-- For specific questions on anything Europe, please contact me at to set up a call.

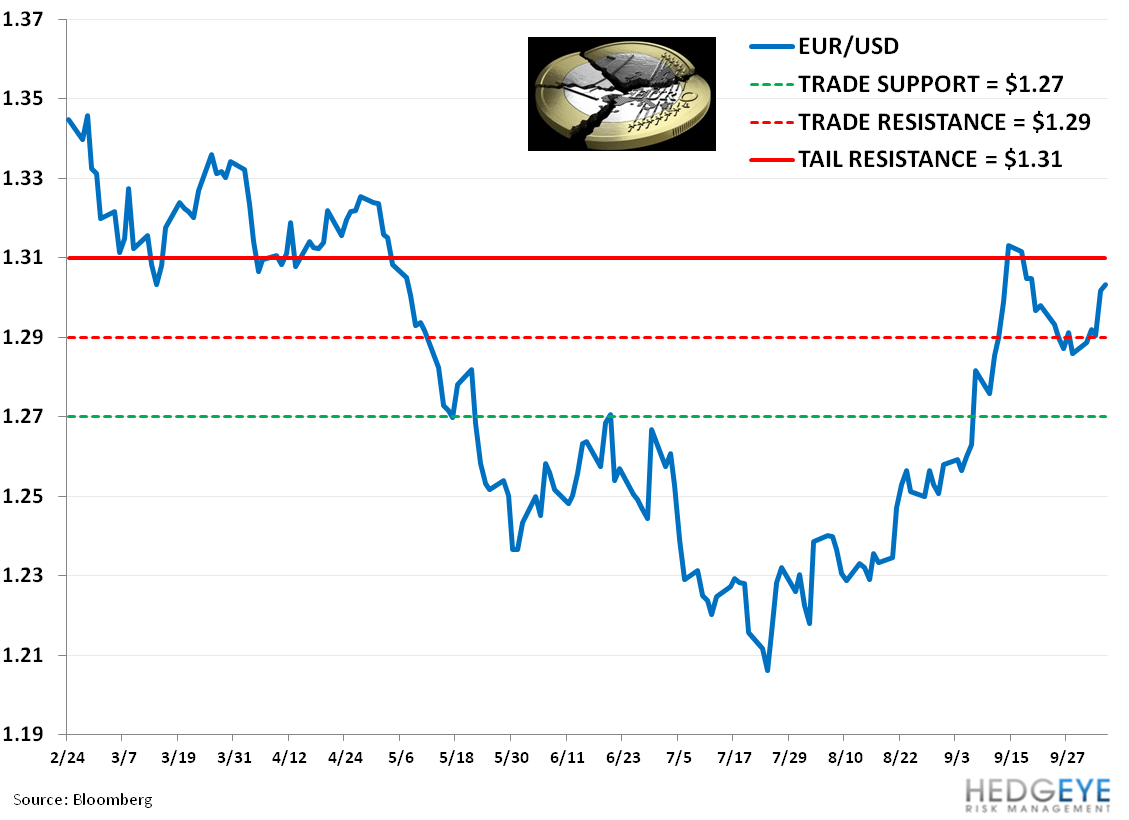

Positions in Europe: Short EUR/USD (FXE); Long German Bonds (BUNL)

Asset Class Performance:

- Equities: The STOXX Europe 600 closed up +2.1% week-over-week vs -2.6% last week. Top performers: Cyprus +19.0%; Greece +12.3%; Italy +5.2%; Austria +4.0%; Portugal +3.6%; Czech Republic +3.4%; Spain +3.2%; France +3.0%; Netherlands +2.9%. Bottom performers: Ukraine -4.4%; Russia (RTSI) -0.4%. [Other: Germany +2.5%; UK +2.2%].

- FX: The EUR/USD is up +1.33% week-over-week. W/W Divergences: PLN/EUR +1.13%; CZK/EUR +1.02%; HUF/EUR +0.91%; ISK/EUR +0.80%; DKK/EUR -0.02%; CHF/EUR -0.20%; NOK/EUR -0.59%; RON/EUR -0.67%; GBP/EUR -1.42%; SEK/EUR -1.89%.

- Fixed Income: The 10YR yield for sovereigns were lower for the peripheral on the week, while the core rose marginally. Portugal declined the most week-over-week at -68bps to 8.32%, followed by Greece -50bps to 19.0% and Spain -27bps to 5.78%. France gained the most at +10bps to 2.28% on the week and Germany gained +6bps to 1.82%.

- Sovereign CDS: Sovereign CDS were lower on the week. On a week-over-week basis Italy led the charge, declining -44bps to 318bps, followed by Portugal -41bps to 476bps, Spain -37bps to 355bps, and Ireland -34bps to 289bps.

The European Week Ahead:

Sunday – Sep. Germany Wholesale Price Index (Oct. 7-12)

Monday - Eurogroup Meeting in Luxembourg (Oct. 8-9); Oct. Eurozone Sentix Investor Confidence; Aug. Germany Imports, Exports, Current Account, Trade Balance, Industrial Production; Sep. UK BRC Sales Like-For-Like, RICS House Price Balance; Sep. France BoF Business Sentiment

Tuesday – Aug. UK Industrial Production, Manufacturing Production, Visible Trade Balance, Total Trade Balance; Aug. France Central Government Balance, Trade Balance; Aug. Spain House Transactions; 2Q Italy Deficit to GDP; Sep. Greece Consumer Price Index

Wednesday – Aug. France Industrial Production, Manufacturing Production; Aug. Italy Industrial Production; Sep. Greece Industrial Production

Thursday – Oct. Bloomberg Economic Survey for the Eurozone, Germany, UK, France, Spain, Italy and Greece; ECB Publishes Monthly Report; Sep. Germany Consumer Price Index – Final; Sep. France Consumer Price Index; Sep. Spain Consumer Price Index – Final; Sep. Italy Consumer Price Index Jul. Greece Unemployment

Friday – Aug. Eurozone Industrial Production; Aug. France Current Account; Italy CPI - Final

Call Outs:

Greece - Greek Prime Minister Samaras said in an interview with the German business daily Handelsblatt that Athens will run out of cash in November if the troika does not approve the next installment (~€31B) of its support package. Note that Athens and the troika have yet to even reach an agreement on a €13.5B package of spending cuts and tax measures over the next two years.

Germany - Germany's claims on the Eurosystem's Target2 system fell to €695.5B at the end of September from €751B at the end of August, the lowest level since April.

Germany - Is pushing the EU to improve proposals for a Eurozone banking supervisor so that countries outside of the EUR might be persuaded to join.

Spain - Bank of Spain Governor Luis Maria Linde said that the government's budget forecasts for the economy and tax income look optimistic, adding that deficit reduction targets (which Madrid reiterated just last week) may be missed. He told parliament that the economy would likely contract by -1.5% next year, while the government's budget is based on a -0.5% contraction.

Spain - Moody's said on Monday that Spanish banks face a capital shortfall of €70B-€105B (almost 2x the estimate from the stress test results on Friday). The test used a 6% core capital ratio under a stressed scenario, while the ratings firm assumed capital ratios of 8-10%.

Portugal - The government unveiled what it described as "enormous" tax increases to help keep the bailout program on track. The measures include an additional 4% tax on 2013 earnings, an increase in the average income tax rate to 11.8% from 9.8% and new taxes on capital income and homes worth more than €1M - will replace a "fiscal devaluation" program that the government was forced to scrap due to anti-austerity protests.

Portugal - Completed a €3.76B bond swap on Wednesday. It purchased bonds maturing in September 2013 and sold bonds maturing in October 2015. It was the country's first foray into the bond market since it requested a bailout last year. Recall that Portugal has to meet a September 2013 bond redemption of ~€10B without the support of its rescue program. In addition, the ECB has established the process of returning to the bond market as a condition for its new intervention program.

ECB and Banking Authority - ECB Executive Board member Joerg Asmussen said on Monday that the ECB will not rush through "half-baked" plans for a new pan-European supervisor.

Cyprus - Plans to seek an €11B bailout, or ~ 62% of the country's GDP. It added that the funds will be used to recapitalize its banks and pay its bills. Recall that when Cyprus became the fifth Eurozone country to seek aid in late-June, no amount was specified for the rescue.

Data Dump:

Eurozone Unemployment Rate 11.4% AUG vs 11.4% JUL (revised from 11.3%)

Eurozone Retail Sales -1.3% AUG Y/Y (exp. -1.9%) vs -1.4% JUL [0.1% AUG M/M (exp. -0.1%) vs 0.1% JUL]

Eurozone PPI 2.7% AUG Y/Y vs 1.6% JUL [0.9% AUG M/M vs 0.3% JUL]

German Factory Orders -4.8% AUG Y/Y (exp.-4.3%) vs -4.6% JUL [-1.3% AUG M/M (exp. -0.5%) vs 0.3% JUL]

German Machinery Orders (VDMA) -11.0% AUG Y/Y vs -2.0% JUL

Germany VDIK New Passenger Car Registrations -11.0% SEPT Y/Y

French Car & Light Vehicle Registrations -17% SEPT Y/Y to 166,891

Italy Unemployment Rate 10.7% AUG vs 10.7% JUL

Spain Jobless +1.7% SEPT Y/Y to 4.7M vs August +0.83%

Spain Industrial Output WDA -3.2% AUG Y/Y vs -5.5% JUL (down for 12th straight month)

UK New Car Registrations 8.2% SEPT Y/Y vs 0.1% AUG

UK M4 Money Supply-4.1% AUG Y/Y vs -4.6% JUL

UK Nationwide House Prices -1.4% SEPT Y/Y (exp. -0.7%) vs -0.7% AUG [-0.4% SEPT M/M vs 1.1% AUG]

UK Halifax House Prices -1.2% SEPT Y/Y vs -0.9% AUG

UK PMI Construction 49.5 SEPT (exp. 49.9) vs 49 AUG

Switzerland Retail Sales 5.9% AUG Y/Y vs 2.9% JUL

Ireland Unemployment Rate 14.8% SEPT vs 14.8% AUG

Ireland Consumer Confidence 60.2 SEPT vs 70 AUG

Netherlands CPI 2.5% SEPT Y/Y vs 2.5% AUG

Belgium Unemployment Rate 7.4% AUG vs 7.5% JUL

Ireland Industrial Production -0.6% AUG Y/Y vs -4.2% JUL

Denmark Industrial Production -2.3% AUG M/M vs 4.4% JUL

Norway Industrial Production WDA 5.6% AUG Y/Y vs 7.6% JUL

Romania Producer Prices 7.2% AUG Y/Y vs 5.7% JUL

Romania Retail Sales 4.7% AUG Y/Y vs 4.4% JUL

Russia CPI 6.6% SEPT Y/Y vs 5.9% AUG

Estonia CPI 3.8% SEPT Y/Y vs 3.8% AUG

Czech Republic Retail Sales -0.8% AUG Y/Y vs 0.3% JUL

Hungary Industrial Production (Preliminary) 1.4% AUG Y/Y vs -2.2% JUL

Romania Q2 GDP Final 0.5% Q/Q [UNCH vs previous estimate]; 1.1% Y/Y [vs 1.2% initial]

Romania Industrial Sales 4.7% AUG Y/Y vs 5.0% JUL

Turkey CPI 9.19% SEPT Y/Y vs 8.88% AUG

Turkey PPI 4.03% SEPT Y/Y vs 4.56% AUG

Interest Rate Decisions:

(10/3) Poland Base Rate Announcement UNCH at 4.75 [consensus expected 25bps cut]

(10/3) Iceland Sedlabanki Interest Rate UNCH at 5.75%

(10/4) BOE UNCH at 0.50% and asset purchase program UNCH at 375 B GBP

(10/4) ECB UNCH at 0.75% (Deposit Facility UNCH at 0.00%)

(10/5) Russia Refinancing Rate UNCH at 8.25% [as expected]

(10/5) Russia Overnight Deposit Rate UNCH at 4.25%

(10/5) Russia Overnight Auction-Based Repo UNCH at 5.50%

Matthew Hedrick

Senior Analyst