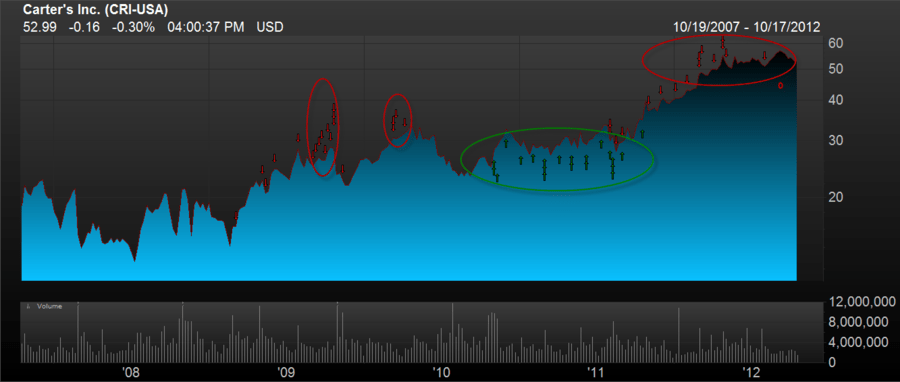

Carter's (CRI) insiders have had a fabulous record of trading the stock as you can see in the chart below (red = sell, green = buy). With the recent insider selling that's been going on, we wouldn't be a buyer if the past is indicative of anything. We remain short CRI in our Real Time Alerts.