TODAY’S S&P 500 SET-UP – October 12, 2012

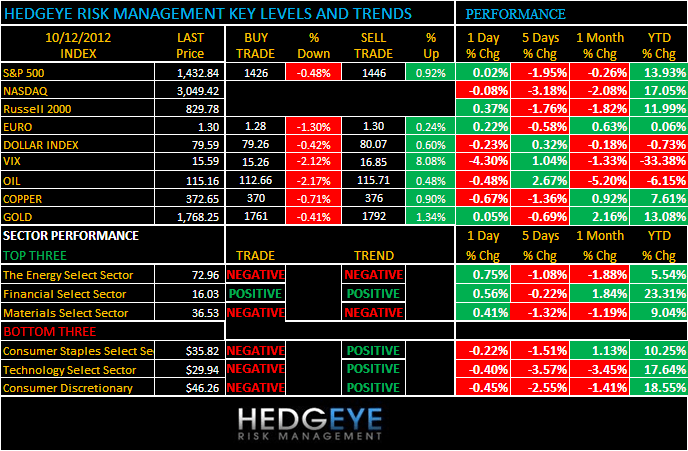

As we look at today’s set up for the S&P 500, the range is 20 points or -0.48% downside to 1426 and 0.92% upside to 1446.

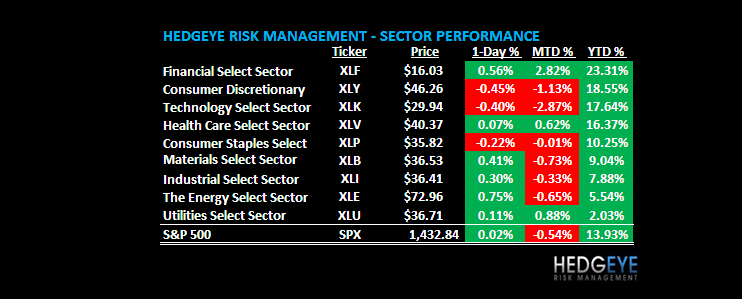

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 10/11 NYSE 909.00

- Increase versus the prior day’s trading of -737

- VOLUME: on 10/11 NYSE 646.68

- Increase versus prior day’s trading of 9.45%

- VIX: as of 10/11 was at 15.59

- Decrease versus most recent day’s trading of -4.30%

- Year-to-date decrease of -33.38%

- SPX PUT/CALL RATIO: as of 10/11 closed at 1.72

- Up from the day prior at 1.67

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 24.36

- 3-MONTH T-BILL YIELD: as of this morning 0.10%

- 10-Year: as of this morning 1.69%

- Increase from prior day’s trading of 1.67%

- YIELD CURVE: as of this morning 1.42

- Up from prior day’s trading at 1.41

MACRO DATA POINTS (Bloomberg Estimates)

- 8:30am: Producer Price Index M/m, Sept. est. 0.8%

- 8:30am: PPI Ex Food & Energy M/m, Sept. est. 0.2%

- 9:55am: University of Michigan Consumer Sentiment, Oct. preliminary, est. 78.0 (prior 78.3)

- 11am: Fed to buy $1.75n-$2.25b notes due 2/15/2036-8/15/2020

- 12:35pm: Fed’s Lacker speaks in Charlottesville, Va.

- 1pm: Baker Hughes rig count

GOVERNMENT:

- Dodd-Frank rules take effect that require companies to begin tallying derivatives trades to determine whether they cross $8b threshold for being designated swap dealers subject to heightened capital and collateral standards; CFTC also will require companies to tally foreign-exchange swaps, forwards

- Interior Secretary Ken Salazar, Senate Majority Leader Harry Reid, D-Nev., make announcement on renewable energy and public lands, 1:30pm

- Education Secretary Duncan answers Twitter questions about federal student aid, tools available to help students, families make informed decisions about financing higher education, 4pm

WHAT TO WATCH:

- Telefonica agreed to sell its Atento call-center division to Bain Capital, with enterprise value of EU1.04b, including debt

- WellPoint reorganizes in interim CEO Cannon’s 1st major move

- TPG withdraws A$694m offer for Billabong as talks end

- Softbank shares fell as operator said it’s in talks to invest in Sprint Nextel, said to be seeking control

- S&P put Softbank’s long-term outlook on creditwatch negative, citing announcement on Sprint Nextel talks

- Kraft said to be putting its Breakstone’s sour cream, cottage cheese business up for sale, may be worth ~$400m

- Gary Gensler, chairman of CFTC, said he’d be willing to serve 2nd term as head of the agency

- Carlyle given another month to consider making Chemring bid

- Family that controls Champion Technologies said to be seeking sale of the closely held company

- Nasdaq, setting up derivatives trading system in London, will seek more than 10% market share in its first year of operation

- JPMorgan expects investment-banking fees from U.S.-listed Chinese cos. to surge this year as they step up acquisitions

- Pfizer appealed judge’s order that CEO Read testify in person at federal trial on claims against anti-smoking drug Chantix

- Samsung Electronics won bid to continue selling newest Galaxy Nexus smartphone in U.S. during appeal

- Apollo Global, Oaktree Capital said to have rejected Nine Entertainment’s debt restructuring proposal, countered by offering funds managed by Goldman a smaller stake in the co.

- Honeywell expects to boost aerospace sales in Asia by 7% a year, double the pace in U.S.

- VMware said partnership with Cisco will change after its $1.26b acquisition of Nicira

- Answers Corp., which lost bid to buy About.com from New York Times in Aug., has other plans to grow through acquisitions

- Morgan Stanley execs said to have told partner in Rhinebridge structured investment vehicle that mortgages underlying SIV may cause it to fail

- Best Buy plans to match Amazon pricing in holiday season: WSJ

- Presidential Debate, China GDP: Week Ahead Oct. 13-20

EARNINGS:

- JPMorgan (JPM) 7am, $1.20 - Preview

- IGate (IGTE) 7:03am, $0.38

- Wells Fargo (WFC) 8am, $0.87 - Preview

- Webster Financial (WBS) 8am, $0.46

- DiamondRock Hospitality (DRH) 8am, $0.19

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Oil Heads for First Weekly Gain in Month on Middle East Tension

- Copper Traders Most Bearish Since June on Economies: Commodities

- Malaysia to Reduce Palm Oil Export Tax, Abolish Duty Free Quota

- Copper Drops on Concern Demand Will Fade Amid Global Slowdown

- Soybeans Drop as Global Supply Concerns Ease After USDA Report

- Gold Seen Gaining in London as Weaker Dollar Spurs Investment

- Sugar Declines on Speculation Demand Is Waning; Cocoa Advances

- Sugar Cane Farmers Should Get 70% of Revenue, India Panel Says

- Iron-Ore Forecast Lowered at HSBC on Weakening Chinese Demand

- CO2 Storage May Aid Oil Company Revenue, Avoid Decommissioning

- Oil May Fall as Rising Output Boosts Stockpiles, Survey Shows

- Rubber in Shanghai Set to Extend Bull Rally: Technical Analysis

- Twin-Peak Rally Seen Boosting Grains in First Quarter of 2013

- Palm Oil Tumbles as Malaysia to Abolish Duty-Free Exports Quota

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

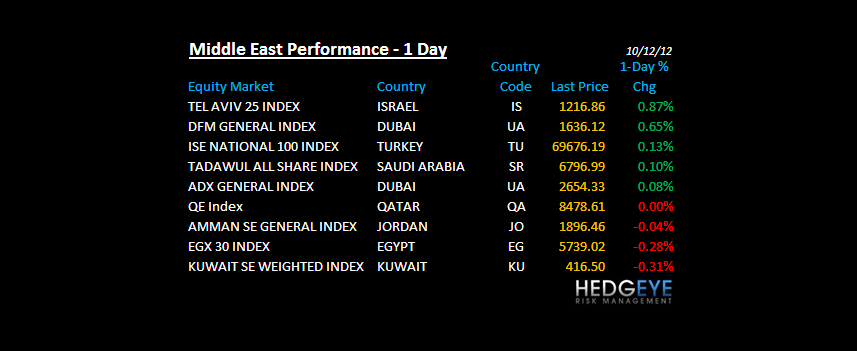

MIDDLE EAST

The Hedgeye Macro Team