As the US Dollar gained, many soft commodities that we track as part of our process declined during the last week. In line with our macro process of paying attention to Correlation Risk, those commodities with the tightest inverse correlation to the US Dollar Index posted the sharpest week-over-week declines.

Summary View

Coffee prices have been gaining on speculation that government stimulus measures in China will buoy consumption within the country – the world’s top consumer.

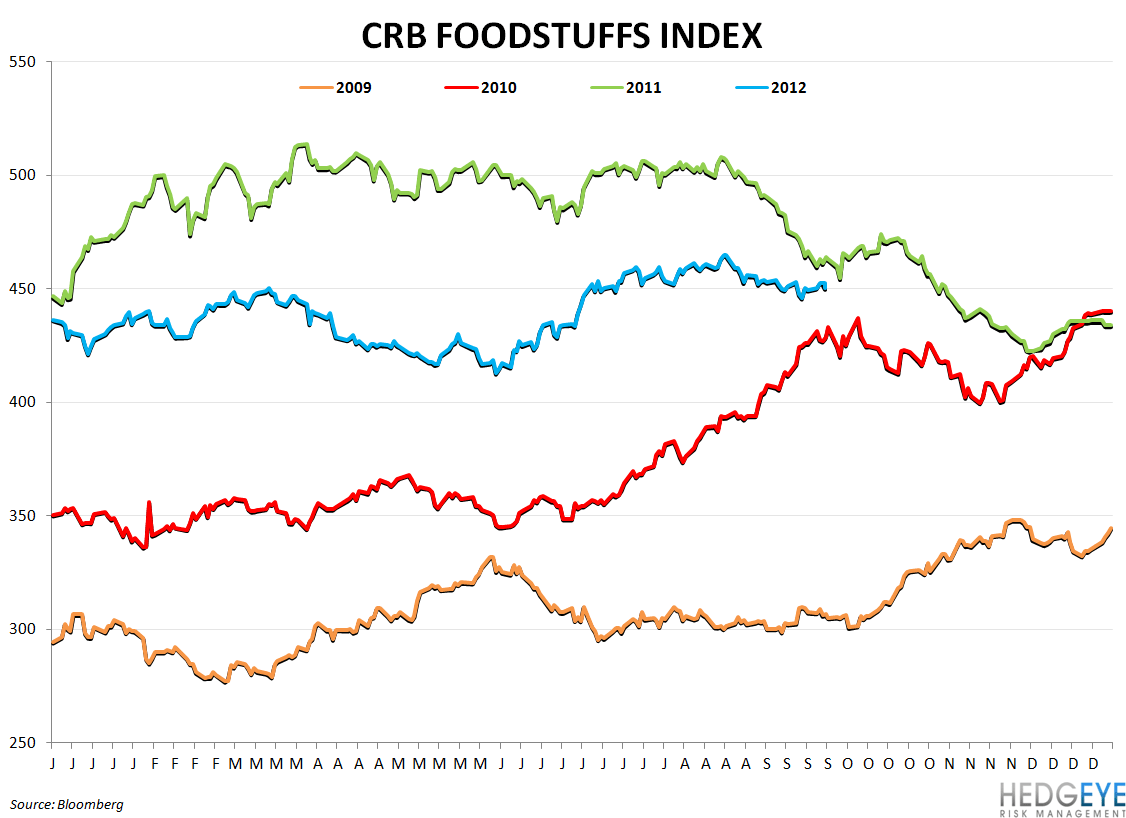

Cheese prices have been rising sharply of late, gaining 7% over the last week as speculation mounts that milk production is set to slow substantially in 2012/2013. Dairy prices are, to varying degrees, a negative for TXRH, CAKE, DPZ, PZZA, and CMG.

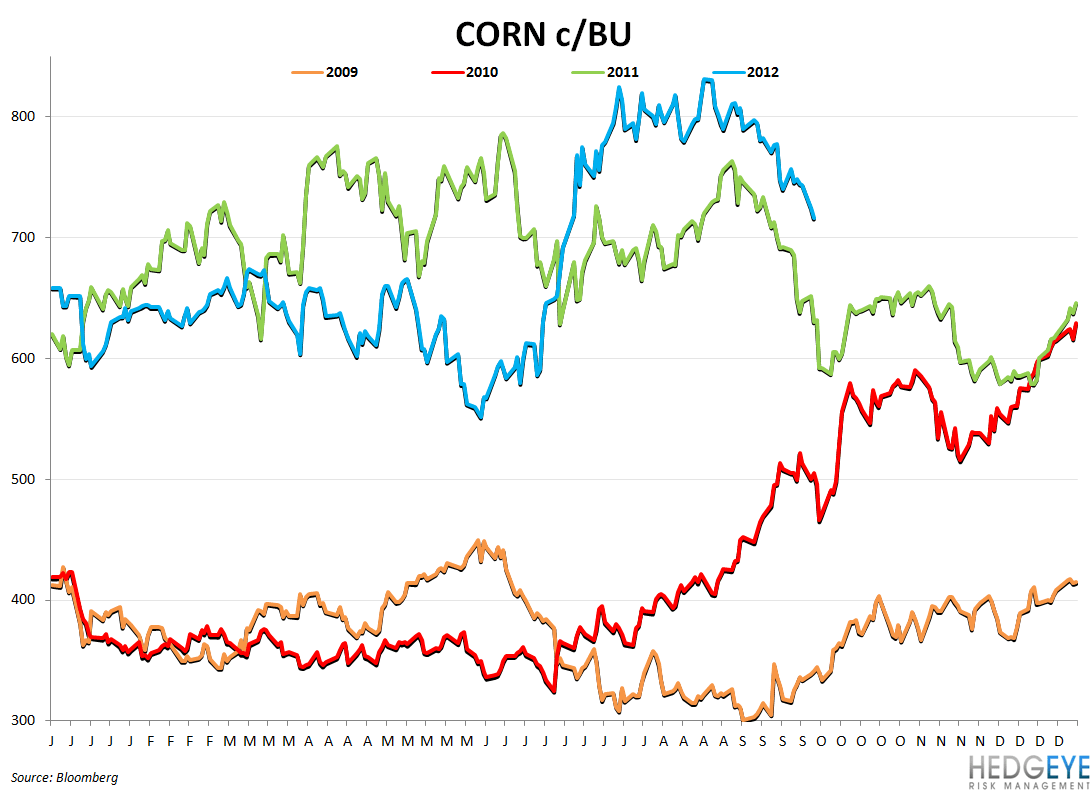

Corn prices declined 4% week-over-week as the USDA is set to release the Grain Stocks report tomorrow. Grain exports data this morning was bearish for corn prices with 400 metric tons sold in the last week versus expectations of 150k-200k. Demand destruction is evident not only in the export sales miss but in the rising stocks of ethanol versus a year ago. Stocks of ethanol are showing strength as production slowed over the past week. The DOE Fuel Ethanol Inventory Index is up 26.5% year-over-year. Slowing demand for corn through ethanol production is bearish for corn prices. The huge export sales miss is the main callout for corn over the last week. It seems that ethanol producers and farmers are waiting for lower prices before demand kicks in again.

Gasoline Prices

Gasoline is rising as concerns grow that refinery shutdowns in the Atlantic Basin will further reduce stockpiles on the East Coast. According to Bloomberg: “Prices climbed the most since June 29 as Europe’s largest refinery, Royal Dutch Shell Plc’s 400,000-barrel-a-day Pernis plant in the Netherlands, is conducting maintenance until early November. Supplies on the East Coast, including New York Harbor, the delivery point for futures contracts, were the lowest since October 2008 last week, Energy Department data show.”

Correlation

Charts

Howard Penney

Managing Director

Rory Green

Analyst