Nike’s setup today is unlike anything we’ve seen in a very long time. It’s fundamentals are showing signs of stabilization, with a) an exceptionally strong footwear business offsetting week apparel in China and parts of Europe, and b) gross margins finally headed back up again after many quarters missing expectations, a) inventories getting back into balance with an outline. But at the same time we’re seeing the worst sell side sentiment Nike has seen in 14 years.

It’s not enough for us to simply take those two factors and buy the stock. Last I check stocks on trade on a two factor model. Ours uses about another 25. Over the past three weeks we’ve been advising clients to trade around a range of $96 to $101, which is served us and them quite well. The problem however is that once Nike broke down through $96, a number starting with an eight is in play. From the fundamental standpoint I can point to zero reasons why it will get there. But near-term irrational stock moves don’t happen based on fundamentals.

Sentiment: So what has Sell-side sentiment so bad? Currently only 37% of the ratings are Buy. What’s funny is that if Wall Street coverage was accurate there would be a fairly even distribution of readings across the buy sell and hold spectrum. Nike however usually has a buy ratio between 90% and 100% percent. Just three months ago it’s ratio hit a recent low of 75% and has since been cut in half to 37%. Just put this into context this is a ratio that’s just slightly above that of JCPenney one of the worst companies and retail right now.

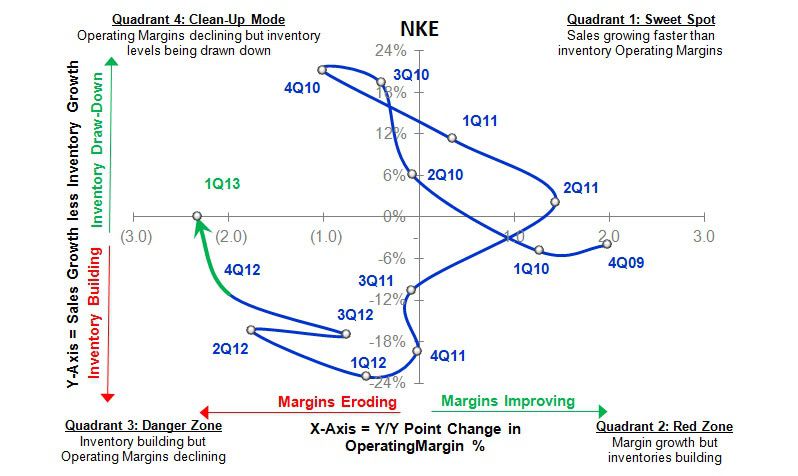

SIGMA: Those who track our Sigma analysis will immediately see that Nike has swung right up to quadrant four of our chart. This is a very critical move in that for the past nine quarters Nike’s positioning on this quadrant has moved either down or to the left, both of which are bad. Were often asked what the most favorable move is for company in this analytical framework, and the answer is clear. It’s the one that Nike just did. It’s when sales begin to grow faster than inventories and the rate of degradation in margins begins to ease. This is a prime set up for improvement into the sweet spot for the next four quarters. That’s when stocks work in retail.

But again as noted from a risk management standpoint we have to be very careful here. The stock is clearly broken down below its key support level and will be looking to add it back to our real-time positions on red.

Here’s some other puts and takes in the quarter which we thought were notable:

- This is more of a company fluff statistic but we still find it notable how every participating nation in the Olympics sent at least one woman and that 44% of all athletes were women in the Olympic Games. That is obviously great news for a secular trend of increased sports participation for women on a global scale. This helps Nike. Not next week, not next month, but a very big long-term positive.

- China futures down six by no means is positive, but on the two-year run great it was actually a slight improvement from the +2% that Nike put up last quarter.

- Nike Japan posted this +7% growth rate in futures which is the first time in forever that we’re seeing growth over there. Granted, “comps are easy” but Nike has been unable to “comp the easy comp” for the better part of a decade in Japan.

- Gross margins compressed by -80bps reflecting benefit from pricing and cost initiatives that were more than offset by higher input costs for materials and labor and mix shift to lower margin businesses. However, the company did not highlight the impact of the expensing – as opposed to amortization – of tools and molds associated with its digital running gear. They could have ‘explained away’ a good 50bps of margin hit there.

- In looking at regional performance:

- North America revs came in up +23% (footwear +20%, apparel +26%)

- Western Europe revs increased by +6% driven by running, basketball and football

- Eastern Europe revs were up by +16% driven by Russia and Turkey and running

- China revs increased by +7% with double-digit growth in running, basketball and action sports. Apparel was down -1%. Definitely gave the impression on the call that after the initial market-led slowdown, Nike is taking the initiative to tighten its order book to improve the quality of business. Two thoughts on this 1) Let’s give them credit. They might have stuffed the channel, but at least they’re taking the steps to unstuff it. 2) This is reminiscent of Nike circa 2000/01 when Nike had this same problem in the US market. Its subsequent actions have had a lasting impact, and are arguably the bedrock for the numbers we see today.

- Emerging market revs were up +22% driven by running, football, and sportswear. That said we were disappointed to see emerging markets futures come in at +9% on a reported basis (14% Constant Currency). Those are decent enough growth numbers, but the reality is that emerging markets should be putting up mind-bending growth figures.

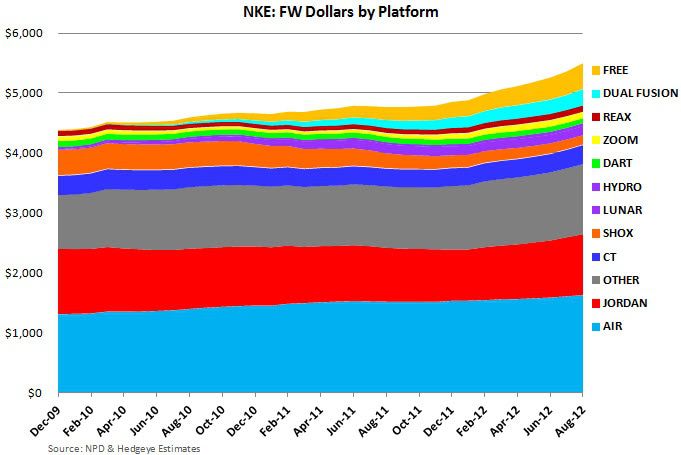

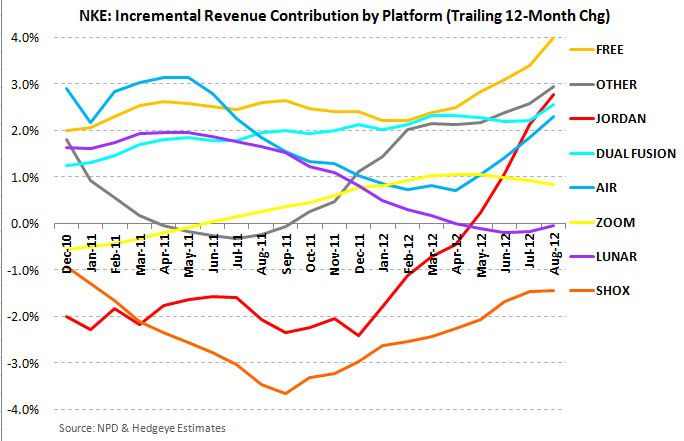

In a note earlier this week “NKE: A Rare Glimpse,” we looked at the breadth of platform engines driving NKE’s top-line. Free and Dual Fusion are the fastest growing. In fact, these two platforms accounted for nearly half of NKE’s domestic growth over the past year. This is particularly notable given that the NKE Free platform only started selling through Europe less than 6-months ago (March/April), which we expect to continue to help offset persistent macro headwinds.