TODAY’S S&P 500 SET-UP – October 10, 2012

As we look at today’s set up for the S&P 500, the range is 30 points or -0.52% downside to 1434 and 1.56% upside to 1464.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 10/09 NYSE -1639

- Decrease versus the prior day’s trading of -601

- VOLUME: on 10/09 NYSE 612.52

- Increase versus prior day’s trading of 31.94%

- VIX: as of 10/09 was at 16.37

- Increase versus most recent day’s trading of 8.34%

- Year-to-date decrease of -30.04%

- SPX PUT/CALL RATIO: as of 10/09 closed at 2.35

- Up from the day prior at 1.87

CREDIT/ECONOMIC MARKET LOOK:

TREASURIES – almost all of the time, bonds would rip w/ US stocks falling for 3 straight days – not this time; so respect the market move as it looks like oversold in stocks into JPM earnings Friday could be the tell here; not sure – need to see more data.

- TED SPREAD: as of this morning 25.04

- 3-MONTH T-BILL YIELD: as of this morning 0.10%

- 10-Year: as of this morning 1.74%

- Increase from prior day’s trading of 1.71%

- YIELD CURVE: as of this morning 1.47

- Up from prior day’s trading at 1.45

MACRO DATA POINTS (Bloomberg Estimates)

- 7am: MBA Mortgage Applications (prior 16.6%)

- 10am: JOLTS Job Openings (Aug.) est. 3735, prior 3664

- 10am: Wholesale Inventories (Aug.) est 0.4%, prior 0.7%

- 10:30am: EIA Weekly petroleum status report

- 11am: U.S. Fed to sell notes

- 11:30am: U.S. to sell $40b in 4-week bills

- 2pm: Fed’s Beige Book

- 2:45pm: Fed’s Kocherlakota speaks in Montana

- 4:30pm: API Energy Inventories

- 4:30pm: Fed’s Tarullo speaks in Philadelphia

- 4:45pm: Fed’s Fisher speaks at Cato Conference in Washington

GOVERNMENT:

- Commerce Dept. announces anti-dumping duties on Chinese solar-energy imports

- G-7 finance ministers meet in Tokyo

- Citigroup’s global head of commodities research, Edward Morse, speaks at DOE “Winter Fuels Outlook” conference. Other speakers include EIA Administrator Adam Sieminski, 8:30am

- CFTC Chairman Gary Gensler, Futures Industry Association President Walter Lukken, SEC Senior Special Counsel Matthew Daigler discuss derivatives regulation under Dodd-Frank, 8:30am

- Commerce Dept., National Telecommunications and Information Administration holds stakeholder meeting to develop consumer data privacy codes of conduct on mobile apps, 9:30am

- Space Exploration Technologies Corp., led by billionaire Elon Musk, will attempt to attach its Dragon spacecraft to the International Space Station, 7:30am

WHAT TO WATCH:

- FedEx to make public today details about goal to boost profit by $1.7b within three years, at meeting starting at 9am NY time

- True Religion may announce plans to be sold as soon as today, private-equity firms, clothing cos. have expressed interest: WSJ

- Toshiba will pay ~125b yen ($1.6b) to acquire Shaw Group’s 20% stake in co.’s nuclear power unit Westinghouse Electric

- Alcoa cut forecast for global consumption of aluminum by 1 ppt on slowing Chinese demand

- Chinese passenger-vehicle sales unexpectedly shrank for 1st time in 8 mos.

- EADS, BAE Systems may determine fate of planned combination by 5pm in London today

- Morgan Stanley, Mitsubishi UFJ CEOs may meet Oct. 13 in Tokyo to discuss deepening their partnerships

- Microsoft cut fiscal 2012 bonus for CEO Steve Ballmer, citing slower-than-planned progress in online services division, failure to comply with pact with European regulators

- Peter Muller’s PDT hedge fund said to raise more than $500m from Blackstone

- RBS said to agree to sell two buildings in Frankfurt, Berlin to Axa Investment Managers, valued at $1b

- Disney’s ABC network, Buena Vista Television units will ask federal appeals court to overturn $319m judgment won 2 years ago by U.K. creators of “Who Wants to Be a Millionaire”

- Trades that caused disruptions in ~140 cos., ETFs canceled after review by firm that reported them

- Lone Star Funds, Kennedy-Wilson Holdings said to be among remaining bidders for parts of ~EU2b of mainly Irish real estate loans Lloyds Banking is selling

- H&R Block may drop designation as savings and loan holding co.

- EBay, Amazon.com’s sales growth slowed in Sept.

- BlackRock’s Laurence Fink said policy makers should plan global bank resolution system that would respond to deteriorations in capital sooner

- Drought damage to corn, soybean fields in U.S. eroding supplies to below consumption Y/y for 1st time since 1974

- U.S. cos. doing business in China less optimistic than 3 yrs ago, according to U.S.-China Business Council survey

EARNINGS:

- Host Hotels & Resorts (HST) 6am, $0.21

- Jean Coutu Group (PJC/A CN) 7am, C$0.22

- Helen of Troy Group (HELE) 7:30am, $0.85

- Progressive (PGR) 8:30am, $0.26

- Ruby Tuesday (RT) 4:01pm, $0.07

- Adtran (ADTN) After-mkt, $0.19

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Alcoa Cuts Global Aluminum Demand Forecast on China Slowdown

- Greece Welcomes Gold Miners to Rank First in Europe: Commodities

- Japan Easing Restrictions on U.S. Beef, Paving Way for Tyson

- Oil Trades Near One-Week High as Mideast Risk Counters Slowdown

- China’s Gold Imports From Hong Kong Slump as Price Deters Buyers

- Palm Oil Stockpiles in Malaysia Surge to Record as Output Climbs

- Soybeans Slide as Harvest Progress Eases Concern About Supply

- Spot Gold Climbs 0.2% to $1,767.25/Oz, Erasing Earlier Decline

- Cocoa Resumes Fall as Data May Signal Weak Demand; Coffee Rises

- Gold Best of Biggest ETFs as Traders Seek Haven: Riskless Return

- Romney’s Farm Policy Restates Republican Positions, Analysts Say

- Drought Cuts U.S. Crops Below Demand First Time in 38 Years

- China Piped Gas Imperils $100 Billion LNG Plans: Energy Markets

- Rubber Declines on Europe Debt Crisis, Slowing China Car Sales

CURRENCIES

USD – don’t look now, but the most asymmetric trade in all of Global Macro is going our way; Romney mo + Euro slow + Japanese money printing pending = USD mo mo; USD now up for 3 of the last 4 wks but finally signaling immediate-term TRADE overbought here, which should but in a base of support for stocks, gold, oil, etc.

EUROPEAN MARKETS

ASIAN MARKETS

JAPAN – Nikkei gets crushed overnight, down another -2% (down -16.2% since #GrowthSlowing started, globally, in March), and the Chinese aren’t going to the IMF meetings because they are being hosted by Japan. FX War = On; short the Yen.

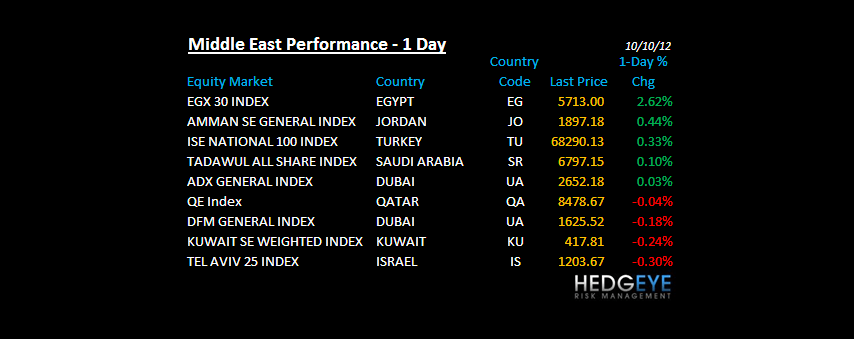

MIDDLE EAST

The Hedgeye Macro Team