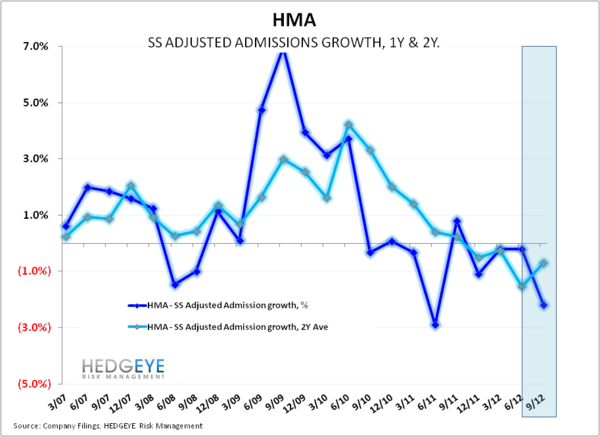

Health Management Associates (HMA) recently reported third quarter earnings that were in-line with consensus estimates. Same Store Admissions and Adjusted Admissions both deteriorated sequentially on a one-year basis but improved on a two-year basis. Everything from weather to a decline in uninsured admissions played a role in lagging volume growth.

The company lowered its guidance for SS admissions to between -3.0% & -5.0% but affirmed its expectation for FY2012 SS adjusted admission growth between -1.0% & +1.0%