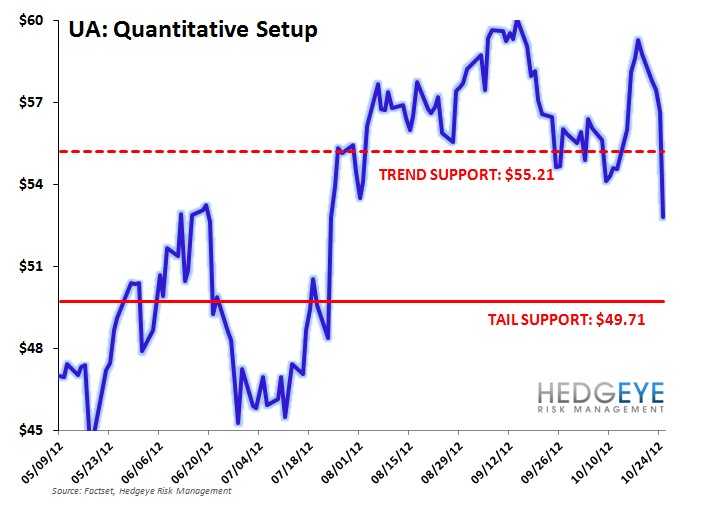

We agree with the market’s assessment of UA’s print, though we wouldn’t rush to cover the short just yet. There are always puts and takes with UnderArmour, but this quarter definitely gave the bears much more to chew on. The stock blew right through its TREND support, which puts the $49.71 TAIL line in play. But even then, we think that the risk is to the downside given the different characteristics of UA’s value creation. Specifically, UA’s multiple grew by 50% to about 38x over the past two years despite having problems with working capital/inventory management and gross margins. The single offsetting factor was sheer top line growth.

Now, we’re seeing the top line growth story slow down, with margins picking up the slack. That’s great. But unfortunately, the market won’t pay as much for margins as it will for top line. The top line shortfall in core apparel is particularly noteworthy, which we think is due largely to our concerns over pack-away inventories at retail, but it is also worth noting two other key factors.

1) Consumer direct revenue was up over 30% and now stands at 24% of sales. As this has grown, the impact on top line has been commensurate as UA booked the revenue as retail dollars as opposed to wholesale. Let’s look at the math this way DTC was 24% this year versus 22% a year ago. That amounts to $36mm incremental dollars. On an apples to apples basis, that amounts to roughly $18mm in wholesale dollars that would otherwise have been shipped at wholesale. This is 4 points of UA’s 23.6% top line growth rate for the quarter. Our point is not that we should rob them of this achievement. But rather that at 24%, the DTC ratio is not getting a whole heck of a lot higher if it expects to succeed in footwear and international markets. Any lack of a perpetuation in this trajectory threatens the growth rate in aggregate – not to mention a reduction in the growth rate overall.

2) International sales grew sub 2% in the quarter. The company noted that it was really +18% excluding a one time shipment a year ago to Dome, a Japanese partner. But the reality is that this was footwear, which is one of UA’s hottest growth businesses. It should be comping the comp with little difficulty.

3) One of the things that saved UA this quarter was growth in its accessories business. Accessories now stands at about 9.5% of total sales. That’s pretty meaty – ie it is unlikely to get much higher. But that’s not as big of a deal to us as the fact that accessories added more revenue in the quarter than footwear did. And that’s ANY way you look at it. Year over year, sequentially, vs 2 years ago…take your pick. Why does that matter? When is the last time you heard anyone say “I’m in this stock for growth in accessories. Probably never. Its about footwear and international, which are both still in their infancy. In fact, on a combined basis their revenue was only slightly greater than UA’s entire pre-tax income this quarter ($95mm vs $90mm).

The inventory position was the big saving grace, as it was down 2% versus a 24% boost in sales. That’s outstanding. But there was literally no mention of the word ‘receivables’ in the quarter. Inventories might be paramount – but the aggregate Receivable dollar figure is within $1mm of Inventories at $311mm. Inventories were down 2%, but Receivables were up 33%. In other words, working capital still came down by $74mm in a quarter where inventories were hailed as coming under control. That’s a big disconnect to us. Clearing inventories is one thing, but clearing them with more generous terms is another.

Here's our previous commentary on UA explaining part of our bearishness.

UA: We’re Getting Bearish (from Oct 12)

This company needs to beat on the top line to keep its momentum going, but we think that wind is being sucked from its sail. The sole multiple supporter is at risk based on our math.

We’re getting bearish on UnderArmour. To be clear, this is a TREND/TRADE call given concerns about the top line, and to a lesser extent, SG&A costs needed to compete in the footwear arena. We think that the long-term TAIL opportunity is largely in-tact, and if our near-term call does not play out, we’ll likely reverse course. But the underlying research is compelling enough for us to get bearish on top line trajectory.

Simply put, we think that wholesale sell-in has been growing faster than retail sell-through for too long.

- By our math, which isolates like-for-like apparel sales by stripping out footwear, International, UA Retail, and e-commerce, UA sell-in to retail has been 20%, 14%, 20% and 28% over the past four quarters, respectively.

- Those are great numbers. But unfortunately retail sell through was 3%, -1%, 17% and 22% over those same periods per third party POS data services.

- The latter two data points might seem like a nice rebound, but it’s not enough. They have not made up for the (-17%) and (-16%) shortfall witnessed at during 4Q11 and 1Q12, respectively. In fact, they added to the shortfall in sell-through.

- Our concern about last year lies in the amount of packaway merchandise that still needs to be sold through. During those two time periods, UA’s Gross Margins and Inventories both improved on the margin. With the sell-in/sell-through gap eroding. That’s simply not good. It suggests that excess product was pushed out to retail.

- In looking at results from specialty retailers like Dick’s as well as Department stores, it’s pretty clear that they are already heavy cold-weather gear before the selling season really begins due to packaway from last year. Simply put, in the absence of excess vendor support they did not clear out goods last year at bargain-basement prices. They stuck it in boxes in the stock room. Ross Stores and TJ Maxx concur with those thoughts on inventory levels.

- Two of our industry sources – including one mid-sized private brand – suggest that these trends are not specific to UA, but are pervasive throughout several players in the industry.

- Basically, this threatens either/or the initial shipment into retail or the first replenishment order – the latter of which happens in the back half of October through the first half of November.

- We’re not suggesting that revenue will be down. But simply that the Street’s 23% top line growth rate for 3Q, or its 29% rate for 4Q (which would be guidance in the release) are at risk.

Another point we’re slightly more concerned about is the success factor associated with footwear. It’s no secret that the footwear initiative at UA is slow to catch. But we think about this a bit different than most. In the end, we think that UA will realize the 6-8% share that most ‘non-Nike competitors’ steadily enjoy. The problem is that the cost of this share will be dramatically higher than the company is currently set-up for. So will UA realize up to $1bn in footwear revenue? It could definitely get there. But it could take the aggregate EBIT margin down by 200-300 basis points along the way. We think that any radical shift in expense structure will take time. But unfortunately, so will a big wad of footwear dollars.

Over the past 2 years, UA has had issues impacting margin, and those start getting easier. But all along the way, the market has looked right through ‘em due to the strength in top line growth. Perhaps it puts up good earnings numbers, but our sense is that the risk of a top line miss is not fairly represented in a stock trading at 37x next year’s EPS and 20+x EBITDA. This company NEEDS a top line beat to head higher, and perhaps even to stand still. Short interest might seem lofty at 13% of the float, but UA’s short interest has historically peaked at 3x that level. It doesn’t give us much confidence either that management has been net sellers of the stock.

Management at the Goldman Retail Conference

“So as far as the back half of the year goes, obviously, in addition to our guidance, I think a couple of things that are important to note, is what are some of those things out there in the back half of the year that could change a guidance for us. Two of – the two biggest things we saw was obviously weather, weather plays an important part especially in the fourth quarter and coming out of a warm winter last year not only does that impact how people book their business for this winter, how they plan for this winter, but there is also some leftover stock from last year too, so how that impacts the start of this fall winter season.

So, if there is upside in the back half of the year relative to weather being colder than last year that would pretty much be in the fourth quarter for us. The other piece of that as we talked a lot about at our last earnings call, is our E-commerce business, and we talked about some challenges we were having in the front half of this year relative to our conversion rate since we launch the new site last November, and that conversion rate was below last year's conversion rate and the gap was widening during the front half of the year.

So, clear the path for E-commerce team, put some quick fixes in place, basics around speed and around easier shop-ability on the site and in the last five weeks or so, we've seen that gap narrowing now for the first time this year versus widening as far as the year-over-year conversion rate. So, that's a good sign for the back half of the year too, but again, E-commerce heavily weighted towards the fourth quarter. So, when you look at the – our guidance in the rest of this year upside, and weather upside for E-commerce business continues to improve, those would be good things for us in the back half, and that it all be weighted towards the fourth quarter.”

Read this how you want, but to us it sounds like an incrementally cautious read on 3Q with a ‘keeping our fingers crossed for a few things to go right in 4Q’ position.

Simply put, we don’t like UA at $56.60. We putting this one in the bucket of our shorts – along with M, KSS, GPS, SPLS, COH and CRI. As always, we identify the fundamentals. Keith will manage risk around the specific price.