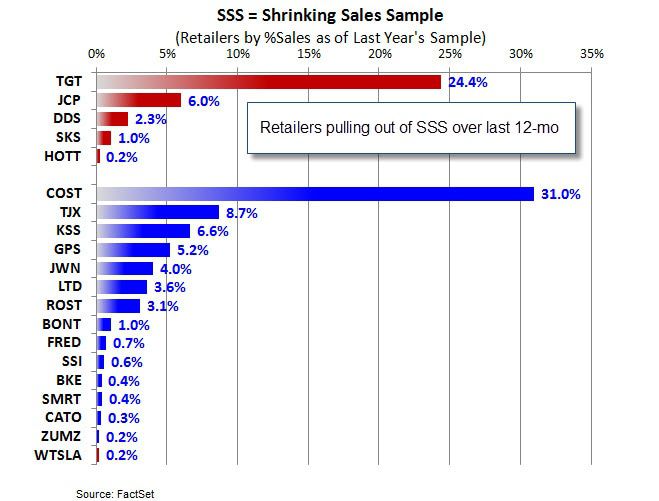

The biggest callout of this morning’s Retail Sales day is the simple fact that this is a legacy process and one that isn’t likely to be in practice a year from now. TGT announced that January will be its last monthly sales report just two months after SKS went dark. We’re now down to 16 companies compared to 21 this time last year. More notable is the size of the parties departing the practice (TGT, JCP, DDS, SKS, HOTT) which accounted for 34% of the SSS sample this time last year. This monthly exercise is clearly losing its relevance.

Back to the results, which were weaker compared to last month as largely expected with 9 companies coming in ahead of expectations compared to 8 misses – a notable deceleration from the favorable 15:1 August mix. Here are a few callouts worth noting:

- What catches our eye is the distribution of results within retail. Apparel retailers came in mixed with a positive skew, Broadlines (COST/TGT) came in clean ahead of expectations, while Department/Dollar stores fell short across the board with the sole exception of SSI.

- The off-pricers (ROST/TJX) continue to outperform and were the only companies to raise their outlook (though TJX had keep prior guidance in check due to an unexpected pension charge).

- KSS’s bet on taking on inventory to drivetraffic clearly hit a snag in execution.

- The fact that Q3 expectations weren’t tempered as a result sets un unrealistic bar in our view. Sept comps were the toughest of the quarter, but Oct is not much different implying a substantial acceleration in 2yr trends to hit guidance of +0%-2% - not likely.

- Moreover, with higher inventory levels we think SG&A is the lever that can get KSS to their EPS for the quarter not gross margin upside – not dissimilar to last quarter. The trend in earnings quality of late is concerning.

- Lastly, the fact that KSS’ top competitor is hemorrhaging over $3Bn in share and it’s comping down is just embarrassing.

- To that end, the slight miss at Macy’s despite a more favorable setup is less than impressive while GPS is reminiscent of the kid in the corner at a holiday party stuffing chocolates in their mouth.

- Aside from the off-pricers, GPS has arguably been the greatest benefactor of the JCP retailer stimulus which it has propped up its US Gap and Old Navy business. Our estimates suggest that GPS may have realized as much as a 3pt lift to total comp of in 1H, which would account for the majority of 1H growth. This is another quarter or two away from being fully realized.

- Comps rolled across all concepts with only Old Navy improving on a 2yr basis (Mr. Johnson your fruit basket is in the mail). This matters with Old Navy accounting for 33% of sales, but that tailwind is decelerating.