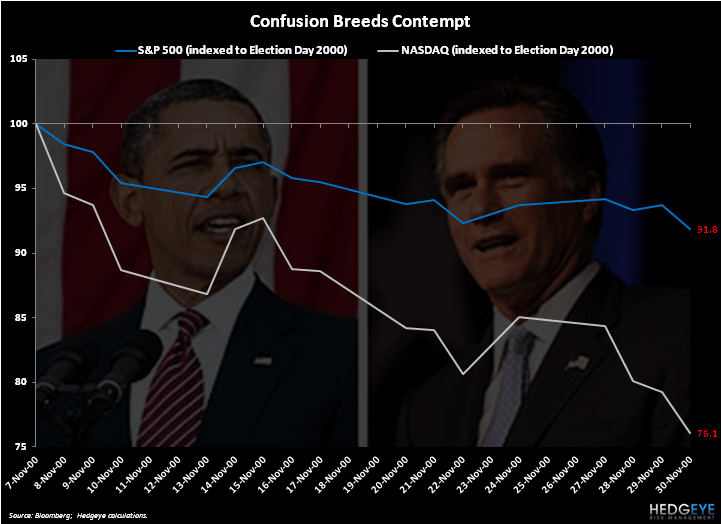

In the Chart of the Day we take a look at how the market performed in the days following the 2000 tied election. It wasn’t pretty to say the least. There was a meaningful drawdown for most of November to the tune of some -8% in the SP500. As my colleague Keith McCullough noted on CNBC last night, it was a market that felt like hell. Indecision is never good for equity markets.

Undoubtedly, many of you will be watching the returns very closely this evening. There are a few things that you want to focus on to get a sense for the eventual outcome of the election. These are as follows:

1) Turnout - If turnout is bigger than expected, it likely favors Obama. If it is lower than expected, it likely favors Romney. Potential rain in both North Carolina and Florida may help Romney. In 2008, more than 131 million people voted. This equated to 62.9% of eligible voters casting ballots, if the turnout percentage looks to be coming in lower it will be an edge for Romney.

2) Exit polls – There are certain demographics that Romney does much better with, namely whites and males. If the exit polls show a high turnout among these groups, this will be a positive for Romney. The inverse is true for Obama. A high turnout of women and ethnic minorities favors Obama.

3) Virginia – The polls in Virginia close at 7pm eastern. The path to Ohio even mattering and an eventual victory for Romney goes through Virginia. If Romney does not win Virginia, he most certainly will not win the Presidency.

4) Ohio - As I’ve written before, no Republican nominee has ever won the Presidency without winning Ohio. While there is a path to the Presidency for Romney without Ohio, it is very unlikely. The key counties to watch in Ohio are Hamilton (Obama won in 2004, but normally goes Republican), Wood and Ottawa. The last two are the swing votes within the swing state and have gone with the Presidential winner every year since 1992. North Carolina closes at 730pm, just like Ohio, and is must win for Romney.

5) 8pm – Three states close at 8pm, including New Hampshire and Florida. If Romney looks to have won North Carolina, Virginia and Ohio, he will likely have also won Florida, but still needs more Electoral College votes. New Hampshire has four and would put him over the top.

6) 9pm – If Romney is still alive at 9pm, then we are on to 14 states, including crucial battlegrounds Colorado and Wisconsin. Democrats have won Wisconsin for six straight elections. If Romney can keep Wisconsin close or flip it, he will likely be the next President.

In closing, I will leave you with a quote from Thoreau:

“All voting is a sort of gaming, like checkers or back gammon, with a slight moral tinge to it, a playing with right and wrong, with moral questions; and betting naturally accompanies it. The character of the voters is not staked. I cast my vote, perchance, as I think right; but I am not vitally concerned that that right should prevail. I am willing to leave it to the majority.”

Indeed.

Our immediate-term risk range for Gold, Oil (Brent), Copper, US Dollar, EUR/USD, UST 10yr Yield, and the SP500 are now $1678-1705, $106.03-110.12, $3.45-3.53, $80.19-80.84, $1.27-1.29, 1.67-1.75%, and 1401-1432, respectively.

Keep your head up, stick on the ice and put your ballot in the box,

Daryl G. Jones

Director of Research