The Street has been pretty bullish on Urban Outfitters (URBN) and rightfully so with the stock up +50% since May. Keith added URBN to our Real-Time Positions this week as a long and our Retail team supports URBN, albeit with reservations.

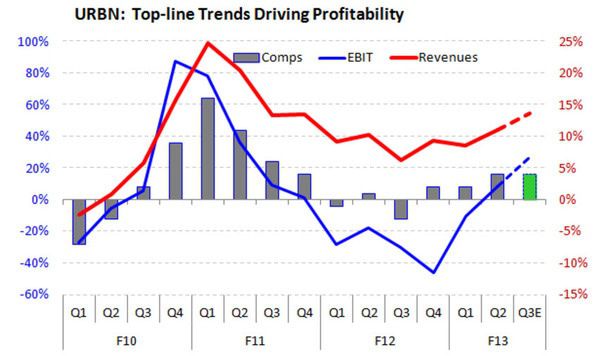

Revenues and comps are trending upward and have been since Q1 of fiscal year 2013. The company revised comp guidance (to a positive tune) earlier this month, pleasing sell-side analysts yet again. What URBN seems to “get” is that it needs to execute and run its business in a tight, efficient matter. Three notes that Retail Sector Head Brian McGough pointed out in a note back in May say it all:

The message is simple:

-Hire all the right talent.

-Empower each of them to come up with a concise plan, to which they will be held accountable.

-Give them the financial and human resources to achieve the plan.

And that’s what you have with URBN. The stock is now more expensive than it was back in May, but we still like it and believe betting against URBN is simply the wrong choice at this point in time.