Coffee prices continue to lead to the downside as the majority of the agricultural commodities – that we track as part of our process – declined as the dollar index strengthened. Beef and dairy prices remain the ones to watch for the restaurant industry in 4Q. The strength in beef prices is negative for TXRH, BLMN, WEN, JACK, CMG and others.

Summary View

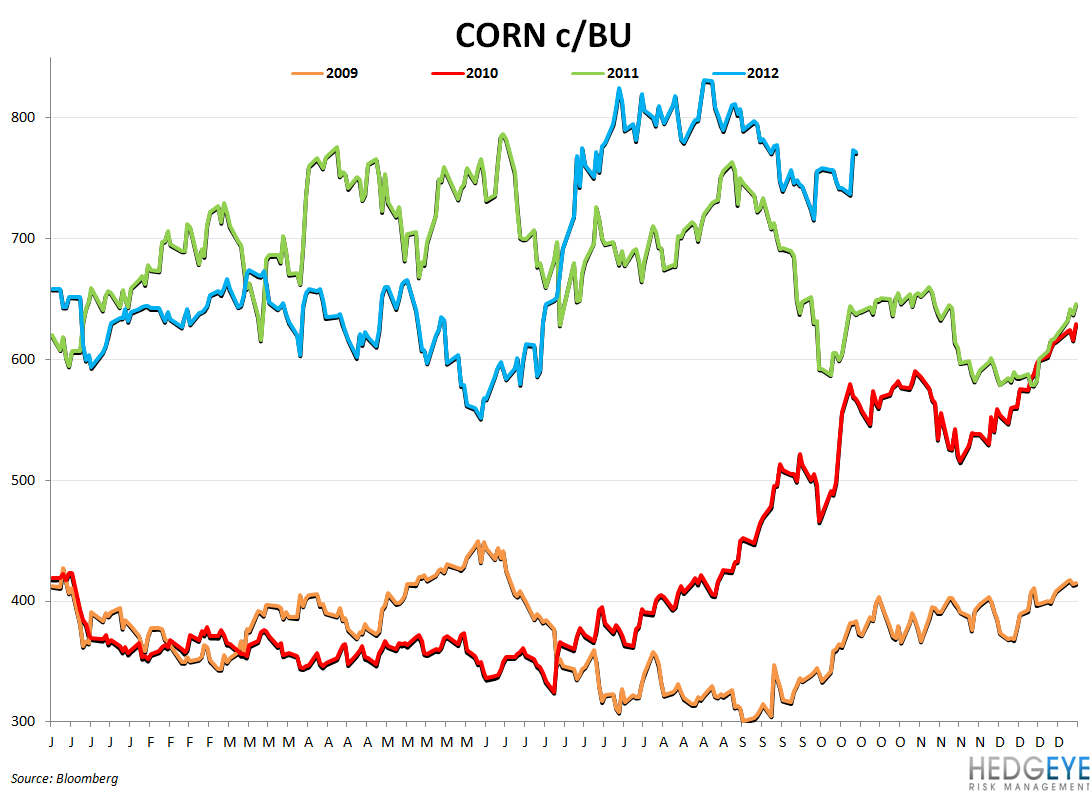

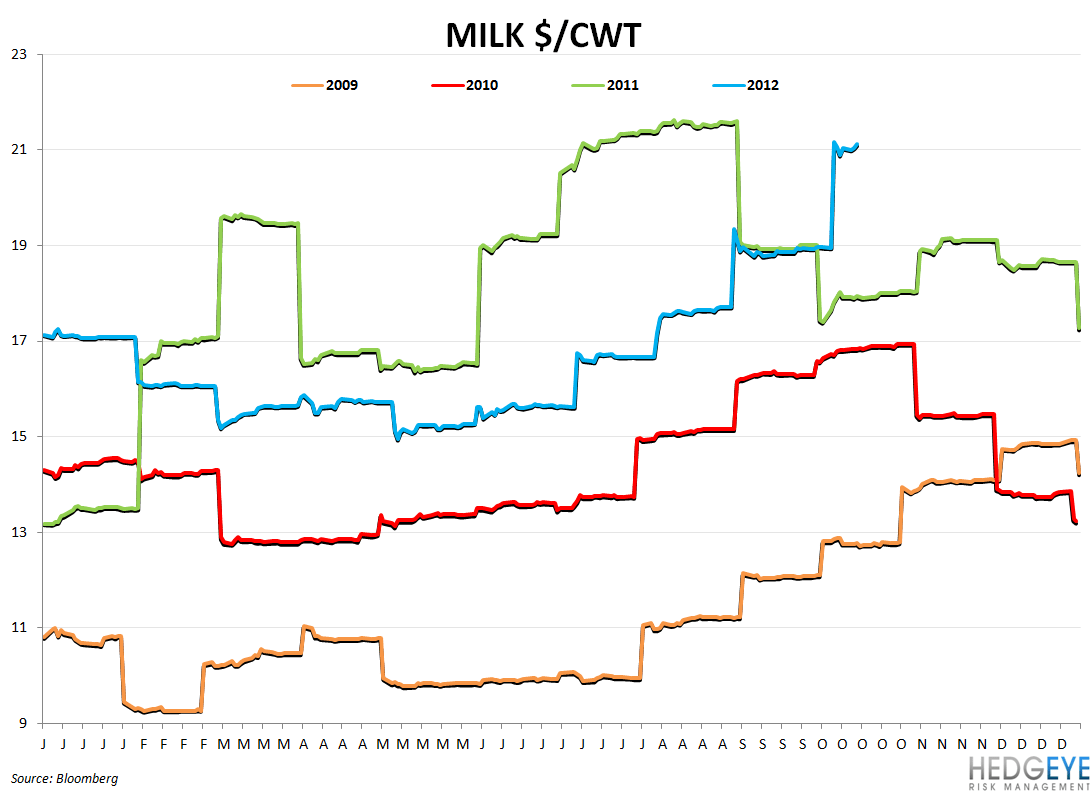

Beef prices gained 1.3% over the last week. The USDA’s WASDE report, released yesterday, was bullish for beef prices as lower expected cattle placements in the third quarter is expected to translate into lower supplies of fed cattle next year. Importantly for beef prices, and proteins more broadly, corn prices surged yesterday as the USDA reported that global inventories are expected to drop more than expected as the U.S. drought cuts output

Coffee prices continue to show weakness as coffee producers in Brazil are reportedly waiting for better prices. According to Bloomberg, the Brazilian Coffee Council is also concerned with low government inventories of the product and is proposing an auction for as many as 6 million bags of Arabica coffee. The continuing weakness in coffee prices is a positive for SBUX, PEET, DNKN, THI, CBOU, GMCR and other coffee retailers.

Gasoline Prices

Gas prices are up 12% year-over-year and we believe that this will have an impact on spending growth. On a regional basis, it is important to note that this impact is likely to be greater in some areas than others; in California gas prices are up 22% year-over-year and could have a significant impact on discretionary spending. Following a peak last week of over $5 per gallon in Southern California, recent prices now seem to be subsiding.

Correlation

Charts

Howard Penney

Managing Director

Rory Green

Analyst