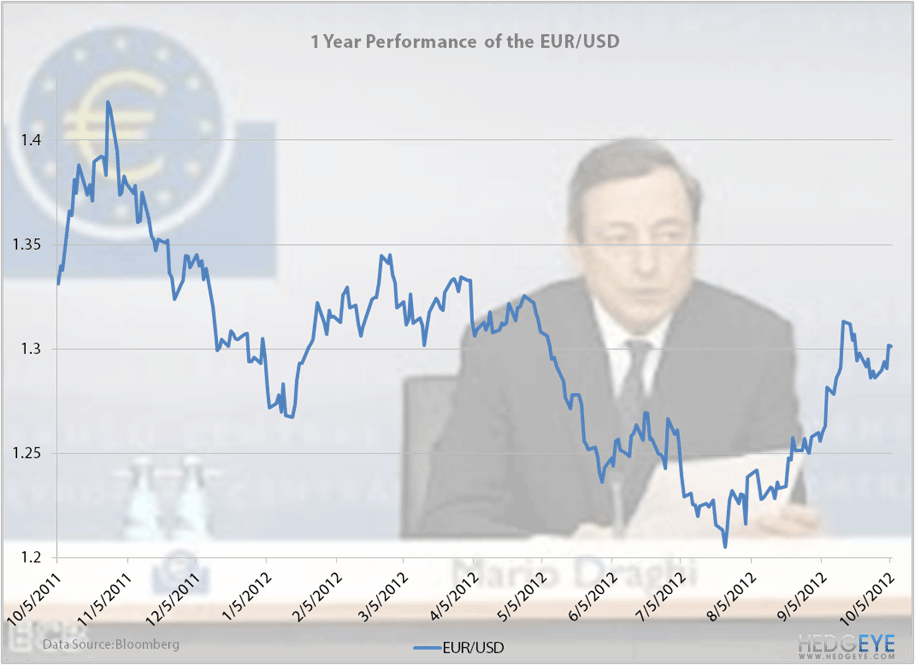

Our chart below showcases the performance of the EUR/USD currency pair over the past year. You can easily spot some of the big events that occurred in 2012: the turmoil of Spain and Italy over the summer, the late July "whatever it takes" comments by Mario Draghi and of course, the "unlimited' buying remark made on September 6 that really kicked the Euro into high gear.

It reminds us of charts we've displayed in the past showing Bernanke's effects on various markets. This is just the European version.