A weak dollar over the last week was partly behind the higher commodity prices, generally, on a week-over-week basis. Coffee prices remain favorable year-over-year, while grains, proteins, and dairy costs are likely to squeeze un-hedged restaurant operators over the next couple of quarters. On the short side, we are targeting stocks like BLMN and TXRH where we think commodity inflation will be difficult to mitigate from a top-line perspective should our stance that, for each company, top line growth should come in below expectations.

Summary View

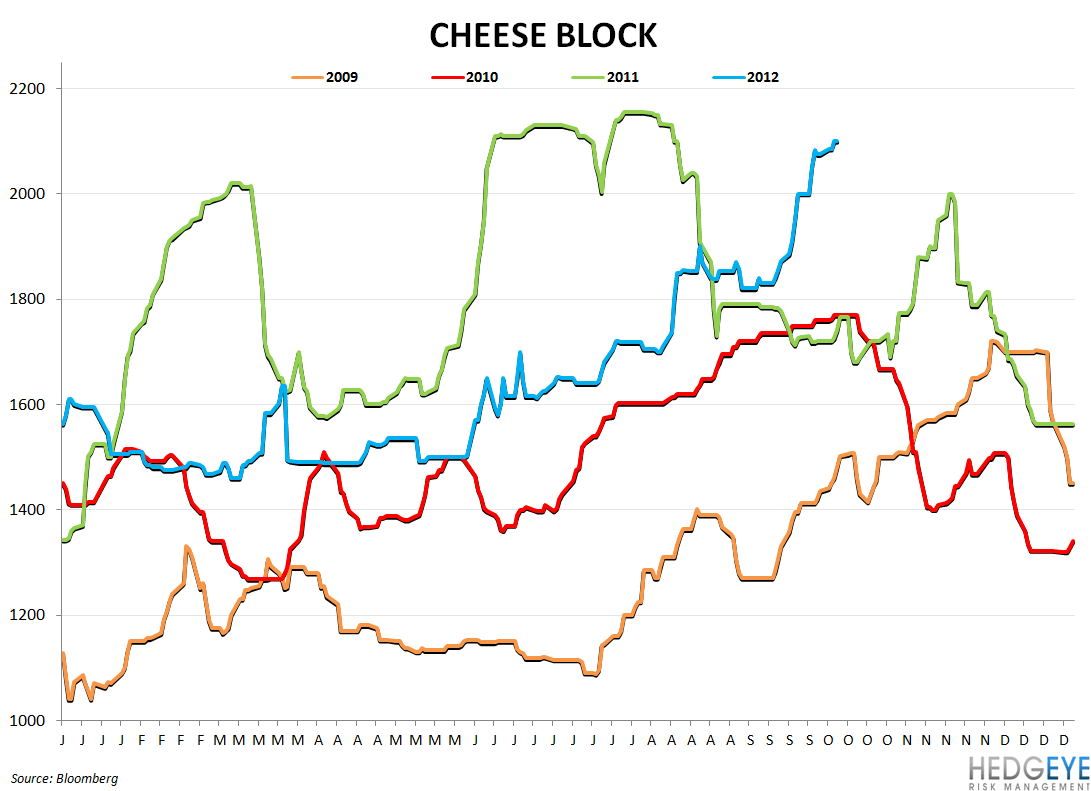

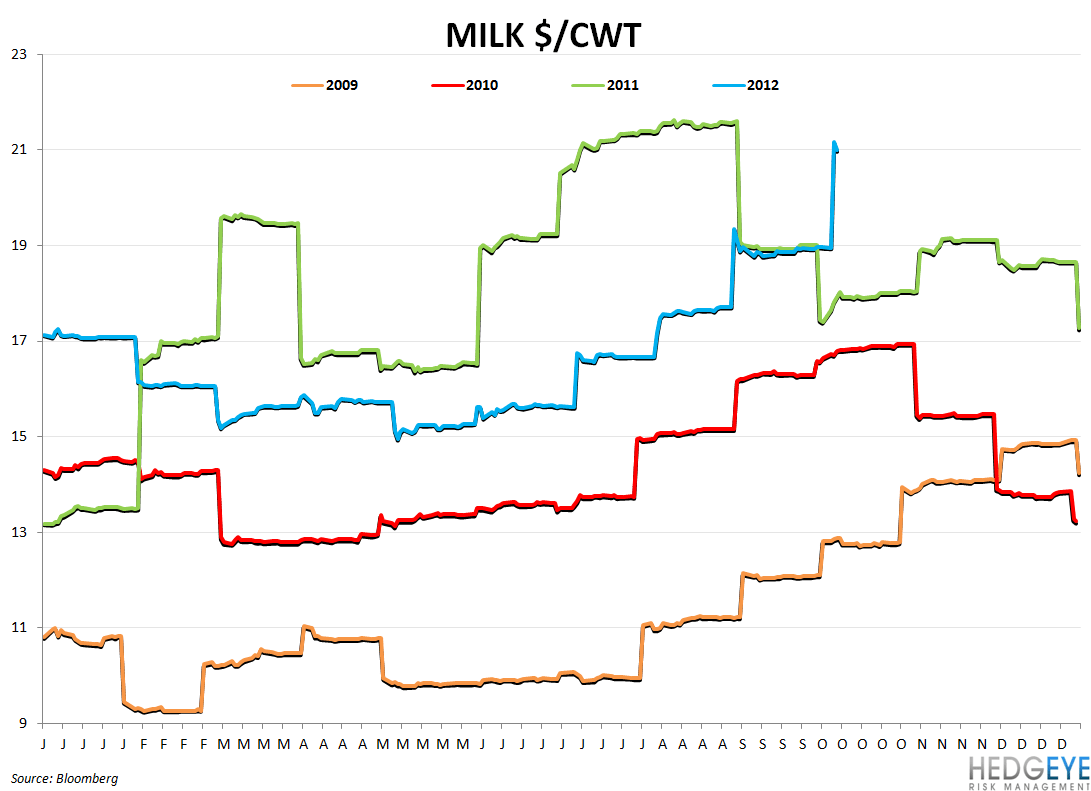

Dairy prices are up ~20% versus a year ago as concerns mount over shrinking herd sizes in the United States. A CME report released this week indicated that the percentage of dairy cows being moved to slaughter is growing and some estimate that a new record high could be achieved when the January 1 inventory report is released by the USDA. We see this as a negative for CAKE, TXRH, CMG, and SBUX (SBUX has guided to dairy headwind in FY13). PZZA have their cheese costs hedged but to the extent that dairy prices continue higher, the company’s commodity costs could rise from here.

Beef prices were flat over the last week as weak economic data and a decline in year-over-year slaughter numbers for cattle YTD. This article explains that this lesser rate of slaughter is not as bearish a sign as it may seem, given the longer term context and extreme slaughter rates in 2011.

Longer-term, our view is that beef prices are likely to remain at elevated levels. Higher feed costs are reducing the number of cattle on feedlots versus a year ago and herd sizes remain depleted after the last two years of drought. It seems that supplies of beef are set to remain tight for at least a couple of years. This is a negative for BLMN, TXRH, CMG, JACK, and WEN, among others.

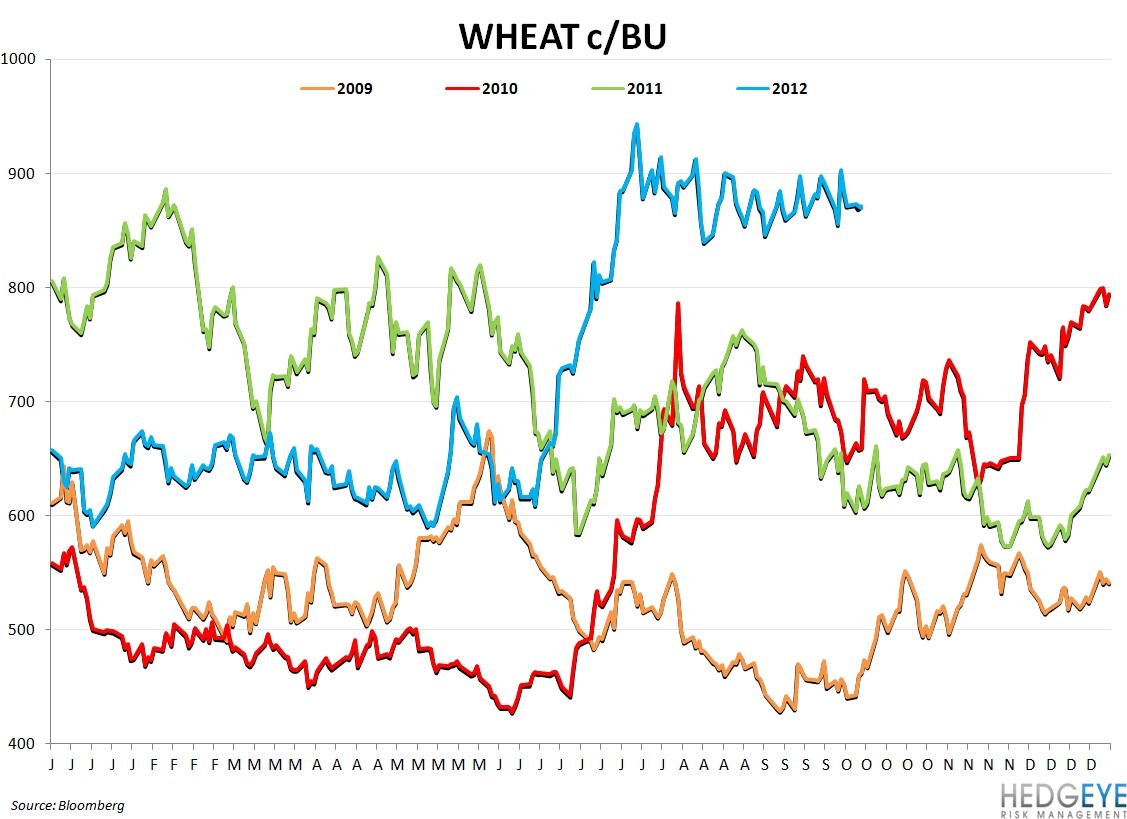

Grains were mixed over the past week largely as a result of the details within the USDA Grain Stocks report released last Friday. Corn and wheat futures traded sharply higher on the report, which indicated that ending stocks for 2011/12 were below and at the low end of estimates for corn and wheat, respectively. Soybean stocks were above estimates and the September WASDE projection; soybean prices have declined -1.2% over the last week. Overall, grain prices remain elevated and, along with energy prices, are squeezing food processor margins. Ultimately, this is leading to higher costs for food retailers, restaurants, and consumers.

Gasoline

Refinery and pipeline shutdowns are increasing concern that supplies are not adequate to meet demand. Gasoline and other commodity-based expenses are squeezing the American consumer. As we have written in recent posts, we view this inflation as having a negative impact on growth in consumer spending and believe that consensus expectations for same-restaurant sales growth are – in many cases – overly optimistic. Gas prices are up 11% year-over-year.

Correlation

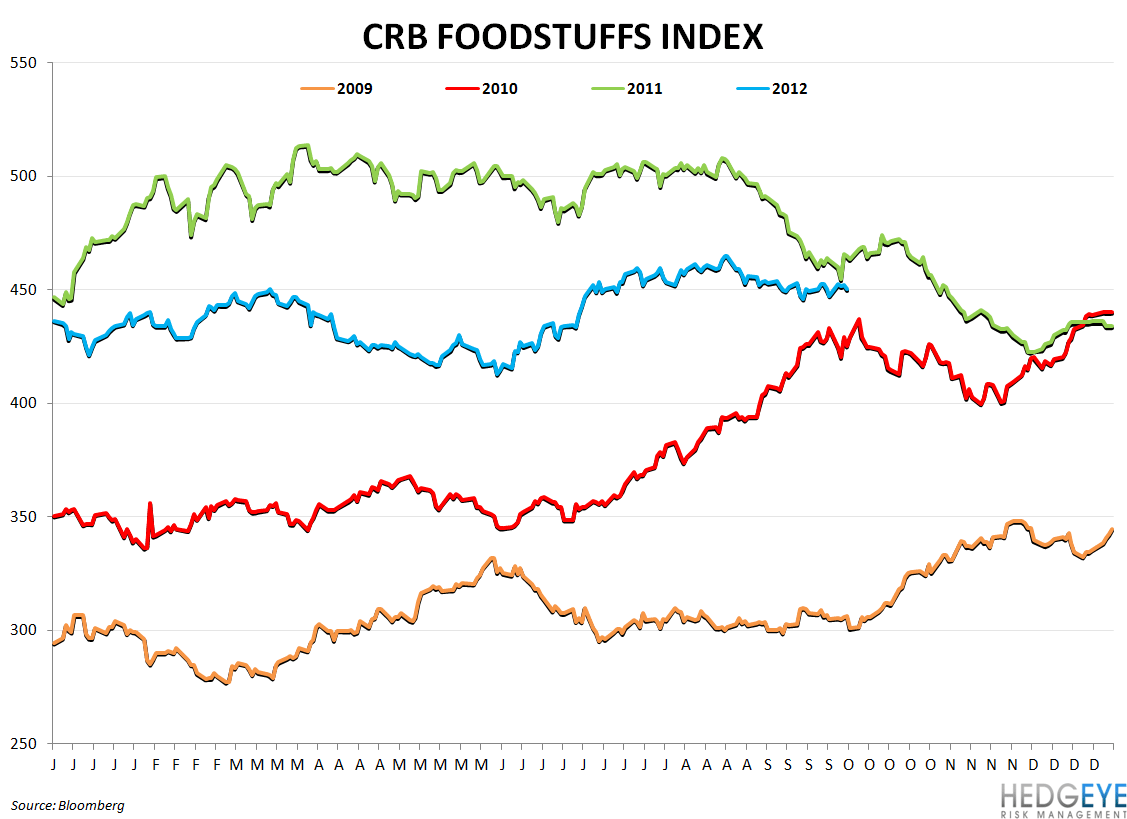

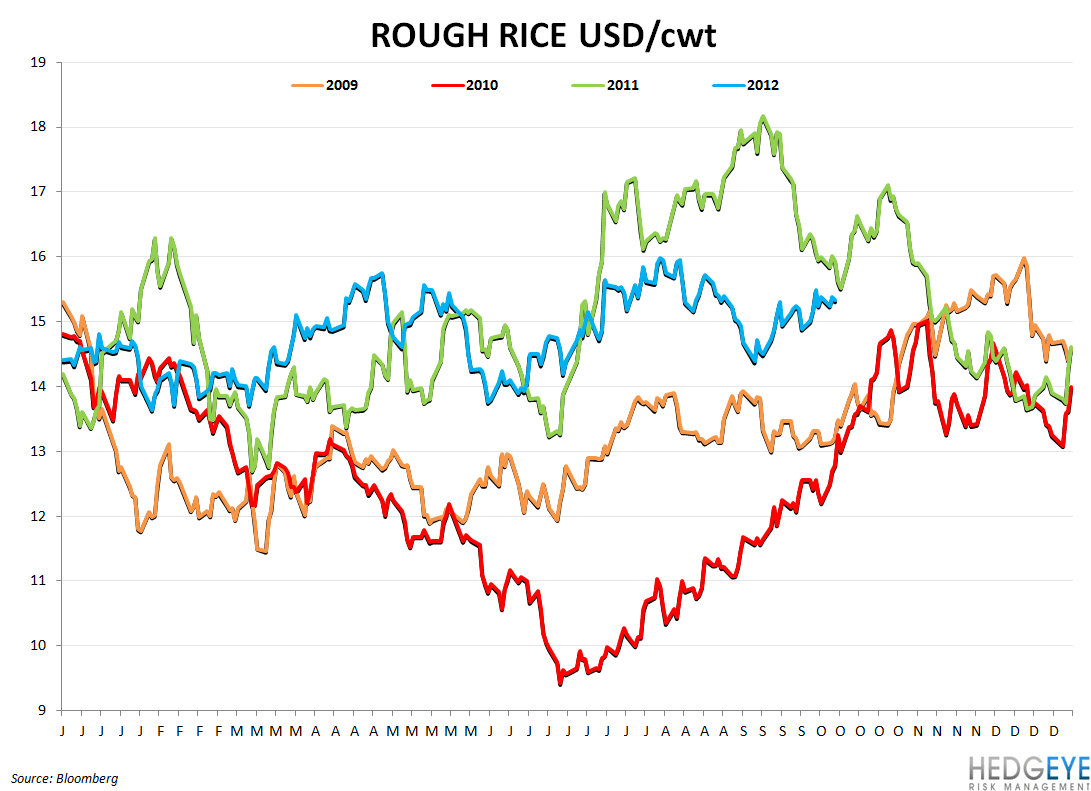

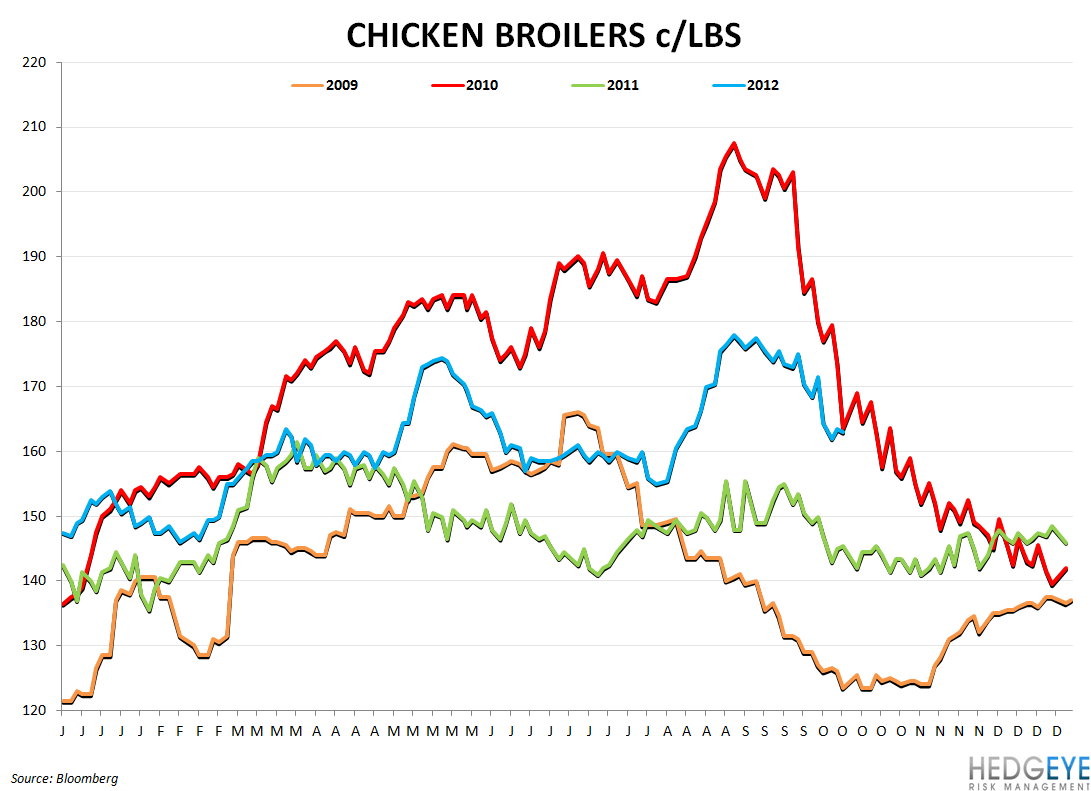

Charts

Howard Penney

Managing Director

Rory Green

Analyst