Positions in Europe: Long German Bonds (BUNL)

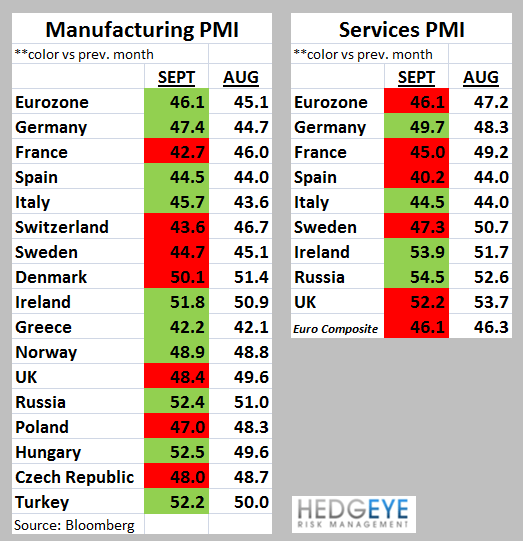

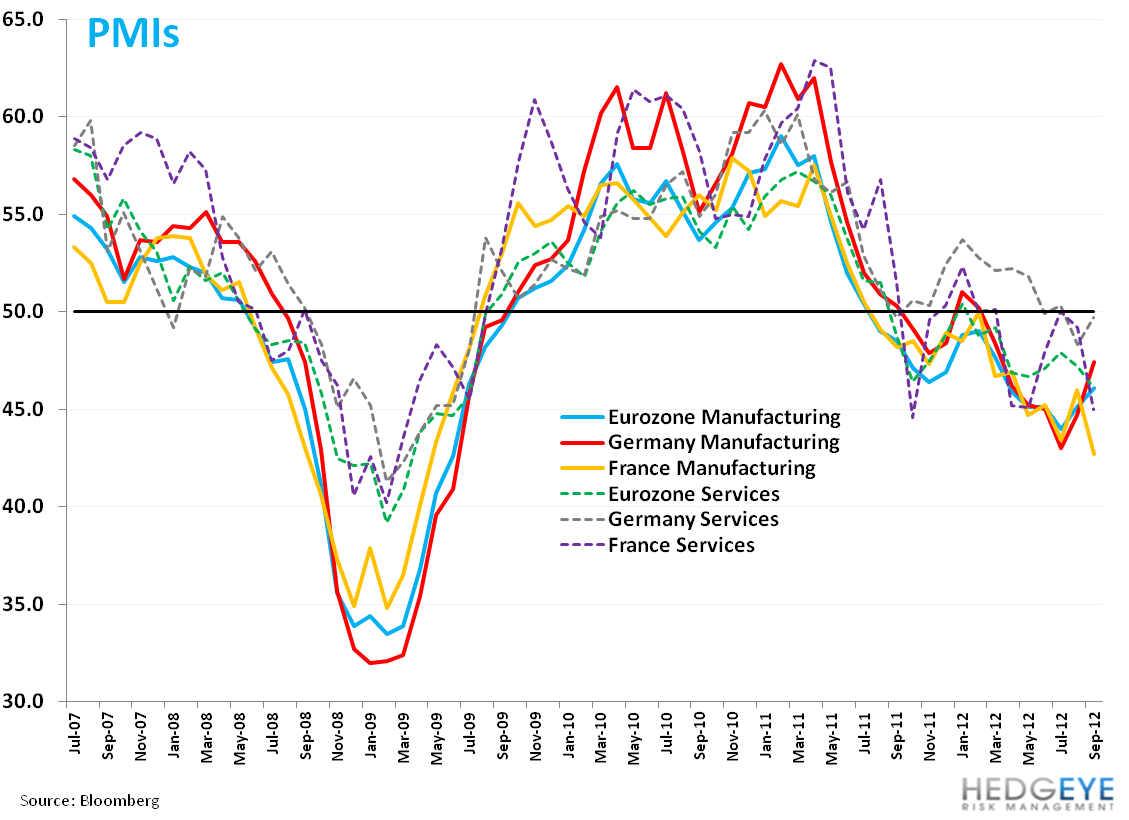

European Manufacturing and Services PMIs for September (released on Monday and today, respectively) have shown little to no improvement over the last 7-8 straight months, stuck below the 50 line indicating contraction (see charts below).

This comes as no great surprise given the larger Eurozone forces of slowing growth alongside fiscal consolidation and political consternation from Eurocrats on collective policy. To the latter point, we believe the runway to get to a fiscal union (including a banking union) is much longer than current expectations project. We see both the push back from stronger nations like Germany to “blindly” accept this risk (ie without conditions to benefit itself and/or limit reduction in its credit rating) and coordination to set up the logistics of a fiscal union inducing a protracted drag in this decision.

To the point on timing, ECB Executive Board member Joerg Asmussen said on Monday that the ECB will not rush through “half-baked” plans for a new pan-European supervisor.

Remember that German Chancellor Merkel and Bundesbank President Jens Weidmann continue to butt heads on many fiscal issues. Eurobonds is one topic that Weidmann remains vehemently against while Merkel has not ruled out their use. However, if the Eurozone is to move to a fiscal union, Eurobonds are simply a natural extension of a fiscally united union. This is one hot topic to monitor as we move through the calendar year.

Interestingly, yesterday, Jin Liqun, chairman of the supervisory board of the China Investment Corporation (China’s $480B sovereign wealth fund), said that CIC will not buy bonds issued by debt-ridden Eurozone countries until their fundamental problems are solved. This point is of note because some over the last 12 months have suggested there’s a reduction in “risk” across Europe given the willingness of the Chinese to step in and support the region. Further, Jin said:

“The mass demonstrations in Greece and in Spain against fiscal tightening do not bode well for attracting investment into their debt… It's not realistic to expect any Chinese investor, CIC included, to buy the bonds, which are not safe…If the euro zone would issue a Eurobond backed by all of the countries - it is more attractive to international investors. Backed by all of the countries means backed by the core members."

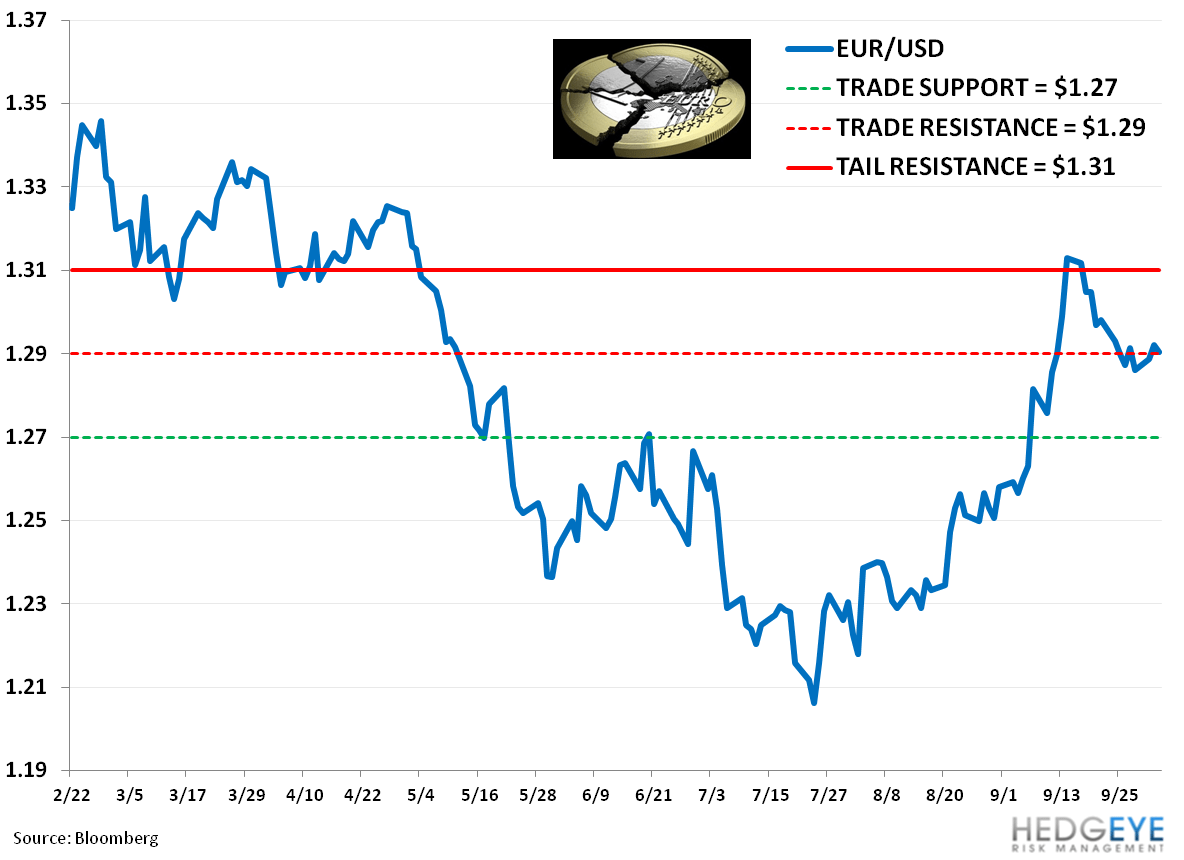

We currently have a Real-time position in German Bonds via the etf BUNL. Keith covered our Real-time position in FXE (EUR/USD) on 10/1 at $128.53 with the cross at our immediate term TRADE oversold level. The EUR/USD continues to fail at its $1.31 TAIL line of resistance.

Matthew Hedrick

Senior Analyst