This note was originally published at 8am on October 02, 2012 for Hedgeye subscribers.

“The peak in resource investment is likely to occur next year.”

-Glenn Stevens

Not all central bankers are like Ben Bernanke. Some of them, like the Reserve Bank of Australia’s Glenn Stevens, go both ways.

Last night Stevens and the RBA cut rates by 25 basis points to 3.25%. Unlike Bernanke, who hasn’t raised rates since taking over the Fed in 2006, Stevens hiked when he should have. And baby boomer retirees living Down Under on fixed incomes liked it.

I realize going both ways isn’t for everyone. If you get that dirty little thought out of your mind for a minute and think like hockey players – we have this little saying about grinding at both ends of the ice: ‘Backcheck, Forecheck, Paycheck.’ And we like that too.

Back to the Global Macro Grind…

When Cycles Peak, you want to be selling into them; not buying them because they look “cheap.” When Cycles Peak, cheap gets cheaper. A stock like Caterpillar (CAT) is our Pamela Anderson poster for that on the short side right now.

Hardcore Japanese Keynesians have been trying to “smooth” economic cycles since their local Pawn Star Economist, Paul Krugman, told them to “PRINT LOTS OF MONEY” in 1997. With Japan’s Nikkei having made lower-highs for 20 years (down again last night, -14.3% since #GrowthSlowing started in March, globally), it’s a worldwide wonder how they last.

While stamina matters, what we’ve learned from some of these economists is that their weathered old dogmas can hang around political life for longer than we can stand them. At the same time, their population growth goes negative, and their economic incentives go dark.

There’s a common sense (behavioral economics) explanation for this. As Michael Cox, Director of the Center for Global Markets and Freedom at Southern Methodist University, writes in The 4% Solution:

“Economies grow faster when investors choose to put their money into productive assets rather than government bonds or gold… businesses won’t get started, workers won’t get hired, and the economy won’t grow.”

Sound familiar?

Of course it does. So let’s buy the S&P Futures on a rumor that Spain does more of that, requesting another bailout, based on growth, inflation, and employment results that their politicians continue to make up on the fly. Then, let’s do that in the USA, kick the can to the edge of The Cliff, then have Nancy Pelosi save us from it in the nick of election time.

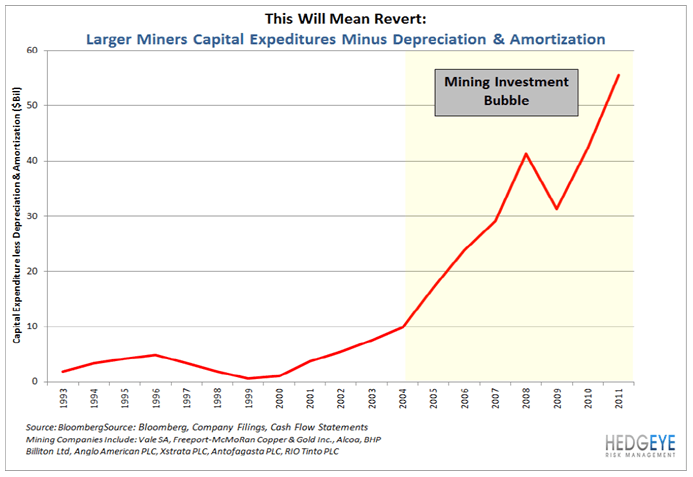

Perfect. Now back to that money printing, metal, and mining cycle peaking…

- The world’s largest miners are already cutting project capex

- The world’s largest mining equipment companies are already guiding down from peak capex investment numbers

- The world’s most credible central banker, Glenn Stevens, is cutting rates because Australia is right levered to #1 and #2

It’s not just the mining cycle that’s peaking (ask sales@Hedgeye.com for Jay Van Sciver’s long-cycle notes on CAT’s issues), it’s the SP500’s Earnings Cycle that’s peaking.

While sell-side consensus bulls have only been wrong by 45-72% on US GDP Growth in 2012, the guys who are always bullish still say they nailed it. So let’s look at what they’re forecasting on growth and earnings from here:

- After cutting their numbers, the slowest revenue growth for the SP500 since 2008

- A magical acceleration in revenue growth for the next 12 months from here

- NTM earnings as far as the eye can see, with operating margins expanding 100bps, per quarter!

If corporate earnings go flat to negative for the next 2-3 quarters, the “stocks are cheap” crowd better beg Bernanke for “multiple expansion” on lower earnings, because that’s the only way stocks are going up from here.

I wrote an intraday risk management note titled “Buyem!” around 1430 SPX on Wednesday of last week. On this morning’s rally, do yourself a favor and sellem’ on green before Earnings Season starts next week.

My immediate-term risk ranges for Gold, Oil (Brent), US Dollar, EUR/USD, UST 10yr Yield, CAT, and the SP500 are now $1770-1784, $108.21-112.98, $79.46-80.35, $1.27-1.29, 1.59-1.70%, $82.13-88.05, and 1430-1451, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer