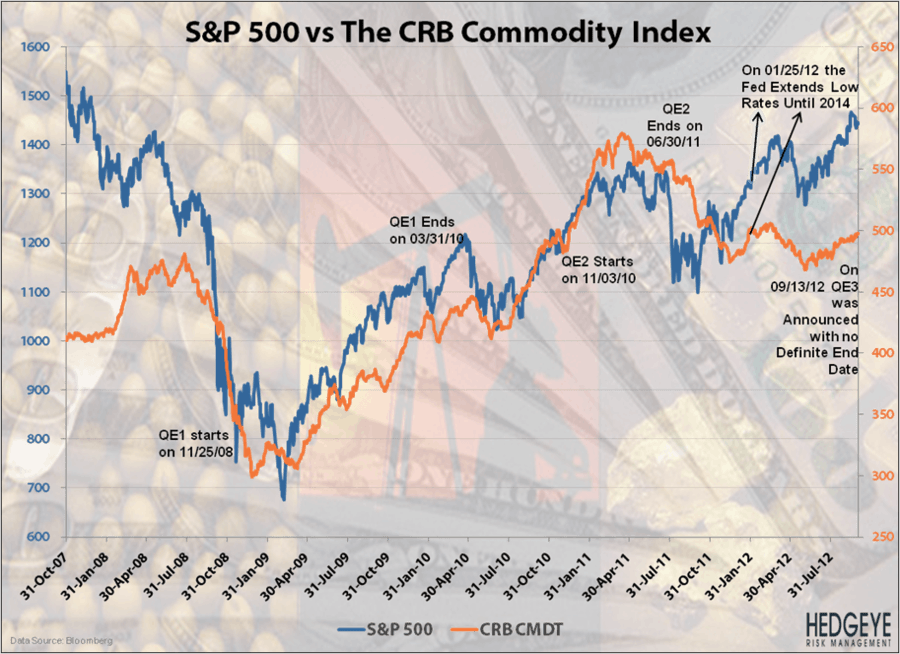

If you look at the chart below, you can clearly see the effects that Ben Bernanke and the Federal Reserve have had in commodity markets since implementing quantitative easing. This is the work of your central planners at work, folks. Since April 2009, you've had to feel the effects at the pump and the grocery store. Commodity prices will continue to climb higher as long as the US dollar stays depressed.