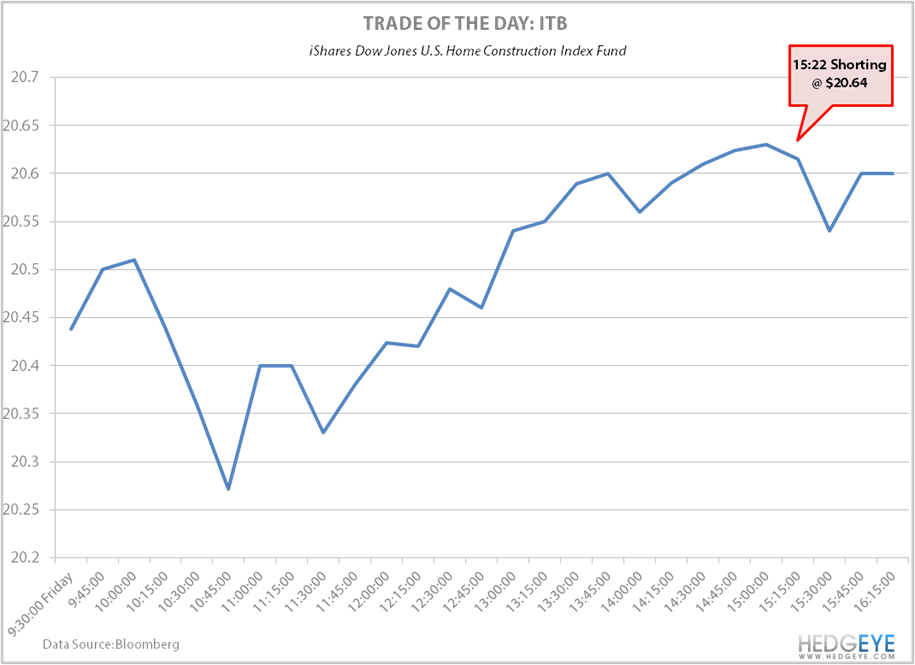

Today we shorted the iShares Dow Jones U.S. Home Construction Index Fund (ITB) at $20.64 a share at 3:22 PM EDT in our Real Time Alerts.

Some investors are too optimistic about the housing recovery and a lot are still long housing at these levels. Immediate-term mean reversion risk finally moves to the downside with market beta turning bearish. Another down day like today can do wonders for a short. We’ll watch and wait with this one.