CAT: 9X Peak Earnings Is Not “Cheap”

- Revisions Negative: This morning, we are seeing lots of revisions downward for CAT’s 2013 EPS. Even though the company did not explicitly provide 2013 guidance for EPS, the commentary about mix and other trends suggest 2013 EPS will decline from 2012 record levels. Flat sales and declining margins vs. 2012 imply lower 2013 EPS.

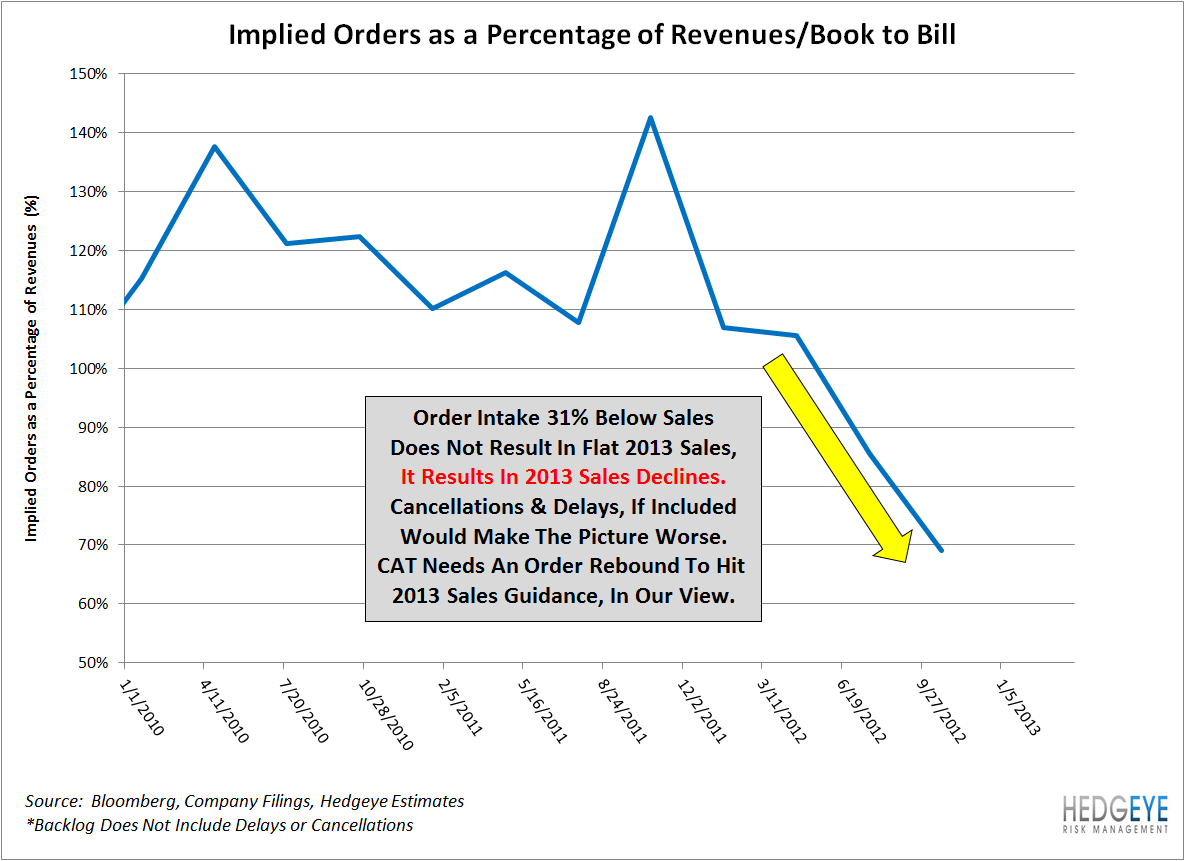

- How Much Lower?: If the book-to-bill ratio of 0.69 in the quarter is any guide, 2013 EPS will head quite a bit lower than 2012. That leaves 2012 as the “peak” in this cycle.

- Peak EPS & Peak Multiple: We dislike “peak multiple” valuation frameworks for a number of reasons (a multiple is just an inflexible implied DCF with all of the assumptions hidden, for one), but we would point out that deep cyclicals like CAT are unlikely to be seen as cheap at 9x peak EPS.

- Downhill: In general, owning a deep cyclical right after “peak” earnings is unlikely to work out well.

- Orders Surprisingly Weak: We found the weakness in CAT’s orders surprising yesterday – and we were very bearish on orders going in. In retrospect, the significant declines in order activity probably drove CAT management to lay out their ultra-bearish scenarios at the MineExpo Analyst day. Orders would have to rebound nearly 50% from the 3Q 2012 run rate for CAT just to hit its 2013 sales guidance, in our view.

- Better Industrials Longs: We like many things about CAT the company: great products, good markets, good people etc. The stock, however, seems a very bad long. Many better Industrials are out there - see our Truck OEM Black Book on PCAR and our upcoming Novemeber 5th Black Book on Express & Courier Services for our take on better long ideas.

Jay Van Sciver, CFA

Managing Director

HEDGEYE RISK MANAGEMENT

120 Wooster St.

New York, NY 10012