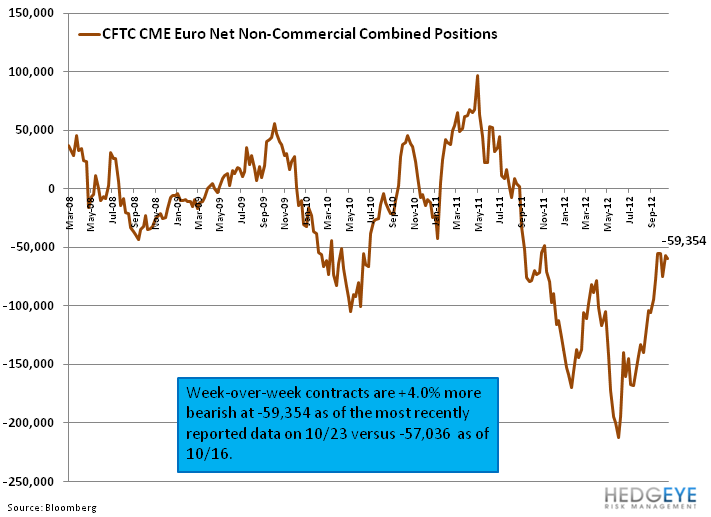

-- For specific questions on anything Europe, please contact me at to set up a call.

Positions in Europe: Long German Bonds (BUNL)

Asset Class Performance:

- Equities: The STOXX Europe 600 closed up +1.6% week-over-week vs -1.3% last week. Top performers: Ukraine +6.3%; Austria +3.8%; Spain +2.5%; Netherlands +2.5%; Finland +2.5%; Ireland +2.2%; Hungary +2.2%; Germany +1.8%. Bottom performers: Cyprus -8.6%; Greece -8.3%; Slovakia -1.4%. [Other: France +1.7%; UK +1.1%].

- FX: The EUR/USD is down -0.80% week-over-week. W/W Divergences:NOK/EUR +1.45%; TRY/EUR +1.25%; SEK/EUR +0.74%; GBP/EUR +0.25%; CHF/EUR +0.16%; HUF/EUR +0.04%; DKK/EUR 0.00%; CZK/EUR -1.24%.

- Fixed Income: The 10YR yield for sovereigns were mixed week-on-week. Greece rose the most at +100bps to 18.21%, followed by Portugal +31bps to 8.35%. Spain and Germany both declined by -7bps to 5.60% and 1.45%, respectively. France fell -2bps to 2.22% and Italy declined -1bp to 4.92%.

Data Slumps:

This week it’s worth noting that despite signals from some analysts of “green shoots” and optimism that the Eurozone will find a path forward, the data continues to indicate that the Eurozone has not found a bottom. A look at the PMI Manufacturing figures out this week (Services come out next week and may be slightly higher) indicate levels that are both comfortably below the 50 line indicating contraction and sequentially lower (especially) for the core countries in OCT versus SEPT.

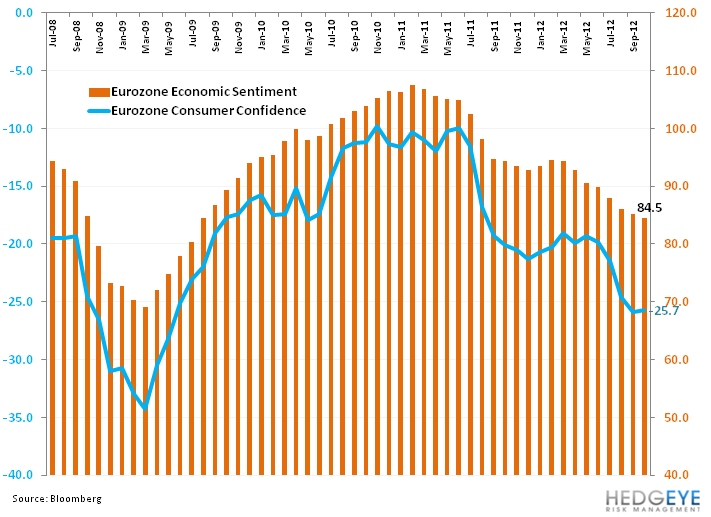

Eurozone Confidence figures showed a similar negative trend, namely declining for a seventh straight month in the October figures. Given that the largest business and trade partners for European countries are their fellow neighbors, we do not expect one country to sustain a positive growth inflection until the entire region starts to see improvement. That said, Germany remains the “best of the rest” and we currently have a Real-Time position in BUNL to take advantage of this relative strength.

The European Week Ahead:

Monday: Nov. Eurozone Sentix Investor Confidence; Oct. UK PMI Services, Official Reserves, BRC Sales Like-For-Like; Oct. Spain Unemployment

Tuesday: Oct. Eurozone PMI Composite and Services - Final; Sep. Eurozone PPI; Oct. Germany PMI Services - Final; Sep. Germany Factory Orders; Oct. UK NIESR GDP, BRC Shop Price Index, New Car Registration; Sep. Germany Industrial Production, Manufacturing Production; Oct. France PMI Services – Final; Spain Services PMI; Oct. Italy PMI Services

Wednesday: Sep. Eurozone Retail Sales; Oct. Germany Wholesale Price Index (Nov. 7-12); Sep. Germany Industrial Production; Sep. Spain Industrial Output

Thursday: ECB Governing Council Meeting; ECB Announces Interest Rates; AFME 7th Annual European Bond Conference in Brussels; Nov. Eurzone Asset Purchase Target; Sep. Germany Exports, Imports, Current Account, Trade Balance; BoE Announces Rates; UK Asset Purchase Target; Nov. UK Bloomberg Economic Survey; Sep. France Trade Balance; Aug. Greece Unemployment Rate

Friday: Oct. Germany Consumer Price Index – Final; Sep. UK Total Trade Balance; Oct. BoF Business Sentiment; Sep. France Industrial Production, Central Government Balance, Manufacturing Production; Sep. Italy Industrial Production; Oct. Greece Consumer Price Index; Sep. Greece Industrial Production

Extended Calendar:

NOV 12 – Eurogroup Meeting in Brussels

NOV 15 – Catalonia regional election in Spain

NOV 22 – ECB Governing Council Meeting

NOV 27 – AFME 4th Annual Spanish Funding Conference in Madrid

DEC 1 – Beginning of the Russian Presidency of G20

DEC 3 – Eurogroup Meeting in Brussels

DEC 6 – ECB Governing Council Meeting

DEC 12-13 – First public consultation between the Russian government, B20 Coalition and international civil society representatives on G20 agenda for 2013 (in Moscow)

DEC 20 – ECB Governing and General Council Meeting

APR 2013 – Parliamentary elections in Italy

MAY 2013 – Presidential elections in Italy

Call Outs:

Greece - Kathimerini discussed how Greece's ruling coalition faces an extremely tense next few days ahead of two key votes in parliament next week. The article highlighted concerns about the rising dissent in the Pasok party that could leave the coalition without sufficient support to pass the austerity and reform measures demanded by the troika. It noted that Prime Minister Samaras is due to meet with his 127 deputies on Monday, ahead of the vote on structural reforms on Wednesday and the vote on the 2013 budget, which will be held at midnight on Sunday, 11-Nov (just ahead of the 12-Nov Eurogroup meeting during which a final decision on Greece is expected).

Italy – Over the weekend former Prime Minister Berlusconi threatened to bring down the technocratic government led by Prime Minister Monti via a no-confidence vote from his People of Liberty party (PDL), the biggest in parliament. Berlusconi noted that, "We have to recognize the fact that the initiative of this government is a continuation of a spiral of recession for our economy. Together with my collaborators we will decide in the next few days whether it is better to immediately withdraw our confidence in this government or keep it, given the elections that are scheduled." While a no-confidence vote would likely force early actions, there were also thoughts that Berlusconi may no longer have enough support within the PDL to bring down the government.

Ireland - Germany has signaled that it is open to a restructuring of the €30B Anglo Irish Bank promissory note to improve the sustainability of Ireland’s adjustment program (rather than tapping the ESM).

Spain - Spain's northern region of Cantabria on Monday became the ninth region to request a credit line, recently established by the central government to cover liquidity needs. It said it would tap the €18B fund for €137M. Recall that other regions have already tapped the credit line for close to €17B.

Greece - Greek 2013 Govt Debt/GDP at 189.1% vs 175.6% in 2012, according to revised Greek Budget.

Netherlands - The incoming Dutch finance minister said on Thursday that “We have agreed to a tight budget and together we are going to implement it. It is a tough package that is going to require sacrifices from everyone in the Netherlands. I see it as my job to keep the finances on the right path.” The government has already agreed to nearly 16 billion euros ($21 billion) in budget cuts.

Slovakia - Prime Minister Robert Fico said on Wednesday that the state will return to having a single, state-run health insurance system and nationalize two private insurers.. "The government that I head rejects the notion of private health insurers making profits from taking public money and then using those profits to realize their ideas of a luxurious lifestyle," Mr. Fico told reporters, saying the newly unified insurance system would be in place by 2014.

Data Dump:

Eurozone CPI Est 2.5% OCT Y/Y vs 2.6% September

Eurozone Unemployment Rate 11.6% SEPT vs 11.5% AUG

Germany Retail Sales -3.1% SEPT Y/Y (exp. -1.1%) vs -1.1% AUG

Germany CPI 2.1% OCT Prelim Y/Y (exp. 2.0%) vs 2.1% SEPT

Germany Unemployment Chg 20K OCT vs 12K SEPT

Germany Unemployment Rate 6.9% OCT vs 6.9% SEPT

UK GfK Consumer Confidence -30 OCT (exp. -28) vs -28 SEPT

UK Nationwide House Prices -0.9% OCT Y/Y vs -1.4% September

UK Construction PMI 50.9 OCT vs 49.5 September

UK M4 Money Supply -3.5% SEPT Y/Y vs -4.0% AUG

France Producer Prices 2.9% SEPT Y/Y vs 2.8% AUG

France Consumer Spending -0.3% SEPT Y/Y vs -0.6% AUG

Italy CPI 2.8% OCT Prelim Y/Y vs 3.4% SEPT

Italy Unemployment Rate 10.8% SEPT Prelim vs 10.6% AUG

Spain Total Housing Permits -31.7% AUG Y/Y vs -37.1% JUL

Spain Q3 GDP Prelim -0.3% Q/Q (exp. -0.4%) vs -0.4% [-1.6% Y/Y (exp. -1.7%) vs -1.3%]

Spain CPI 3.5% OCT Y/Y Prelim vs 3.5% SEPT

Spain Retail Sales -12.6% SEPT Y/Y vs -2.0% AUG

Norway Unemployment Rate 3.1% AUG vs 3.0% JUL

Finland Business Confidence -11 OCT vs -8 September

Finland Consumer Confidence -1.6 OCT vs 3.4 September

Sweden Retail Sales 4.6% SEPT Y/Y vs 1.6% AUG

Belgium Unemployment Rate 7.4% SEPT vs 7.4% AUG

Belgium CPI 2.79% OCT vs 2.76% SEPT

Switzerland Retail Sales 5.4% SEPT Y/Y vs 6.0%

Switzerland UBS Consumption Indicator 1.07 SEPT vs 1.02 AUG

Austria PPI 0.7% SEPT Y/Y vs 1.0% AUG

Iceland Unemployment Rate 5.0% in Q3 vs 7.2% in Q2

Ireland Unemployment Rate 14.8% OCT vs 14.8% SEPT

Portugal Consumer Confidence -55.3 OCT vs -51.4 September

Portugal Economic Climate -4.6 OCT vs -4.2 SEPT

Portugal Retail Sales -5.7% SEPT Y/Y vs -6.1% AUG

Portugal Industrial Production -9.2% SEPT Y/Y vs -2.1% AUG

Greece Retail Sales -7.2% AUG Y/Y vs -8.0% JUL

Hungary Unemployment Rate 10.4% SEPT vs 10.4% AUG

Hungary Producer Prices 2.5% SEPT Y/Y vs 5.1% AUG

Romania PPI 6.6% SEPT Y/Y vs 7.2% AUG

Interest Rate Decisions:

(11/1) Czech Repo Rate Announcement CUT from 0.25% to 0.05%

(11/2) Romania Interest Rate Announcement UNCH at 5.25%

Matthew Hedrick

Senior Analyst