Post-Bernanke party, when stocks have ripped 50-100% higher in just a few months, energy is one place where we’re looking for short ideas. Fundamentals like durable goods, growth and demand are beginning to roll over and with stocks at expensive prices, we think there’s room for a pullback. Growth is still slowing - remember that.

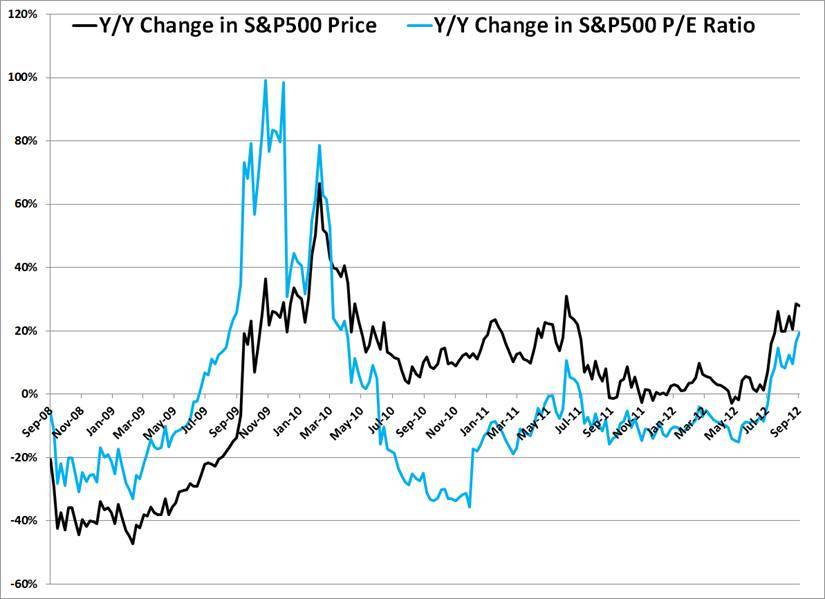

S&P500 revenues will be +2.2% YoY in the 3Q – adjust that for inflation and real revenue growth has gone negative. And lately many companies are missing estimates and guiding lower, so the forward outlook is not much better. The question is how high of a multiple can some of these companies trade at in terms of price-to-earnings? 20x? 60x? 100x? Things seem to be getting worse in the market and the economy, not better.