Buffalo Wild Wings printed a highly disappointing 3Q12. This has been a difficult stock to call this year – the market’s reaction to earnings prints have been testament to that. As things stand post 3Q earnings, we are back where we started: $3.05 in FY12 EPS.

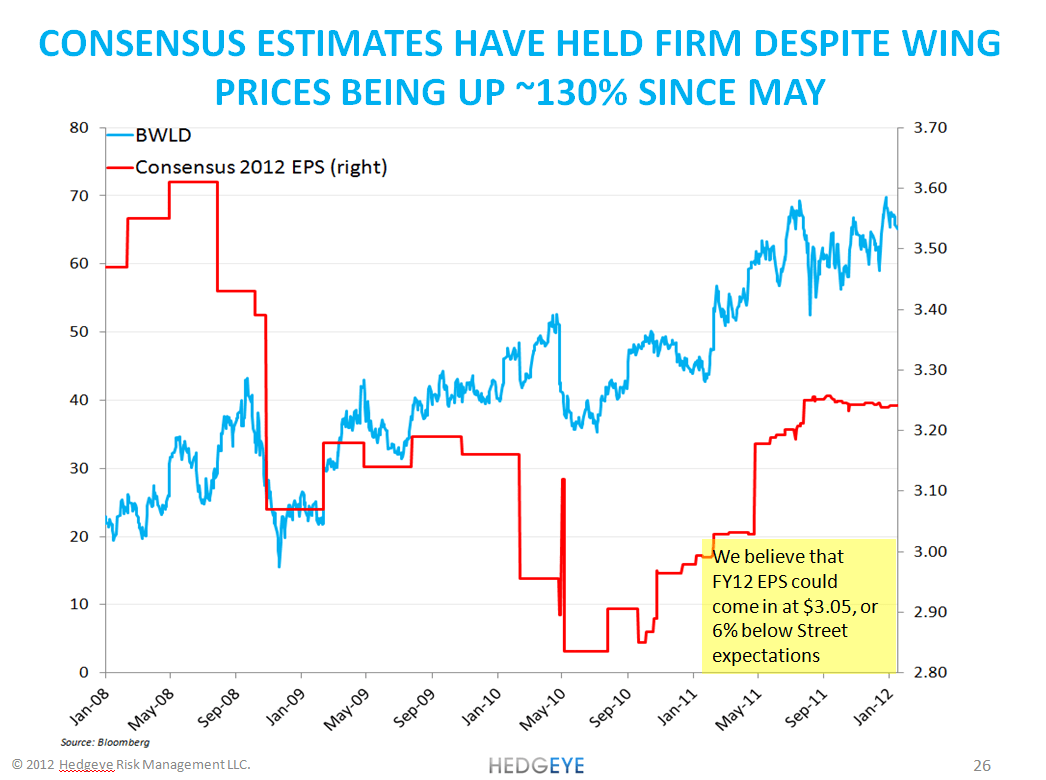

Below is a slide from our January 19th 2012 conference call outlining our bearish view of BWLD for the year. We stuck our neck out and made a contrarian call of $3.05 in earnings for 2012. Needless to say, that was an ill-timed call, but the two pillars of our bear case – input costs and the cost of growth – have been proven out. We expect earnings revisions from the Street, which remains at $3.21 for FY12. We remain negative on Buffalo Wild Wings and would expect the stock to break $70.

Recap

Management highlighted “high cost of sales and incremental preopening expenses” as moderating factors in earnings per share of $0.57 versus $0.61 in 3Q11 and $0.61 consensus.

Comparable restaurant sales, for company stores, grew 6.2% year-over-year, which was in line with consensus. The revenue miss was driven in part by new unit volumes declining year-over-year. This was especially disappointing for the bulls, given that this has been described – and valued – as a growth concept for restaurant investors. Operating income declined 8% versus last year. Consensus was expecting 5.2% operating income growth.

From here, it seems that margin pressure will continue with decelerating same-restaurant sales. Weather could be a potential headwind for the stock as we head into the winter months. Independent of weather, traffic trends remain a concern going forward as the company is – incredibly – taking 6% price in the fourth quarter. That level of pricing could have unintended consequences for the brand.

Howard Penney

Managing Director

Rory Green

Analyst