This note was originally published October 11, 2012 at 13:48 in Financials

Key Drivers of the Quarter:

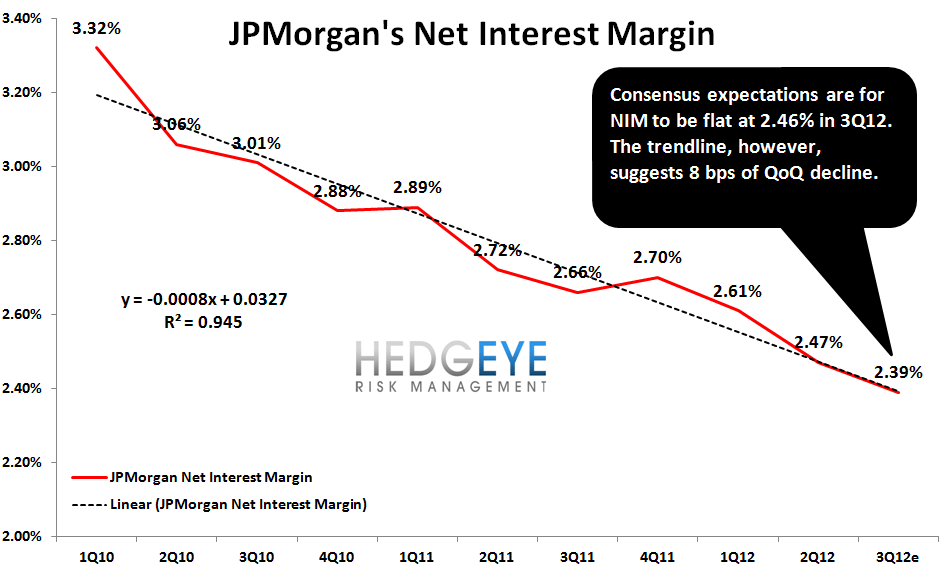

* NIM - Consensus is too bullish. Consensus is looking for 2.46% vs. last quarter's 2.47%. This may be optimistic. In the chart below we take a look at the trendline in JPMorgan's net interest margin since 1Q10. It's been decreasing at a rate of 8 bps per quarter, and should be at 2.39% in 3Q12. We realize the company chalked up a portion of 2Q12's NIM decline to hedge ineffectiveness that should reverse in 3Q. That's possible, and clearly what the street has modeled, but it's also possible that the ongoing QoQ compression in the yield curve robs them of another 8 bps.

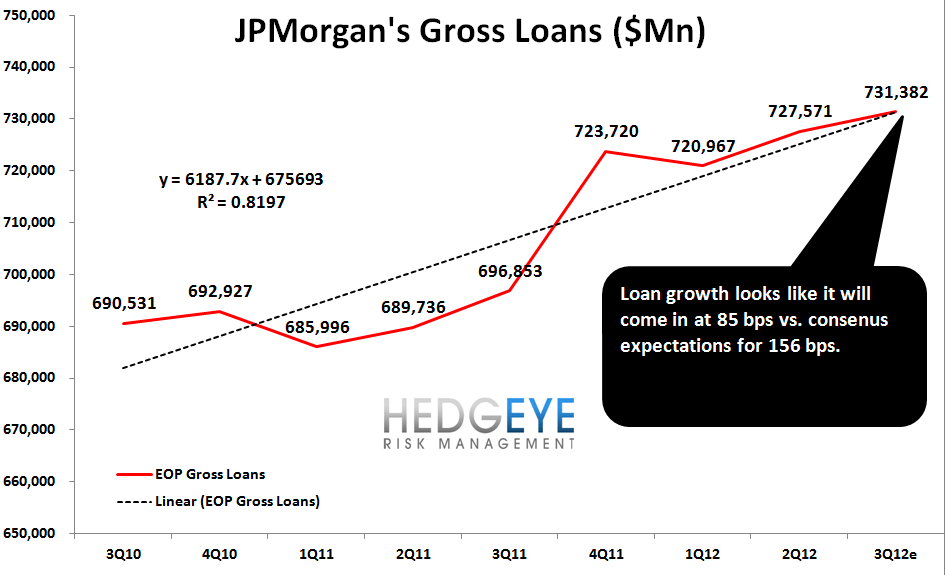

* Loan Growth - Consensus may be too bullish. Consensus is looking for 1.56% sequential loan growth, whereas the trend line would suggest 0.85% QoQ growth. It's certainly possible that the company could have chosen to originate and retain a larger amount of mortgages this quarter. It would make sense to do so - it would help both their NIM and loan growth, and they certainly wouldn't have had to compete aggressively to do so with mortgage volume up 70% YoY in 3Q. That said, the trendline suggests that Consensus is looking for roughly double what the company has delivered in the last 8 quarters.

* Net Interest Income - Consensus is too Bullish. With margin and loan growth expectations rather high, we think the product of those two variables is also too high. Consensus is modeling $11.32 billion in net interest income, but if we're right on margins (down 8 bps QoQ) and loan growth (+85 bps QoQ) then NII should look more like $10.84 billion. That shortfall of $478 million equates to around 8 cents per share after-tax. A more simplistic approach of just trend-lining the NII yields a slightly less pessimistic scenario of -$270 million, or 4-5 cents per share after tax (we show this in the chart below).

* Non-interest Income - Unclear. Consensus is looking for $13.02 billion, which is up $2 billion from $11.03 billion in 2Q12. Obviously the big wildcard here is how much is being modeled for further CIO losses and how much will there actually be. The company has said to expect another $1.7 billion in losses in a worst case scenario. It's unclear what the street is modeling on this line, making apples to apples comparisons difficult. Mortgage banking will be the other line that should show notable sequential change. We're estimating mortgage banking revenue may be higher by $250-500 million sequentially. Given the uncertainty around CIO, we think investors will be focused on the core numbers here. Outside of a potential CIO surprise (up or down), we see little reason to think non-interest will be a disappointment vs. expectations this quarter.

* Credit - Consensus is too Bearish. Consensus is looking for $1.37 billion in provision expense and $741 million in reserve release. As we published in our H8-based sector preview a few days ago, we think the Street is underestimating reserve release by almost 60%. Collectively, the street is looking for $2.3 billion in reserve release, whereas the H8 is suggesting a number closer to $5.4 billion. If we assume that as a proxy for JPMorgan, then the actual reserve release should be closer to $1.7 billion, or roughly $1 billion higher. This should add roughly 17 cents to the bottom line print vs. expectations.

*Opex - Consensus is about right. Consensus is modeling $15.45 billion in 3Q12 operating expense. This compares with 2Q12 opex of $14.97 billion. The company has given guidance on this line to expect operating expenses to be flat with 1H12 levels, which averaged $15.2 billion, exclusive of $3 billion in litigation reserve build. The rationale given was higher legal costs and mortgage production-related expenses, both of which seem to be playing out as expected based on the news flow intra-quarter. For reference, this is also fairly consistent with the last 10 quarters trendline, which would suggest a 3Q12 opex of $15.6 billion. As such, it looks like consensus may be overestimating operating expenses by roughly $250 million. Obviously there's the potential that the company is guiding conservatively here.

* Bottom line - Consensus is too Bearish. With all the big pieces being considered, it looks to us like the company will beat estimates by 4-8 cents net of one time items and DVA, primarily on reserve release (again). That said, there will be a eye-popping number of one-time items and adjustments necessary to get from the reported number to the real number. We think the JPMorgan print will set the tone for a generally positive 3Q12 earnings season from the Financials.

* Sector Strategic Outlook. As we see it, there are five key, positive tailwinds for the Financials and only one big headwind. The tailwinds we see are: (1) Political, Romney's momentum is finding its way into multiples, (2) Jobs, jobless claims are moving lower and have a tailwind through February, (3) Housing, collateral values are stabilizing and transaction activity is improving. Autocorrelation is the most important factor in housing, (4) QE Infinity, Financial stocks love QE for multiple reasons: it's inflationary, it bids up their securities holdings, (5) Earnings, as enumerated above, we think the earnings season will be, on balance, positive for the Financials. Against this, we see one very large risk: The Fiscal Cliff. Our macro team has written extensively on this subject.

From a timing standpoint, we see upside between here to the election driven by earnings, QE and the election, but after the election we would be very cautious until the market has a clear understanding of what to expect from Congress and the President on the Cliff.

Joshua Steiner, CFA

203-562-6500

jsteiner@hedgeye.com

Robert Belsky

203-562-6500

rbelsky@hedgeye.com