TODAY’S S&P 500 SET-UP – September 28, 2012

As we look at today’s set up for the S&P 500, the range is 19 points or -0.91% downside to 1434 and 0.40% upside to 1453.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 09/27 NYSE 1479

- Increase versus the prior day’s trading of -678

- VOLUME: on 09/27 NYSE 634.05

- Decrease versus prior day’s trading of -14.15%

- VIX: as of 09/27 was at 14.84

- Decrease versus most recent day’s trading of -11.72%

- Year-to-date decrease of -36.58%

- SPX PUT/CALL RATIO: as of 09/27 closed at 1.82

- Down from the day prior at 1.84

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 27.40

- 3-MONTH T-BILL YIELD: as of this morning 0.09%

- 10-Year: as of this morning 1.62%

- Decrease from prior day’s trading of 1.65%

- YIELD CURVE: as of this morning 1.38

- Down from prior day’s trading at 1.40

MACRO DATA POINTS (Bloomberg Estimates)

- 8:30am: Personal Income, Aug., est. 0.2% (prior 0.3%)

- 8:30am: Personal Spending, Aug., est. 0.5% (prior 0.4%)

- 8:30am: PCE Core (Y/y), Aug., est. 1.6% (prior 1.6%)

- 9am: NAPM-Milwaukee, Sept., est. 45.0 (prior 42.9)

- 9:45am: Chicago Purchasing Manager, Sept., est. 53 (prior 53)

- 9:55am: UMich Confidence, Sept. F, est. 79 (prior 79.2)

- 11am: Fed to buy $1.5b-$2b notes due 2/15/2036 to 8/15/2042

- 1pm: Fed’s Fisher speaks in Dallas on economy

- 1pm: Baker Hughes rig count

GOVERNMENT:

- Obama leads in latest swing-state polls as first debate nears

- Financial Stability Oversight Council meets to choose first nonbank companies likely to be branded potential risks to financial system

- FDIC holds Consumer Research Symposium; panelists include Fed officials, 8am

- CFTC holds closed meeting on enforcement matters, 10am

- SEC holds meeting of Dodd-Frank Investor Advisory Cmte, 10am

- WTO sets up panel to decide whether U.S. broke global commerce rules with anti-subsidy duties affecting $7.3b of Chinese products

- Acting Commerce Secretary Rebecca Blank speaks at Council on Foreign Relations on policies to promote manufacturing, 12pm

- FCC open meeting on licensing, operating rules for satellite services; economic, innovation opportunities of spectrum through incentive auctions; mobile spectrum holdings, 10:30am

- Homeland Security Secretary Janet Napolitano speaks at cybersecurity summit, 8am

WHAT TO WATCH:

- Spanish banks scheduled to release results of stress tests today

- Monti says ECB conditions, IMF role hinder bond-buying requests

- Yuan climbs to strongest level since 1993 on China stimulus

- Euro-region inflation unexpectedly accelerated in September

- Xstrata split with Glencore on terms as deadline nears

- FSA to oversee Libor in streamlining of tarnished benchmark

- U.S. criminal Libor probe said to seek London trader interviews

- Sony to invest $645m in Olympus

- Hartford to sell life-insurance unit to Prudential Financial

- U.S. Debate, ECB Bond Buying, Spain: Week Ahead Sept. 29-Oct. 6

EARNINGS:

- Finish Line (FINL) 7am, $0.44

- Walgreen (WAG) 7:30am, $0.56 - Preview

- American Greetings (AM) 7:30am, $0.14

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Sumitomo Sees Higher Copper Fees in 2013 as Supplies Increase

- Copper Bulls Retreat on Concern Stimulus Not Enough: Commodities

- Crude Oil Poised for Quarterly Gain Before U.S. Spending Report

- Gold Seen Extending Best Quarterly Gain Since 2010 on Stimulus

- Copper Heads for Quarterly Gain on Reduced Euro-Crisis Concern

- Corn Slides to an 11-Week Low Before USDA Report; Wheat Declines

- Cocoa Advances Most in Three Weeks in London; Coffee Declines

- Domestic Cuts May Make India a Net Importer of Iron Ore by 2015

- Brazil Has 24.8 Million Tons of Sugar for Export, Datagro Says

- Oil May Fall on Weaker Economy and Higher Output, Survey Shows

- Airlines Threatened by Costliest Fuel Since 2008: Energy Markets

- Shale Takeovers Loom as Texas Discounted in Australia: Real M&A

- Xstrata Split With Glencore on Terms as Deadline Nears: Energy

- India’s Goa Iron Ore Ban Likely to Have Minimal Effect on Market

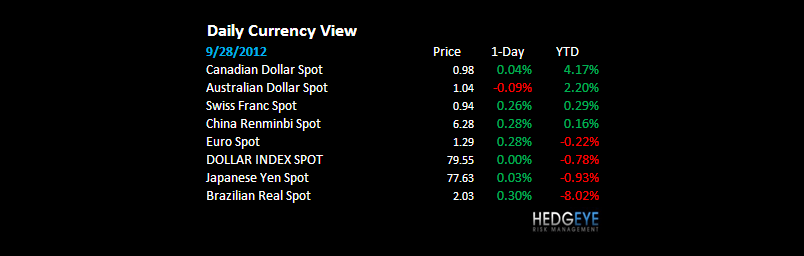

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

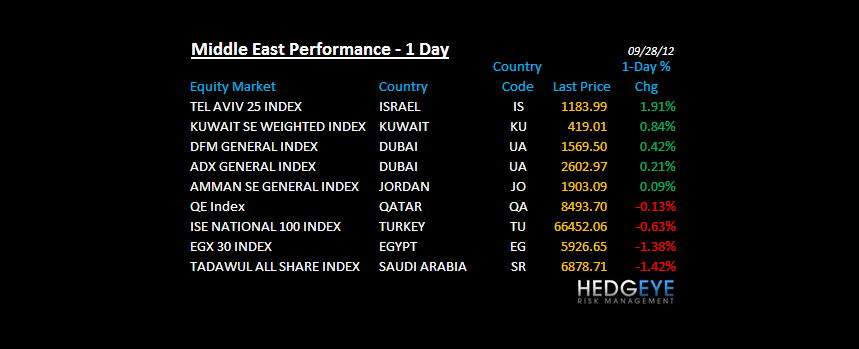

MIDDLE EAST

The Hedgeye Macro Team