Housing is improving but still not good enough

- We’ve shown that housing prices have historically been the most statistically significant macro variable in explaining gaming revenue growth

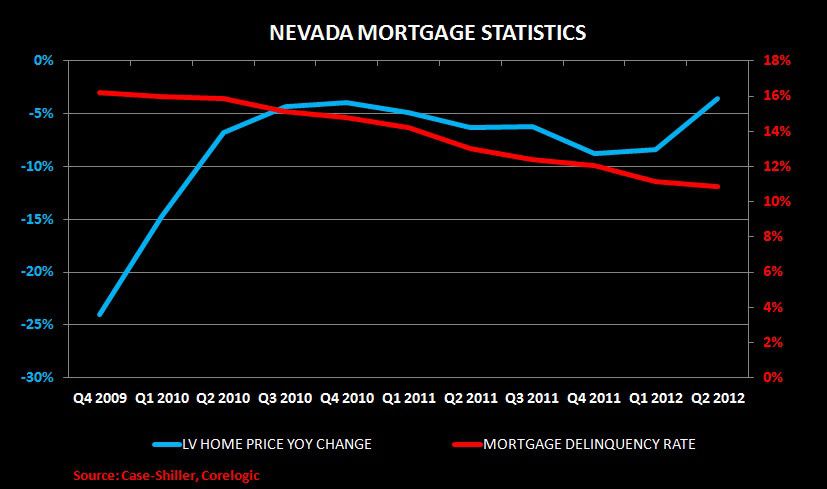

- While better, home prices were still down YoY in Q2. The good news is that price change might be on the positive side in Q3.

- The mortgage delinquency rate continues to slope downward which is a decent economic barometer. However, that could also mean that more people are paying their mortgage or have moved out and are now paying rent. Either way, it likely means less monthly discretionary spending which could be impacting gaming spend. This phenomenon could continue to suppress locals gaming revenue.