TODAY’S S&P 500 SET-UP – October 2, 2012

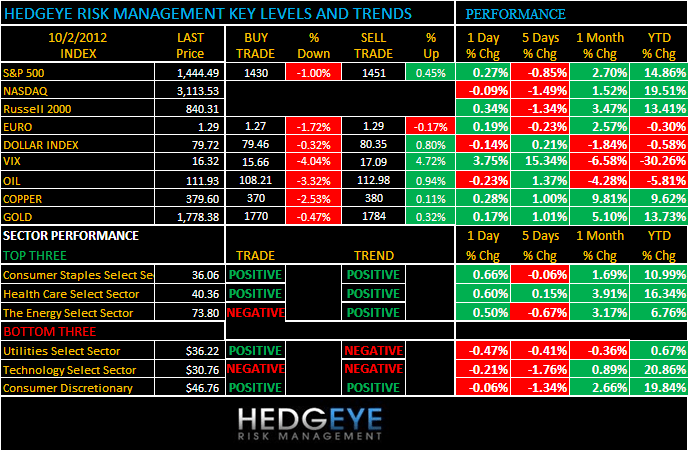

As we look at today’s set up for the S&P 500, the range is 21 points or -1.00% downside to 1430 and 0.45% upside to 1451.

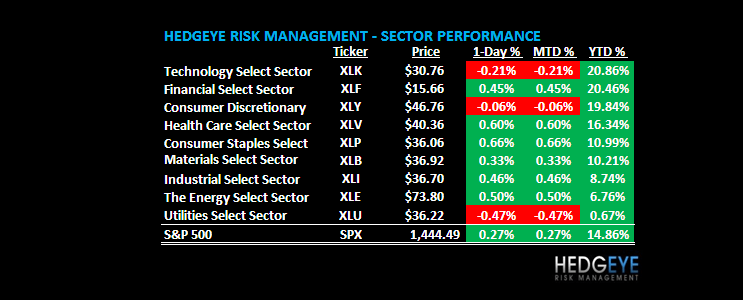

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 10/01 NYSE 718

- Increase versus the prior day’s trading of -658

- VOLUME: on 10/01 NYSE 672.31

- Decrease versus prior day’s trading of -19.22%

- VIX: as of 10/01 was at 16.32

- Increase versus most recent day’s trading of 3.75%

- Year-to-date decrease of -30.26%

- SPX PUT/CALL RATIO: as of 10/01 closed at 1.68

- Down from the day prior at 2.01

CREDIT/ECONOMIC MARKET LOOK:

TREASURIES – bonds still don’t seem to care about the daily flicker of S&P futures; the 10yr yield hasn’t moved more than a beep in the last 48hrs; long-bond remains in a Bullish Formation as 10yr yields look like they could easily test YTD lows.

- TED SPREAD: as of this morning 27.42

- 3-MONTH T-BILL YIELD: as of this morning 0.08%

- 10-Year: as of this morning 1.63%

- Increase from prior day’s trading of 1.62%

- YIELD CURVE: as of this morning 1.40

- Up from prior day’s trading at 1.39

MACRO DATA POINTS (Bloomberg Estimates)

- 9:45am: ISM New York, Sept. (prior 51.4)

- 11am: Fed to buy $1.75b-$2.25b Treasury debt due 2/15/2036-8/15/2042

- 11:30am: U.S. Treasury to sell 4-week bills

GOVERNMENT/POLITICS:

- House, Senate not in session

- Obama, Romney make preparations for first presidential debate tomorrow

- News conference on latest Quinnipiac poll. NPC. 10am

- SEC hosts discussion on automated-trading technologies. 10am

- FAA advisory panel holds second day of meetings to review air-traffic control procedures. National Harbor. 8:30am

- Early voting begins in Ohio

WHAT TO WATCH:

- U.S. auto sales seen advancing 9.5% in September

- SEC to investigate high-frequency trading

- Samsung says Apple iPhone 5 infringes eight patents in lawsuit

- Former SAC Capital manager tells FBI fund used insider information

- SAIC loses protest of $4.6b contract awarded to Lockheed

- Juniper said to cut 500 jobs to reduce costs amid competition

- U.S. retail sales growth may slow to 4.1% during holiday season

- Manhattan home inventory falls to 7-yr low

- Value Investing Congress includes presentations from David Einhorn

EARNINGS:

- Mosaic (MOS) 7am, $1.16

- Acuity Brands (AYI) 8:19am, $0.93

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Palm Oil Slumps Most Since October 2008 to Lowest in Three Years

- Rubber Bulls Back as Exporters Cut Most Since 2009: Commodities

- Soybeans Reach Lowest Price Since July on U.S. Harvest Progress

- Oil Trades Near One-Week High as U.S. Manufacturing Expands

- Gold Set to Gain for Second Day After Fed Renews Stimulus Pledge

- Cocoa Falls as Concerns Ease Over Ivory Coast Industry Changes

- Iron-Ore Swaps Little Changed as China Holidays Slow Trading

- Countries Must Refrain From Banning Food Exports, FAO Says

- Zinc Price Softens in 3Q on Surplus, 9.3% Rise Expected in 4Q

- Cargill to Stop Using Fuel-Inefficient Ships to Curb Emissions

- Nuclear Output Seen Falling to 3-Year Low on Refueling Shutdowns

- Rothschild’s Bashed Bumi Offers ‘Great Trade’: Chart of the Day

- Rubber May Advance 28% on Ichimoku Chart: Technical Analysis

- Copper May Gain for Fourth Day on Global Central-Bank Stimulus

CURRENCIES

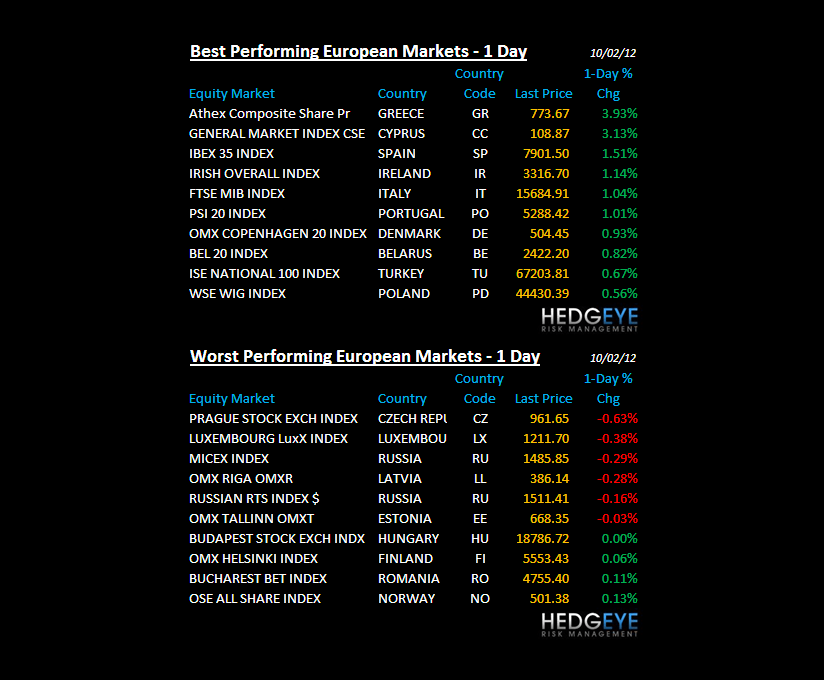

EUROPEAN MARKETS

EUROPE – after European Equities got slammed last wk (Spain and Italy -6% each), seeing day2 of the bounce; plenty of rumoring going around about when Spain asks for bailouts and reminds the world they’ve been lying about pretty much every number that matters #classy; should end well.

ASIAN MARKETS

JAPAN – top 3 economy in the world is now seeing both its stock market and economic data collide; after a bearish Tankan yesterday, Nikkei closed down again overnight, taking the draw-down since the global #GrowthSlowing top (March) to -14.3%; #KeyenesianEconomics.

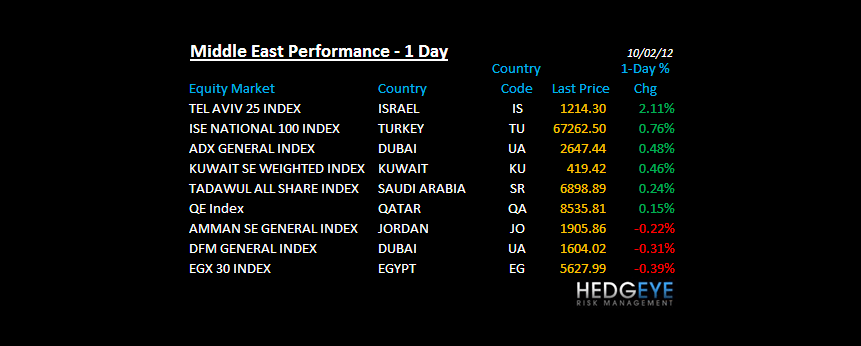

MIDDLE EAST

The Hedgeye Macro Team