-- For specific questions on anything Europe, please contact me at to set up a call.

Positions in Europe: Short France (EWQ); Long German Bonds (BUNL)

Asset Class Performance:

- Equities: The STOXX Europe 600 closed up +1.7% week-over-week vs +2.1% last week. Top performers: Cyprus +21.9%; Greece +5.6%; Spain +3.4%; France +3.4%; Denmark +2.7%; Italy +2.3%; Romania +2.2%; Germany +2.0%; Austria +2.0%. Bottom performers: Ukraine -6.2%; Latvia -0.9%; Hungary -0.5%; Poland -0.5%. [Other: UK +1.8%].

- FX: The EUR/USD is up +0.62% week-over-week vs -0.74% last week. W/W Divergences: SEK/EUR +1.31%; CZK/EUR +0.60%; NOK/EUR +0.37%; HUF/EUR +0.20%; RUB/EUR +0.09%; TRY/EUR +0.09%; DKK/EUR 0.00%; CHF/EUR -0.02%; RON/EUR -0.31%; PLN/EUR -0.32%; GBP/EUR -1.00%; ISK/EUR -1.87%.

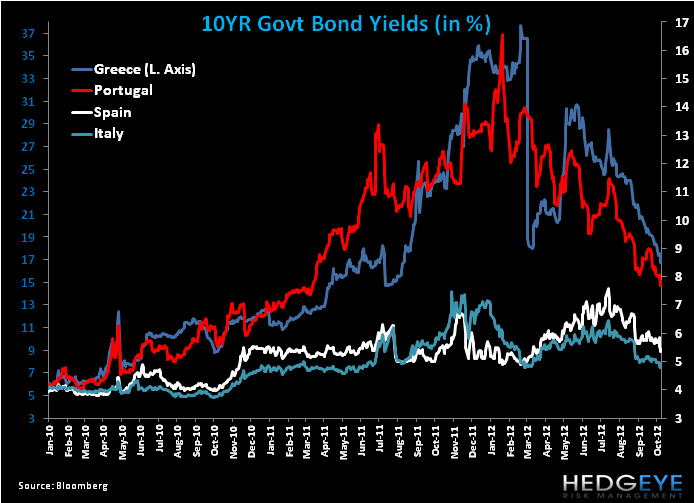

- Fixed Income: The 10YR yield for sovereigns were mostly lower on the week for the periphery and higher for the core. Greece declined the most week-over-week at -143bps to 16.78%, followed by Portugal -38bps to 7.67% and Spain -34bps to 5.34% and Italy -20bps to 4.77%. Germany rose the most at +12bps to 1.60% and France gained +2bps to 2.2%.

EU Summit Disappoints, No Surprise

The EU Summit concluded its two day meeting today and leaders issued a statement indicating that they will continue to work towards the goal of a single bank supervisor “with the objective of agreeing on the legislative framework by 1 January 2013” and “work on the operational implementation will take place in the course of 2013”.

One of the main struggles that Eurocrats are running up against is how to create a fiscal and banking union. It appears that they’re trying to craft both simultaneously; however recent discussions suggest that a banking union is getting more attention which we find problematic because it means Eurocrats are putting the cart ahead of the horse.

We’ve written about it for many weeks, but the importance of establishing a fiscal union is critical for the Eurozone if it hopes to retain its existing structure (the global crisis showed the flaws of only having a monetary union). We’re of the opinion that states will very unwillingly give up their fiscal sovereignty, which should drive decision from a core consensus on how to set up a fiscal union far afield.

That said, given the linkage between sovereigns and their banks and across other member states, until there is a fiscal union there is little hope of having a functional banking union given the need for an authority (or authorities) to regulate both fiscal (think veto national budgets) and mandate banking conditions as well as determine bailouts of sovereign and banks throughout the region. And to boot, European politicians are considering crafting a banking union not only around the 17 Eurozone member states, but the entire EU27.

So what are the key and ongoing points of indecision following the Summit?

- Banking Union: The statement released following the Summit did not discuss whether ECB supervision would apply to all 6K banks in the region or just the systemically important institutions (Merkel recently said that this still needs to be hashed out and is more in favor of only the larger banks).

- Greece: Nothing specific to future bailouts of Greece or debt restructuring was mentioned. “We welcome the determination of the Greek government to deliver on its commitments and we commend the remarkable efforts by the Greek people."

- ESM: No further detail on the scope of the ESM to directly recapitalize troubled banks was offered. Does the facility have to be first completely capitalized to lend? Will legacy assets be eligible for a loan?

Of note this week was a paper from the EU Council’s top legal adviser contending that a plan to create a single supervisory mechanism for Eurozone banks is illegal and goes “beyond the powers” permitted under law to change governance rules at the ECB. We also heard France, the second largest economy in the Eurozone, express reluctance to cede sovereignty on fiscal policy.

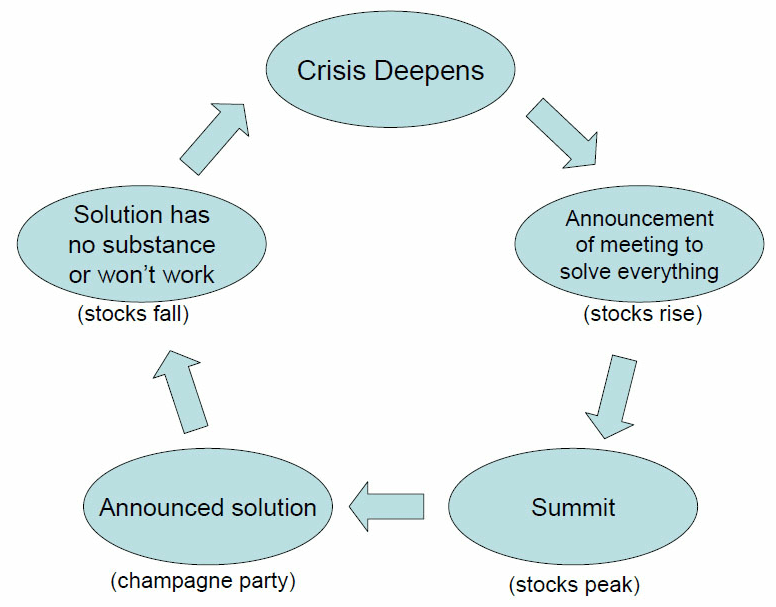

This week’s Summit simply confirmed that there will be another plan to make a plan and plenty of details and questions that remain unanswered. David Einhorn's chart below sums this up pretty well:

Spanish Bailout in the Crosshairs

This week an unnamed senior Finance Ministry official said that Madrid is considering requesting a credit line, rather than a full-scale bailout from the ESM, and may qualify for the ECB's OMT.

Germany said it was open to a credit line for Spain, which makes some sense given the scope of the ESM undefined.

Yet we’re no further or closer this week to determining the timing of a Spanish sovereign bailout.

- Will a formal bailout request be linked to regional elections in Basque Country and Galicia as soon as this Sunday or Catalan elections on November 25th?

- How will Spanish bonds act in light of last week’s decision from the S&P to downgraded Spain by 2 notches to BBB- ? The 10YR is currently trading with a yield of 5.34%, well off highs of 7.5% in late July of this year. Could we see a selloff by investors worried that the country's credit rating will be cut to junk? (Note: Moody’s confirmed Spain's government bond rating at BAA3, with a negative outlook this week).

Our Real-Time positions in Europe remain Long German Bunds (BUNL) and short France (EWQ). See our note on 10/16 for our position on France.

The European Week Ahead:

Sunday: Spanish regional elections in Basque Country and Galicia

Monday: 2011 Eurozone Government Debt/GDP Ratio; Aug. Spain Mortgages-capital loaned, Mortgages on Houses; Aug. Greece Current Account

Tuesday: Oct. Eurozone Consumer Confidence – Advance; Sep. UK BBA Loans for House Purchase; Oct. France Production Outlook Indicator

Wednesday: Oct. Eurozone PMI Manufacturing and Services – Advance, PMI Composite; 2Q Government Debt; Germany DIHK Trade and Industry Group Releases Fall Outlook Survey; Oct. Germany PMI Manufacturing and Services – Advance, IFO Business Climate, Current Assessment and Expectations; Oct. UK CBI Trends Total Orders, Selling Prices and Business Optimism; Oct. France PMI Manufacturing and Services - Preliminary; Sep. France Jobseekers; Oct. Italy Consumer Confidence Indicator

Thursday: Sep. Eurozone M3; 3Q UK GDP - Advance; Aug. UK Index of Services; Spain Sep. Producer Prices; Italy Sep. Hourly Wages; Aug. Italy Retail Sales

Friday: Nov. Germany GfK Consumer Confidence Survey; Sep. Germany Import Price Index; Oct. France Consumer Confidence Indicator, Business Survey Overall Demand; 3Q Spain Unemployment Rate; Oct. Italy Business Confidence, Economic Sentiment

Call Outs:

UK - BOE Minutes from October 3-4 meeting: officials were split on need for more stimulus.

France - French Finance Minister Pierre Moscovici said in an interview with Les Echos that he had "positive" discussions with Moody's regarding the country's triple-A rating. Recall that Moody's said in early September that it would conclude an assessment of France, which it currently rates triple-A with a negative outlook, sometime in October.

Banking Union - ECB President Draghi said that the ECB may not be operational as the single supervisory mechanism for Eurozone banks until 2014. He noted that “It’s very important that the council regulation enters into force January 1 but that doesn’t mean supervision will be in place on January 1 from an operational view point.”

Banking Union - citing EU officials Britain is pushing for changes to a proposed Eurozone banking union to dilute the power of the ECB. Britain plans to propose a system that would give countries outside of the banking union the possibility of blocking those within the group from banding together to influence EU-wide regulations, such as defining the type of capital reserves that qualify as a cushion against banks' risky assets. While the article noted that Britain is still in favor of a banking union, it said that its push for an effective veto for non-euro countries (something that has been discussed before in the press) could slow down the progression.

Spain - Faces a refinancing hurdle of €29.5B at the end of October. Finance Minister Luis de Guindos stressed that he was "very comfortable" with the debt repayments.

France - French Prime Minister Jean-Marc Ayrault said on Tuesday that reforms to make French industry more competitive will be spread over two to three years. While he did not detail what measures would be taken to improve companies' competitiveness. He also reiterated that France must meet its target of reducing the deficit to 3% of GDP by the end of 2013 from a projected 4.5% this year.

France - France's business federation has vetted its frustrations with Socialist President François Hollande’s polices. The group is rightly concerned about a competitiveness drag, including from Article 6 of the new tax law, which raises the top rate of capital gains tax from 34.5% to 62.2%. For reference these levels compare with 21% in Spain, 26.4% in Germany and 28% in Britain.

Data Dump:

Eurozone CPI 2.6% SEPT Y/Y vs 2.7% AUG

Eurozone ZEW Economic Sentiment -1.4 OCT vs -3.8 September

Europe EU27 New Car Registrations -10.8% SEPT Y/Y vs -8.9% AUG [dropped the most in 2 years]

Eurozone Construction Output -5.5% AUG Y/Y vs -6.2% JUL [0.7% AUG M/M vs 0.1% JUL]

Germany ZEW Current Situation 10.0 OCT vs 12.6 September

Germany ZEW Economic Sentiment -11.5 OCT vs -18.2 September

Germany Producer Prices 1.7% SEPT Y/Y vs 1.6% AUG

UK PPI Input -0.2% SEPT M/M vs 1.9% AUG [-1.2% SEPT Y/Y vs 1.1% AUG]

UK PPI Output 0.5% SEPT M/M vs 0.5% AUG [2.5% SEPT Y/Y vs 2.3% AUG]

UK CPI 2.2% SEPT Y/Y vs 2.5% AUG

UK RPI 2.6% SEPT Y/Y vs 2.9% AUG

UK ILO Unemployment Rate 7.9% AUG vs 8.1% JUL (Olympics boosts job creation)

UK Jobless Claims Change -4k SEPT vs -14.2K AUG

UK Retail Sales with Auto Fuel 2.5% SEPT Y/Y vs 2.5% AUG

UK Rightmove House Prices 1.5% OCT Y/Y vs 0.7% SEPT

UK Public Sector Net Borrowing 10.7B GBP SEPT vs 10.8B GBP AUG

Italy Industrial Orders -9.0% AUG Y/Y vs -4.9% JUL

Switzerland Credit Suisse ZEW Expectations -28.9 OCT vs -34.9 September

Switzerland Exports 2.6% SEPT M/M (exp. 0.5%) vs 0.4% AUG

Switzerland Imports 3.0% SEPT M/M vs 2.6% AUG

Switzerland Producer and Import Prices 0.3% SEPT Y/Y vs -0.1% AUG

Netherlands Consumer Confidence -32 OCT vs -29 SEPT

Netherlands Retail Sales 0.9% AUG Y/Y vs -3.9% JUL

Ireland PPI 2.2% SEPT Y/Y vs 6.0% AUG

Sweden Unemployment Rate 7.4% SEPT vs 7.2% AUG

Finland CPI 2.7% SEPT Y/Y vs 2.7% AUG

Portugal Producer Prices 4.6% SEPT Y/Y vs 4.2% AUG

Austria CPI 2.7% SEPT Y/Y vs 2.2% AUG

Slovakia CPI 3.8% SEPT Y/Y vs 3.8% AUG

Slovenia Unemployment Rate 11.6% AUG vs 11.7% JUL

Slovenia PPI 0.7% SEPT Y/Y vs 0.4% AUG

Czech Republic Export Price Index 3.7% AUG Y/Y vs 4.7% JUL

Czech Republic Import Price Index 5.8% AUG Y/Y vs 5.5% JUL

Czech Republic PPI 1.7% SEPT Y/Y vs 1.9% AUG

Poland CPI 3.8% SEPT Y/Y vs 3.8% AUG

Poland Producer Prices 1.8% SEPT Y/Y vs 3.0% AUG

Poland Sold Industrial Output -5.2% SEPT Y/Y vs 0.5% AUG

Russia Industrial Production 2.0% SEPT Y/Y vs 2.1% AUG

Russia Producer Prices 11.6% SEPT Y/Y vs 6.6% AUG

Russia Disposable Income 3.8% SEPT Y/Y vs 6.8% AUG

Russia Retail Sales 4.4% SEPT Y/Y vs 4.3% AUG

Russia Unemployment Rate 5.2% SEPT vs 5.2% AUG

Turkey Unemployment Rate 8.4% JUL vs 8.0% JUN

Turkey Consumer Confidence 88.8 SEPT vs 91.1 AUG

Interest Rate Decisions:

(10/18) Turkey Benchmark Repo Rate UNCH at 5.75%

(10/18) Turkey Overnight Lending Rate CUT 50bps to 9.50%

Matthew Hedrick

Senior Analyst