“Tax changes have very large effects: an exogenous tax increase of 1 percent of GDP lowers real GDP by roughly 2 to 3 percent."

-National Bureau of Economic Research

We have been at times criticized for using Keynesianism in a derogatory sense as it relates to economic policy. Critics of this use suggest that current policy makers are not really true Keynesians and are misusing and misinterpreting, the tenets of Keynesian economic policy. This may well be true and we will fully admit that Keynes has become a bit of a straw man of sorts for us.

Nonetheless, there is no denying that government deficit spending has led to unsustainable debt loads globally. In the United States, the outcome of a decade of unfettered deficit spending is coming to a head in the next quarter with what we are calling the Keynesian Trifecta – increased taxes, lower government spending, and another debt ceiling.

On the first point of taxes, based on current policy we are set to undergo perhaps the most meaningful tax increases in a generation effective 2013. The quote above comes from a paper co-written by Christina Romer, formerly President Obama’s chief economic advisor entitled, “The Macroeconomic Effects of Tax Changes: Estimates Based on a New Measure of Fiscal Shocks.” The key takeaway is that tax increases in the short run negatively impact growth.

The key areas in which the tax increases are coming in 2013, which the Washington Post has aptly named Taxmageddon, include:

- 34% of the tax increases come from the expiration of the 2001 and 2003 Bush tax cuts (includes capital gains and dividend increases);

- 25% of the tax increase comes from an expiration of the temporary payroll tax cut (including on Social Security deductions); and

- The remainder largely comes from new taxes under the Affordable Care Act (or Obamacare).

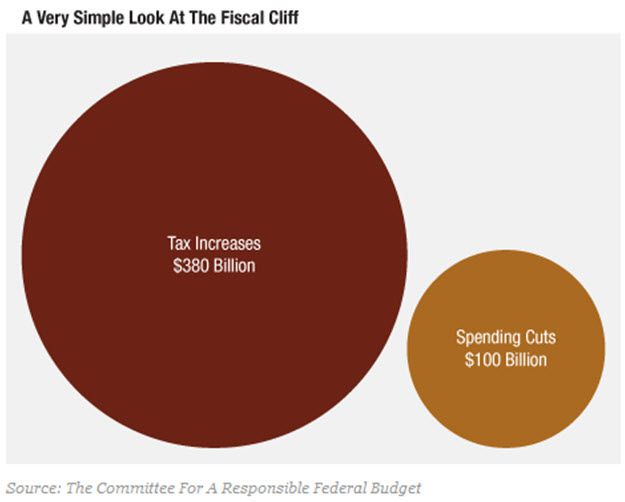

Below, we’ve attached a graphic that looks at the scale of the coming tax increases. There are many estimates for the actual annual scale, but the range is $380 - $450 billion. On a GDP base of just north of $15 trillion, this accounts to an aggregate GDP tax of 2 – 3%.

In the current form, the tax increases look to impact a wide portion of the tax base. The key exception is the purported middle class, so those unmarried filers making less than $35K per year or married joint filers making less than $70K per year. In the table below, prepared by our Financials Sector Head Josh Steiner, we look at tax increases by both income level and also by line item. The key takeaway is that the upcoming tax increase will be broad based and comprehensive.

In fact, a report released today from the Tax Policy Center finds that 90 percent of Americans will see their taxes go up starting January 1st. The average tax increase will be $3,500 and the typical middle-income taxpayer will see his or her tax bill go up by $2,500.

In conjunction with these tax increases is the automatic cut in government spending that is going to occur under the Budget Control Act of 2011. Since the Joint Select Committee on Deficit Reduction failed to implement a $1.5 trillion deficit reduction plan, the sequestration process is triggered. Sequestration cuts are not new in the United States (three under the Gramm-Rudman-Hollings deficit targets and two under the statutory discretionary spending caps), but this round will be the largest in terms of scale.

One interesting note is that while the federal fiscal year ends in September, the first year of sequestration doesn’t begin until January 2013. As a result, a year of cuts will be squeezed into nine months. As American Progress wrote:

“On a percentage basis the cuts would have to be about a third larger than the 8.5 percent to 10 percent required for the year as a whole. Such programs would face cuts of between 11.3 percent and 13.3 percent during that nine-month period.”

Therefore at a time when we are set to see tax increases that are as large as the U.S. economy has experienced in a generation, the cuts in government spending will also be magnified.

The Budget Control Act spells out the steps that the Office of Management and Budget must take due to the lack of agreement by the Joint Committee. In 2013, sequestration cuts will be equally split between defense and non-defense for a total of $109.3 billion in total cuts. In terms of the non-defense cuts, it is expected that $16.7 billion come from mandatory programs with the bulk coming from Medicare.

In the long run, we are firm believers that taking capital away from the government and giving it back to the people to more efficiently allocate is a great thing. In the short run, though, we do need to be aware that deep cuts in government spending will be a headwind to growth. On the basis of $109.3 billion in spending cuts, this will be an incremental -0.5% detractor from GDP in 2013.

Finally, as if the cliff weren’t enough, the debt ceiling is about to be breeched again. The statutory debt limit is $16.4 trillion. As of September 28th, the total debt outstanding of the U.S. government was $16.0 trillion. The estimated required debt issuance for Q4 2012 is $316 billion. This would mean that the implied capacity going into 2013 is $50.1 billion. Therefore the debt ceiling is likely to be breached in January 2013. In reality, the ceiling can likely be extended a quarter or two based on a number of one-time items, but will most definitely be hit in the first half of 2013.

If you recall to the summer of 2011, the debt ceiling was a major catalyst for the market. In the last chart we highlight the impact to equity markets in the summer of 2011 as uncertainty around the debt ceiling accelerated. From July 1st the S&P 500 went from 1,315 to its summer trough of 1,127 on August 22nd - for an aggregate decline of some 14%.

As if Taxmagedon weren’t enough . . . the Keynesian Trifecta is looming on the horizon and will slow growth and potentially be a negative catalyst for the equity markets.

Daryl G. Jones

Director of Research