Keith asked me today if I’d stay short COH into the print. His quant models say that the answer is to short more here, and fundamentally, I can’t say that I disagree as the primary reasons we’re short it are still in-tact.

Specifically, and simply, revenue is decelerating while the cost of growth is rising. This should be fairly evident in Coach’s numbers for another 2-3 quarters at a minimum. Growth is dependent on the Legacy launch, as well as Men and to a lesser degree, China. At the same time, SG&A costs are rising in advance of the launch (which may or may not work), and Gross Margins are at risk as the financial triangulation of Sales Inventories and Margins rests in a tenuous point of our SIGMA analysis.

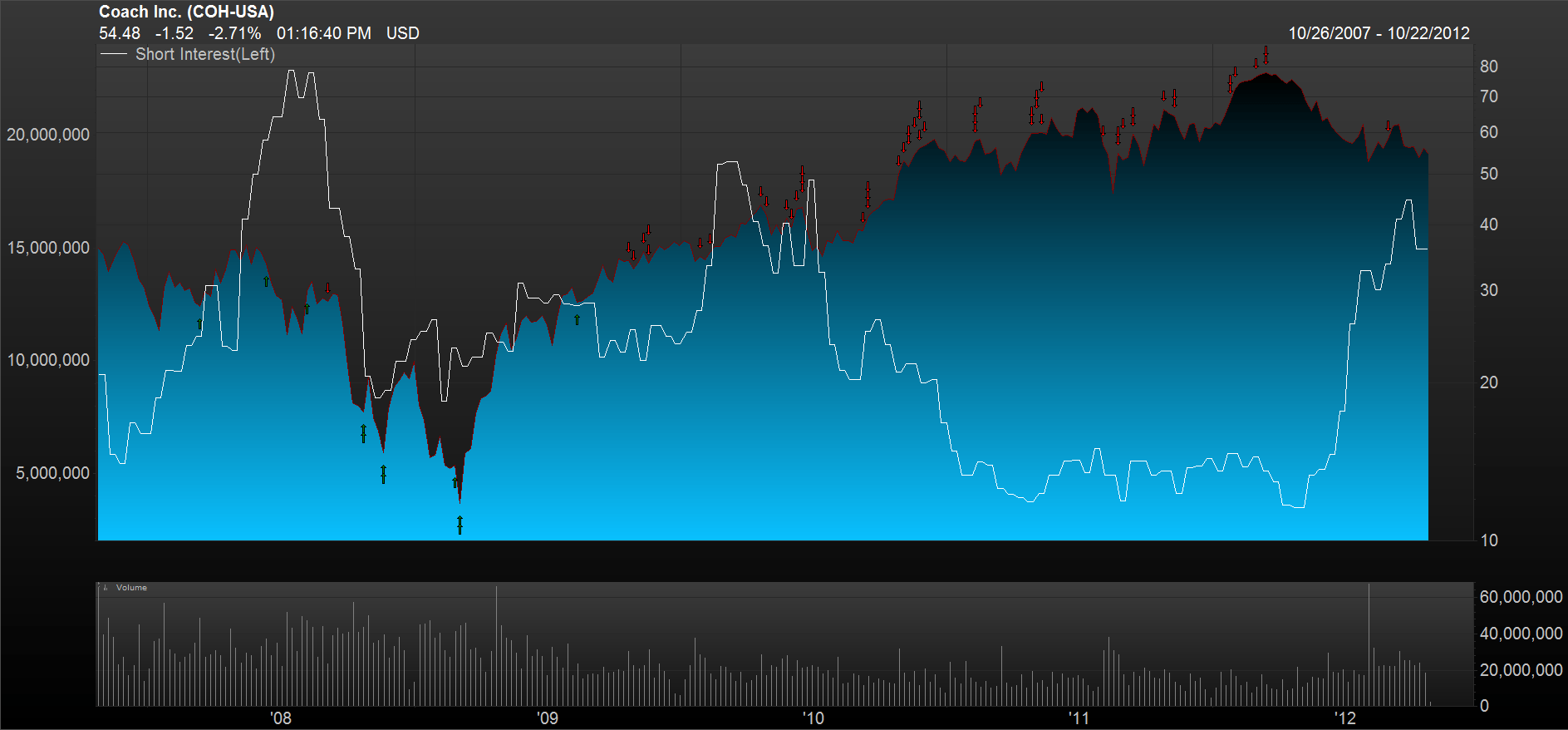

We concur that the stock looks cheap on next year’s numbers, but a) valuation is not a catalyst, and b) we’re 5% below the consensus this year (fiscal 6/13), and 9% below for the following year. We also hear the argument that sentiment is already bad, but we’re not so sure. In fact, we’re looking at about 4% of the float short, while historical peaks have been double that. Interestingly enough, higher short interest has not proven to be a deterrant from making money here on the short side. Check out the chart below to track the historical trend. Lastly, the stock has been acting poorly over the past few days, but note that it’s still $2 above the closing price on the day the company last released – and we have no reason to believe that things have improved materially.

The biggest caveat is that they’re likely to start with their new reporting structure with this print. There will be confusion on the release. People will be slow to react, and any positive spin by the company will be tough to contextualize. But if they stop reporting comps, or other important info, at a time when sales growth WILL slow and costs WILL rise, it can’t be good.

It’s always easy to get spooked headed into a print with any position – long or short. But when the research tells us to stand our ground, that’s exactly what we’ll do. Again, valuation is not a catalyst.

Coach’s SIGMA Positioning is Not Good

Short Interest Is Nothing To Be Afraid of Here