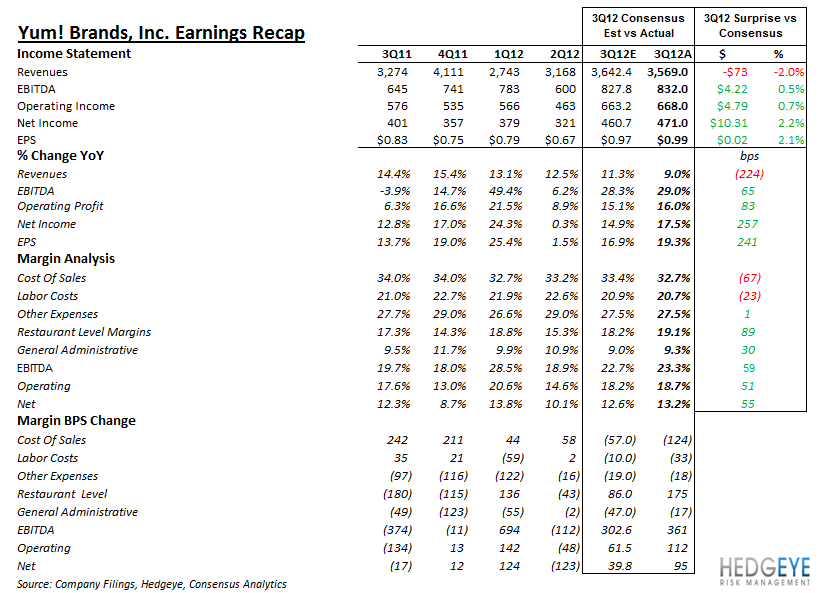

Yum! Brands reported $0.99 in EPS versus consensus expectations of $0.97. The China division drove almost three-quarters of the EBIT growth as lower COGS helped profitability in YUM’s most important market.

3Q Report Card

YUM is trading up 8.5% as, during the earnings call, management provided bullish commentary on China and the growth opportunity that market presents for the company’s brands. With that said, we view China’s volatile economy as the greatest risk in the stock. Management acknowledged this reality but came across as confident that China would continue to perform profitably. Historically, buying this stock on “China scares” has proved profitable, particularly over longer durations.

However, given difficult 4Q compares for YUM’s business in China and the persistence of concerning economic data from the region, we remain on the sidelines for the immediate-term TRADE. It is worth bearing in mind that YUM’s 3Q ended September 8th; the macro data for September, so far, pertaining to China were, generally, sub-consensus. Longer-term, this remains one of the best growth companies in the industry. From a fundamental perspective, depending on the macro backdrop, we would likely become more positive on the stock on an immediate-term basis at $65 per share.

Press Release & Earnings Call Details

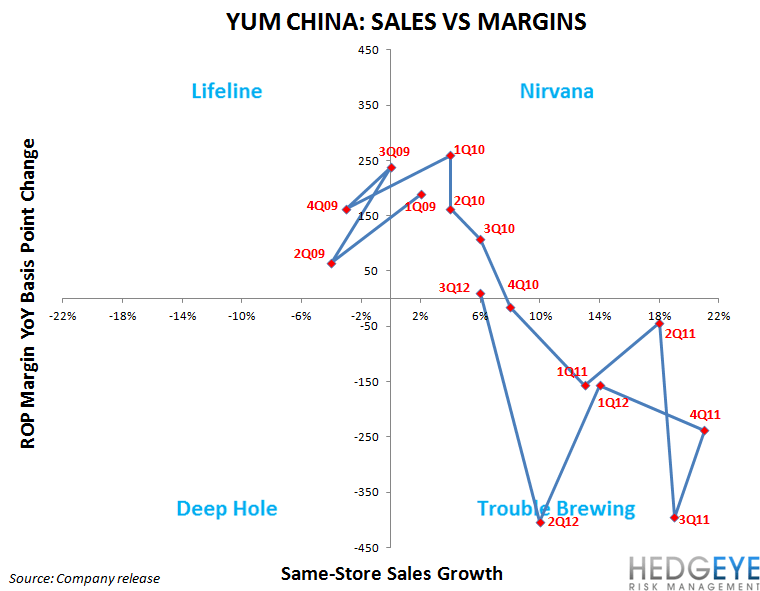

The China Division drove almost 75% of the consolidated EBIT growth of the company as unit count grew 18%, same-restaurant sales grew 6%, and restaurant level margins improved year-over-year on lower than expected food costs. Management expects China comps to be in the flat-to-low-single-digit range in the fourth quarter.

- Transactions declined 1% versus 27% growth in 3Q11

- Opening 750 restaurants in China this year (18% growth) versus initial expectation of 600

- Difficult to know how much of sequential slowdown in comps is due to economy

- Pizza Hut comps gained 8% in 3Q

- KFC comps gained 6% in 3Q

- 3Q labor inflation was 8%, commodity inflation was 2%

China Outlook

- 4Q is toughest SSS compare…expecting flat-to-LSD comps with 5% price (negative LSD transactions)

- Expecting slight y/y improvement in 4Q restaurant operating margins in China due to deflation in commodity prices

- Development focus is shifting from Tier 1 cities to lower tier (better returns, margins)

- Continuing 20% margins “over the long run”

- Current development rate is 18% which lowers SRS required in FY13 to hit earnings growth target

Potential Issues for the China Division

NEAR-TERM: Price cycling off the menu and sequential economic deterioration

INTERMEDIATE-TERM: Economic deterioration in excess of what management is anticipating

INTERMEDIATE-TERM: Management growing too fast. Currently, returns imply that “over-growth” is not yet a problem

The United States Division has gone from abysmal to impressive in little over a year. Whether or not this performance can be sustained remains to be seen. The US generated 6% in same-restaurant sales growth and management highlighted the completion of the KFC and Pizza hut refranchising as a positive.

- Doritos Locos Tacos and Cantina Bell have been key product introductions – should drive sales in FY13

- KFC sales and profits benefitting from new items and advertising

- Pizza Hut business in the US is stabilizing – added stores in 2011 after 10 years of unit decline

- Commodity costs were flat (below industry) in the U.S. due to supply chain initiatives

US Outlook

- 4Q will be weaker than YTD for US

- Overlap of 53rd week

- Lapping toughest comps of last year

- YTD refranchising of 340 restaurants in US will be profit dilutive in 4Q

- Ongoing growth model for the US calls for same-restaurant sale growth of 2-3%

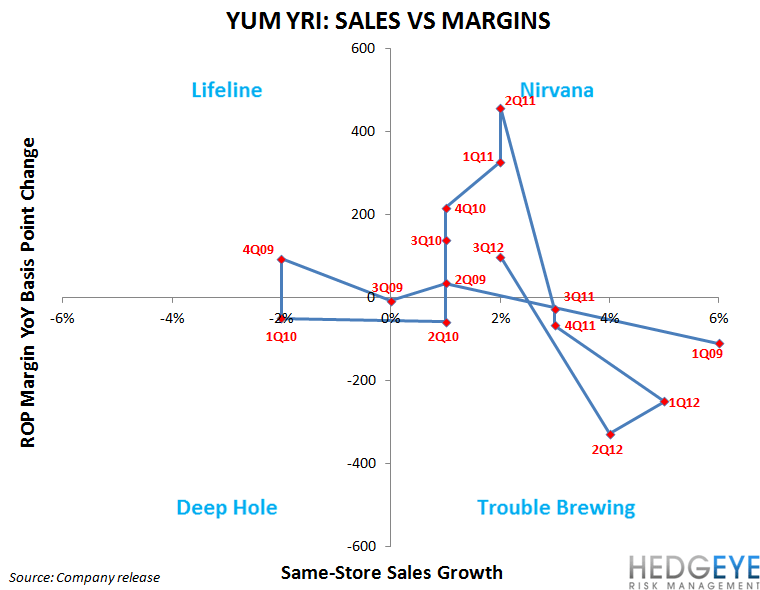

The YRI Division delivered same-restaurant sales growth of 2%, including 5% in emerging markets. Ramadan negatively impacted comps by 1%. The division drives roughly 8-9% of the company’s overall EBIT growth.

- Building 900 new units this year

- Opportunities in developed countries like France, Germany, Russia where YUM underpenetrated

- KFC Russia business improving dramatically, AUV’s at $1.8m from $1.2m two years ago

YRI Outlook

- 4Q comps should benefit by 1% due to Ramadan timing

- Positive earnings growth for YRI in 4Q offset by impact of lapping 53rd week in 2011

- Ongoing growth model for YRI calls for unit growth of 3-4% and SRS of 2-3%

- 45% of YRI units are in emerging markets

Howard Penney

Managing Director

Rory Green

Analyst