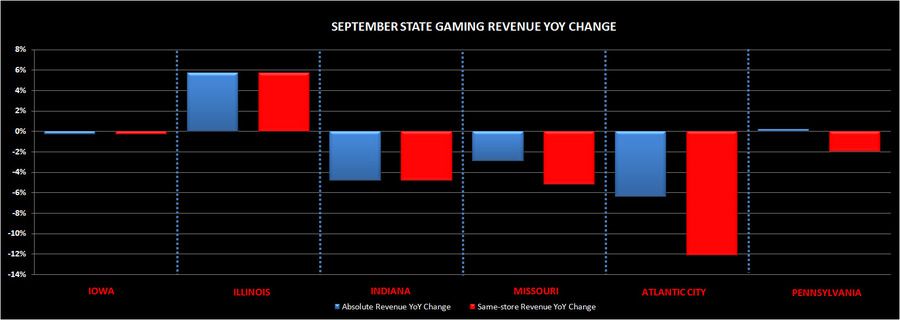

Down a Friday but up a Saturday and Sunday, we would’ve expected a 2-4% calendar boost. Yet, out of the six states that have released September gaming revenues, only Illinois – yes, Illinois – posted same-store revenue growth. Pennsylvania managed to eke out total gaming revenue growth but same-store growth in that market was negative. What’s going on?

Clearly, consumers are stretched but gaming seems to be underperforming other consumer sectors. We would argue that trends are sequentially getting worse. See chart below. Adjusted for seasonality, July and August were worse than the trend projected, and September looks like more of the same.

Clearly there is more going on than just a soft consumer. Here are some additional factors acutely impacting the gaming sector:

- New competition and market saturation – We’ve seen same-store revenues suffer hits from new properties, indicative of market saturation. New casinos in Ohio, PA, and Missouri are probably having an impact

- Gas prices – We’ve shown statistically that higher gas prices negatively impact regional gaming revenues

- Higher slot hold have masked lower volumes – Slot hold percentage has been on a consistent uptrend for years. We think higher “pricing” is unsustainable. Volumes have been under pressure for years.

- Younger generations not playing slots – We’ve shown that the average age of the slot player continues to increase among other discouraging demographic trends. The fact is, the post baby boomer generations are not playing slots. This is a problem longer-term but may be impacting slot play currently.

- Gaming is more discretionary than other consumer sectors

September probably needed to be a strong month for most of the regional gaming companies to make their Q3 earnings. It doesn’t look like it materialized so there is near-term earnings risk. We will be putting out earnings previews over the next week and we expect to be below consensus for most of the regional gaming companies.