This note was originally published at 8am on October 04, 2012 for Hedgeye subscribers.

“A half-truth is more dangerous than a lie.”

-Saint Thomas Aquinas

The aforementioned quote comes by way of Saint Thomas Aquinas, who, to this day, is still considered among the most influential priests in the history of the Catholic Church as a function of his bridging the gap between ancient philosophical works and theology. While this is certainly not the proper forum to discuss religion in any detail, we do think modern-day financial markets could use a scholar of Aquinas’ caliber to help bridge the gap between the prices of many liquid asset classes and the fundamental data underpinning them.

Furthermore, the Manic Media outlets tasked with delivering us our economic and financial news could certainly use an army of Aquinas-like editors to help bridge the gap between what has occurred and what is reported.

To say that a large portion of the headlines and stories we’ve consumed in recent quarters were delivered in one of the following two formats would be a gross understatement: “ABC Occurred On XYZ Stimulus Speculation” or “[INSERT: Policymaker Name] Signals Further [INSERT: Stimulus Measures; Bailout Funds; etc.]”. In effect, the financial media can be considered guilty of incessantly stoking the broad-based optimism bias of both investors and corporate executives alike in priming news – particularly anything negative – with rumors and expectations for future improvement via “stimulus” or bailouts.

For reference, we use quotations around the word “stimulus” because we have shown repeatedly since 2010 that Policies To Inflate do little beyond stoking commodity price inflation that ultimately slows the pace of economic activity. In fact, if we had a burning Bernanke buck for every article in the last three months that anchored on some form of “stimulus”, Hedgeye would have enough capital to create all of the jobs QE3 is allegedly supposed to produce! River baptisms continue to dominate the heavily-biased study of economics in Western academia.

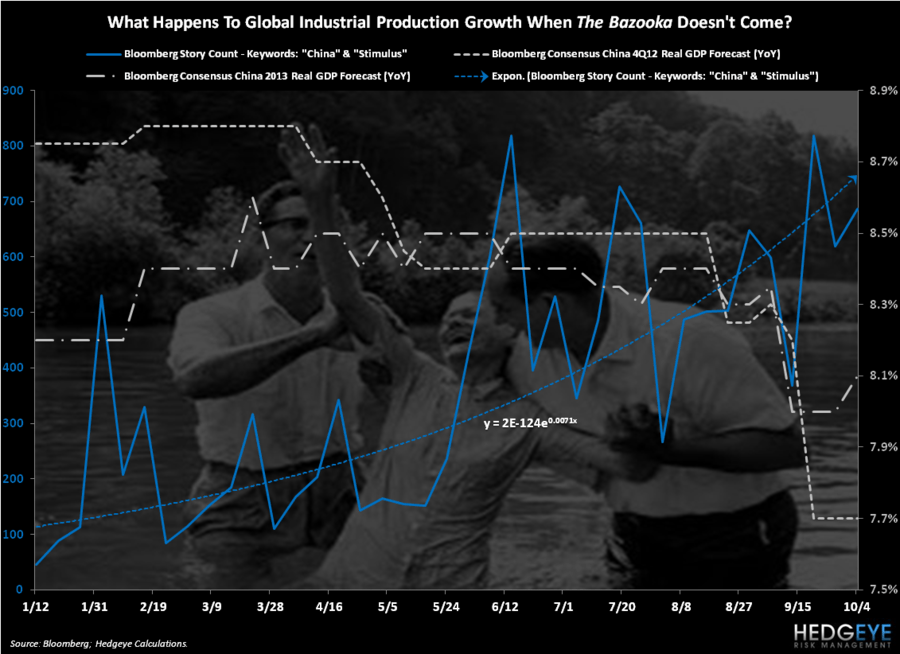

Take China, for instance. For much of the year-to-date, just about every occurrence in the Chinese economy was reported on in the context of “stimulus”. Moreover, a great deal of what Chinese policymakers have said publically in the YTD has been interpreted as a general update on the size and scope of China’s pending stimulus package. Alas, the bazooka has yet to be spotted and, perhaps more importantly, we continue see limited scope for and probability of a large-scale Chinese stimulus package over the intermediate term. We have published a compendium of work detailing our thoughts on the subject, analyzing the key data series, political catalysts and rationale(s) of Chinese policymakers pertaining to this topic and are happy email them to you upon request.

A couple of the more entertaining rumors emanating from China in recent weeks were centered around actions by the China Securities Regulatory Commission and the National Development and Reform Commission. Last week, it was reported that Chinese stocks rallied over +2% during the last 90 minutes of trading on a rumor that the CSRC was going to hold a press conference to announce measures to boost the stock market after the close. The event turned out to be a previously-scheduled meeting with no major reforms or announcements to speak of. We’re sure you remember the CNY1 trillion of infrastructure initiatives from early SEP that got a large swath of the financial media and international investment community to both celebrate and cheer on further stimulus measures (“globally coordinated easing” was the catch-phrase of the day). Since then, Xu Lin, head of the planning department at the NDRC, has come out and blatantly refuted the consensus interpretation of the event:

“The recent accelerated infrastructure project approvals did not mean the government is rolling out more stimulus. These projects are already in our plan... [The] 4-trillion yuan package of state spending and tax cuts announced in 2008 stoked inflation and sparked concern local governments took on more debt than they can afford.”

– Xu Lin speaking to reporters at Peking University on SEP 17, 2012

Of course, Chinese policymakers could emerge from Golden Week next week or from their 18th Communist Party Congress in the second week of NOV with plans to materially reflate their ailing economy. The desire to pursue social and economic stability – particularly on the inflation and employment fronts – is great among Communist Party officials and, per the latest China Beige Book from CBB International LLC, the percentage of mainland companies reporting net firings increased +700bps QoQ to 20% in 3Q.

Despite obvious growing pressure to “do something” (as IMF Director Christine Lagarde would put it), we continue to take the view that Chinese policymakers have a much longer horizon for economic planning than most Westerners are able to comprehend through the prism of democracy. Xi Jinping and Li Keqiang (China’s likely future President and Premier) will be in power for a decade. Do you think it’s in their best interests to perpetuate China’s “unstable, unbalanced, uncoordinated and unsustainable” growth model (per current Premier Wen Jiabao) by reflating the Chinese economy just ahead of or early in their administration? Perhaps, though we’d argue anyone taking a longer-term view would be keen to anticipate the negative impact of a mid-regime property market bust and subsequent financial crisis upon Chinese economic growth and social stability. Unlike most Western financial market participants, the Politburo does not operate in the vacuum of YTD gains or with respect to some year-end bonus pool.

All told, the Chinese economy will continue to grow; it probably just won’t grow as fast or necessarily in the same manner as international investors and corporations have become accustomed to. That’s one of the core tenets of prospect theory, specifically in that myopic loss aversion from the status quo occurs not just from present states, but also from future states that were previously assumed to be true.

In this light, how will companies like Caterpillar Inc. and Fortescue Metals Group Ltd. react when the Chinese “stimulus” bazooka they’ve all been anticipating to varying degrees does not show up? How will international investors respond to this potential scenario? After accounting for 43.9% of global real GDP growth since 2008, does China even matter anymore? Why can’t everyone just buy the SPDRs and hold on for dear life until the data starts to improve?

While we are certain that none of these questions have easy answers, we are convinced that they need to be pondered by anyone managing risk in today’s choppy Global Macro environment. Best of luck out there, everyone.

Our immediate-term risk ranges for Gold, Oil (Brent), US Dollar, EUR/USD, UST 10yr Yield and the SP500 are now 1770-1786, 106.78-110.99, 79.60-80.23, 1.27-1.29, 1.58-1.69 and 1437-1462, respectively.

Darius Dale

Senior Analyst