This morning’s Retail Sales are littered with one off company specific callouts and little by way of broader themes. For the second month in a row, a major retailer (KSS) is announcing that it will no longer participate in the monthly SSS exercise confirming its increasing irrelevance. Over the last two months, the exit of both TGT and KSS represents over 30% of last year’s SSS sample that has now withdrawn. With top-line results increasingly stressed, we expect additional defections in coming months.

All in October results came in marginally better than last month with 12 companies coming in ahead of expectations compared to 5 misses. Here are a few callouts worth noting:

- With retailers and consumers alike still trying to measure the impact of Sandy, few details were offered.

- The deviation of beats and misses were relatively tight with JWN and TJX the exception coming in well above expectations.

- At JWN, the Rack continues to succeed with comps up +10.5%

-

One of the more notable callouts is the deviation between TJX (beat) and ROST (miss) given persistent strength in the off-price channel.

- While momentum behind ROST has already started to fade, we expect today’s results to accelerate recent weakness.

- At TJX, Europe comps up +11% confirm favorable weather helping to drive sales overseas, which is key differentiator between the two off-pricers.

- KSS surprised to the upside after abysmal September results. In fact, when looking at the two months in aggregate, KSS’ hit its Q3 comp outlook. A notable outcome given weakness headed into quarter-end particularly given what have been very low expectations for the retailer and its inability to capitalize on share gifted from JCP. November results will be closely monitored re the sustainability of this improvement.

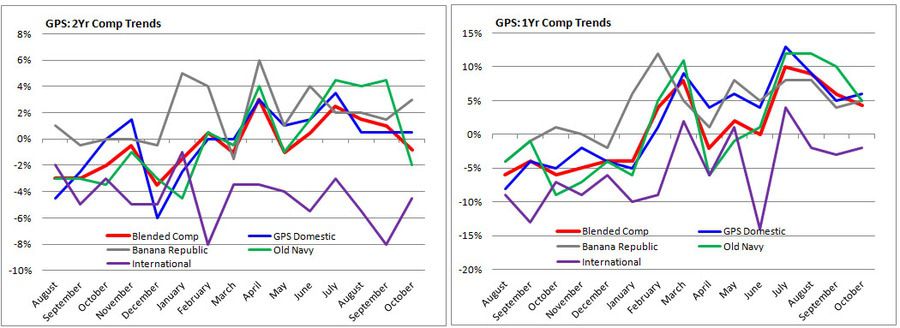

- GPS results will have investors focused on the ~10% EPS 3Q beat, but a look under the hood reveals a major slowdown at Old Navy despite the most favorable setup of the year. We think GPS’s upward trajectory is increasingly unsustainable. Old Navy and Gap Domestic have benefitted significantly from JCP. Now GPS has to anniversary it.

- TGT missed perpetuating what now marks three consecutive sequential months of decelerating underlying 2-year comp trends. With the setup getting tougher through year-end before it eases in early 2013, near-term results will remain pressured and reliant largely on cost management to drive earnings performance.

- With underperformance at both Old Navy and ROST, we will be keeping a close eye on this development as two of the greatest beneficiaries of JCP’s share shift…dare we say an incrementally positive data point for JCP?