TODAY’S S&P 500 SET-UP – October 1, 2012

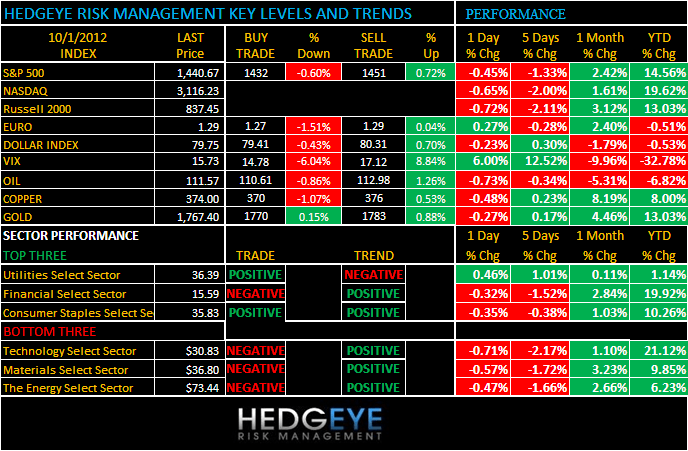

As we look at today’s set up for the S&P 500, the range is 19 points or -0.60% downside to 1432 and 0.72% upside to 1451.

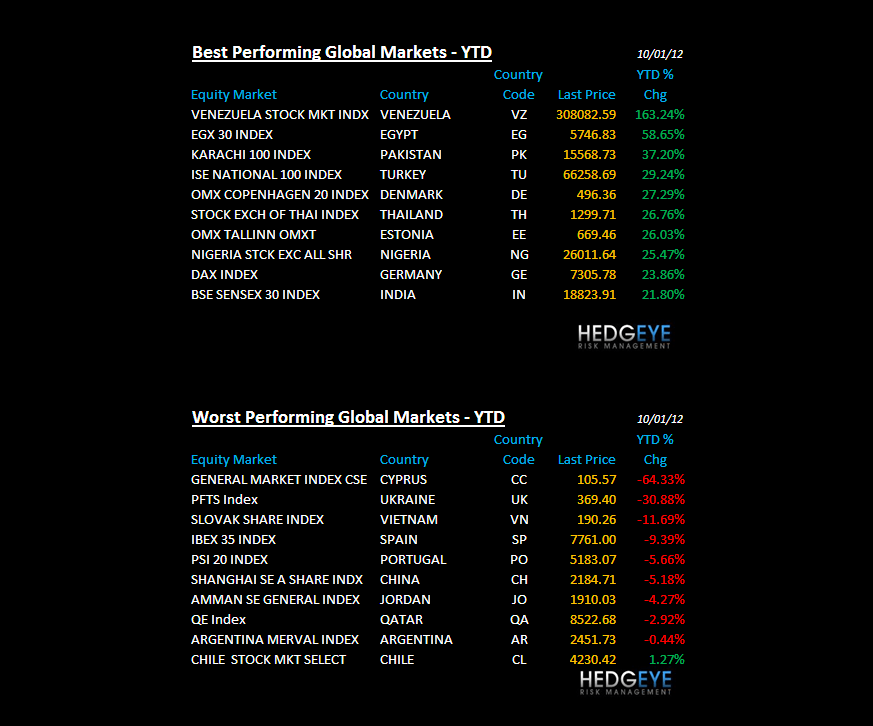

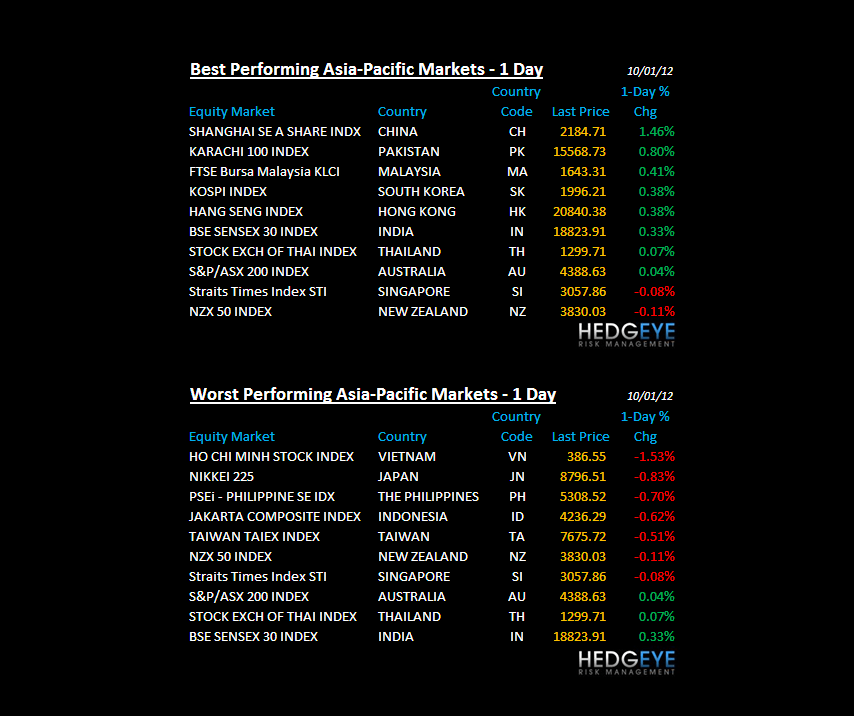

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 09/28 NYSE -658

- Decrease versus the prior day’s trading of 1479

- VOLUME: on 09/28 NYSE 832.31

- Increase versus prior day’s trading of 31.27%

- VIX: as of 09/28 was at 15.73

- Increase versus most recent day’s trading of 6.00%

- Year-to-date decrease of -32.78%

- SPX PUT/CALL RATIO: as of 09/28 closed at 2.01

- Up from the day prior at 1.82

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 26.72

- 3-MONTH T-BILL YIELD: as of this morning 0.09%

- 10-Year: as of this morning 1.62%

- Decrease from prior day’s trading of 1.63%

- YIELD CURVE: as of this morning 1.39

- Down from prior day’s trading at 1.40

MACRO DATA POINTS (Bloomberg Estimates)

- 8:58am: Markit US PMI Final, Sept. est. 51.5 (prior 51.5)

- 10am: ISM Manufacturing, Sept. est. 49.8 (prior 49.6)

- 10am: Construction Spending M/m, Aug. est. 0.5% (prior -0.9%)

- 11am: Fed to buy $4.5b-$5.5b Treasury debt due 11/15/2020-8/15/2022

- 11:30am: U.S. to sell $32b 3-mo, bills, $28b 6-mo. bills

- 12pm: Fed’s Williams speaks in San Francisco

- 12:30pm: Bernanke speaks on monetary policy in Indianapolis

- 4pm: USDA crop-condition reports

GOVERNMENT:

- U.S. government’s fiscal year, Supreme Court term begin

- FDA Center for Drug Evaluation and Research Director Janet Woodcock speaks on agency’s future, 8am

- FAA advisory panel meets to review air-traffic control procedures for standardization, revision, clarification and upgrading of terminology, 8:30am

- WTO Director-General Pascal Lamy speaks on future of international trade at Brookings, 4:45pm

WHAT TO WATCH:

- U.S. manufacturing probably shrank in Sept. as global economy

- Xstrata backs Glencore bid after winning board assurance

- Kraft Foods Inc. becomes Mondelez; Kraft Foods Group spun off

- Greek government resumes talks with international creditors

- U.S. jobs outlook seen weak as companies see need to cut costs

- Nokia, Oracle to unveil mapping software pact: WSJ

- KKR said to buy stake in oil services company Acteon Group

- Euro-area unemployment at record 11.4% in Aug., matching est.

- Sony’s ‘Hotel Transylvania’ posts $43m in weekend N.A. sales

- Yahoo to hold “all-hands” meeting on process, goals: AllThingsD

- Japan Tankan sentiment worsens as slowdown hurts exports

- Chinese markets are closed all week

- LightSquared bankruptcy hearing over control of co.

EARNINGS:

- Cal-Maine Foods (CALM) 6:30am, $0.35

- Ferrellgas Partners (FGP) 7am, $(0.43)

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

OIL – the most bullish break-down in all of Global Macro in the last 10 days is the one associated with the USD having 2 consecutive up wks; Brent’s long-term TAIL line = $112.98, so we’ll be watching that line closely this week into and out of the Oct 3rd debate.

- Oil Declines From One-Week High as China Manufacturing Weakens

- Bull Wagers Tumble Most in 16 Weeks as Prices Slump: Commodities

- Xstrata Recommends Glencore’s Revised Offer to Its Shareholders

- Corn Reaches Two-Week High as Stocks Fall More Than Estimated

- Raw Sugar Climbs for Third Day Before Delivery; Cocoa Declines

- Gold Seen Falling in London as Some Investors Sell After Rally

- Copper Seen Falling as East Asian Economies Struggle for Growth

- Iron-Ore Price Forecast Cut by ANZ to $110/MT for Fourth Quarter

- Hedge Funds Cut Bullish Oil Bets as Output Soars: Energy Markets

- U.S. Beating Russia in Diesel Shipments Boosts Tankers: Freight

- Sumitomo Sees ‘Solar Bubble’ as Japan Rejects Nuclear: Energy

- Timah to Assess Work of Bangka Miners to Ensure Tin-Ore Supplies

- Silver Tops Commodities First Time Since 1997: Chart of the Day

- Iron-Ore Swaps Slide 0.5% in London, Clarkson Data Show

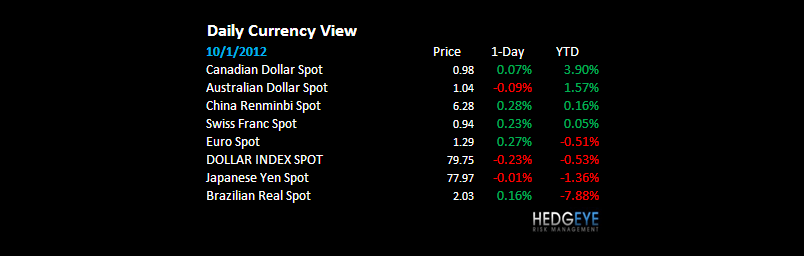

CURRENCIES

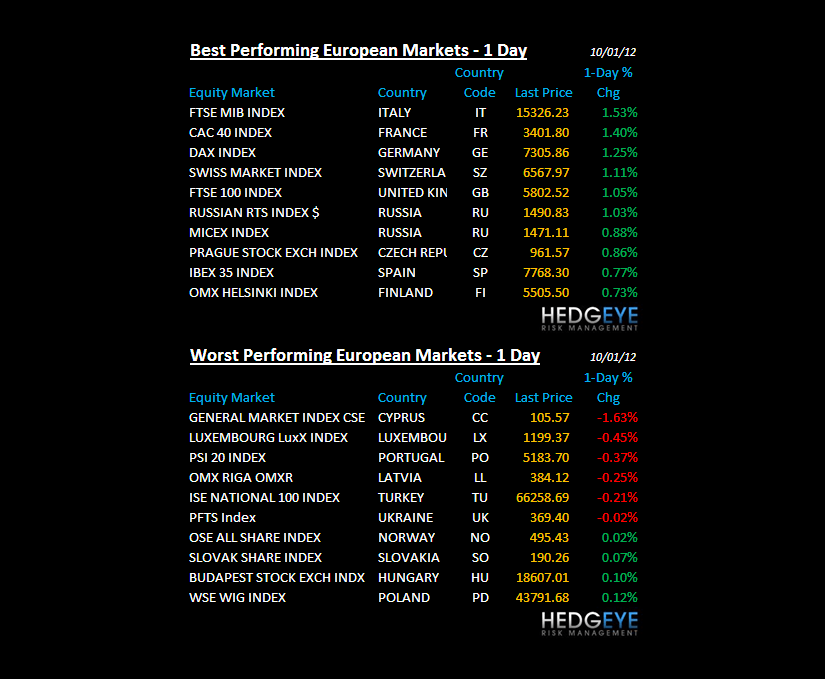

EUROPEAN MARKETS

FRANCE – the Hollande election seems to be having some economic issues; France reported an absolute bomb of a PMI print for SEP of 42.7 this morning (vs 46 in AUG); still trying to figure out how USA becoming more like France in 2013 is a good thing…

ASIAN MARKETS

JAPAN – if countries with Keynesian policy makers would just ban reporting of economic data, everything would be fine; after closing down -2.6% last wk, Nikkei continues its bearish divergence, down another -0.8% overnight (-14.2% since the global #GrowthSlowing top in March); Top3 economy in the world; not inconsequential.

MIDDLE EAST

The Hedgeye Macro Team