Keith shorted KMTUY in Real Time Alerts

Levels:

TRADE resistance = 19.91

TREND = 21.63

Komatsu Exposed To Declines in Mining Equipment & Chinese Construction Investment

- KMTUY Like CAT…: Komatsu is heavily exposed to mining equipment capital spending, which appears to be slowing significantly. For a detailed review of our views on the mining capital investment cycle, please see CAT’s Deep Cycle.

- …But More China: Construction equipment sales have been in free fall in China, with CAT reporting that the market is off 40% yoy. Komatsu’s percentage of sales in China has dropped from over 20% to around 10%. The Chinese domestic market has become increasingly competitive and local inventories have been elevated.

- Valuation: Komatsu has a strong franchise, but remains overvalued from a cyclically-adjusted standpoint. We see the ADR fair value in the mid-teens with the potential for an overshoot if mining capital investment continues to weaken.

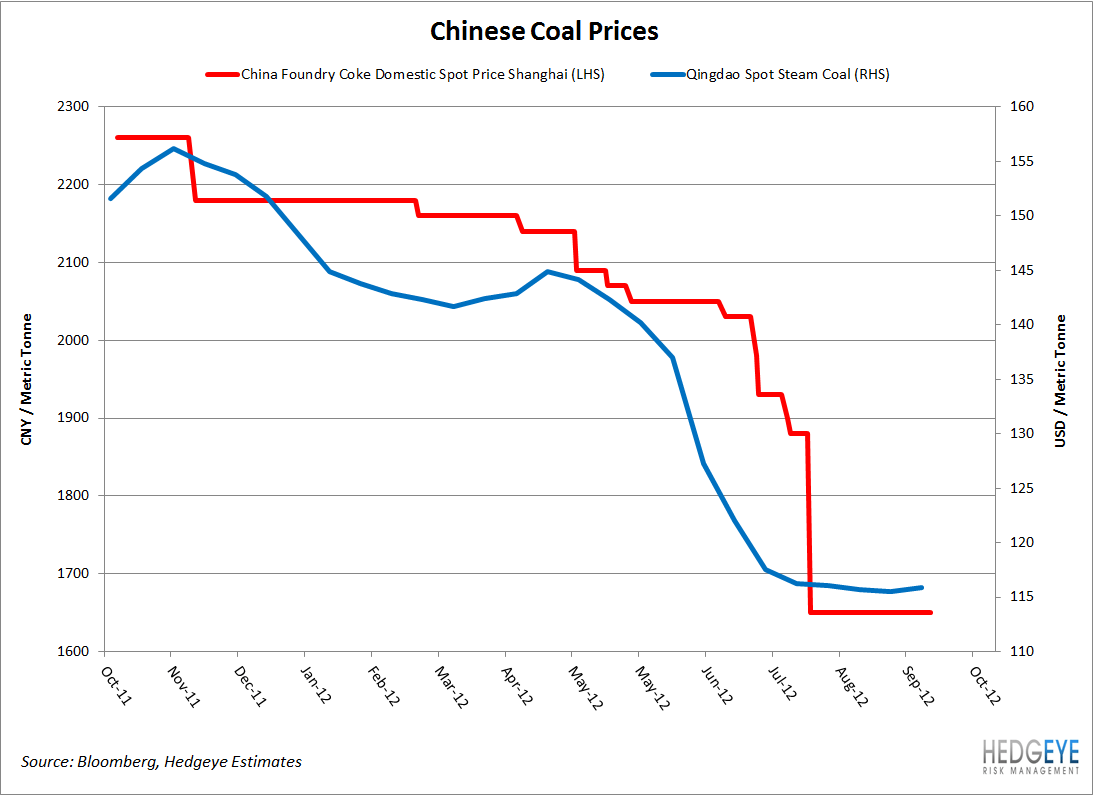

- Improved Data: Recent disconfirming evidence has been a sharp rebound in iron ore and Chinese steel prices. However, real Chinese rebar prices have only bounced to their 2009 lows. Coal prices, another key mining equipment end-market, have not rebounded. Commodity prices in China are an important indicator for mining investment, in our view.

Real Chinese rebar prices have bounced to the 2009 lows….

…but coal prices have not bounced.