Positions in Europe: Short EUR/USD (FXE); Long German Bonds (BUNL)

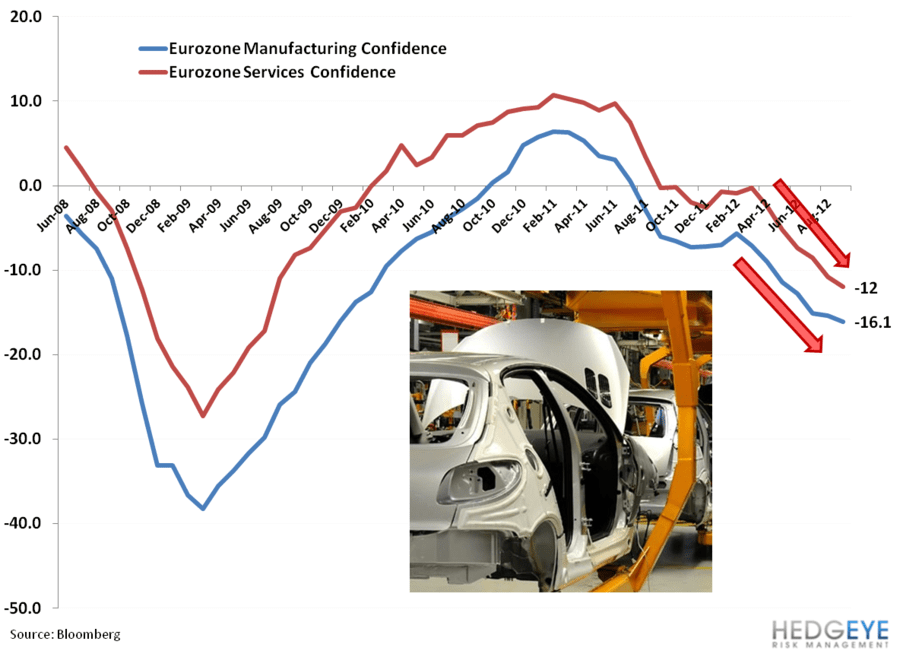

The charts below show very definitively that confidence figures across the Eurozone continue to roll. Business, Consumer, Economic, Industrial and Services confidence figures all fell in the September reading, marking 6 to 7 months of consecutive decline.

Here we’ll note that the data from the Eurozone continues to paint a challenged fundamental picture over the intermediate to longer term. These confidence figures are but one piece of the puzzle demonstrating the intersection between expectations for slowing growth and the uncertainty on the direction of the Eurozone. Eurocrats continue to suspend reality and Draghi’s “unlimited” put will continue to fuel a disconnect between the health of the economy and performance of capital markets.

As we see it, there is a long and uncertain road for the Eurozone moving from a monetary union to a monetary union with a fiscal union, including a banking union. We’ve already seen much push back from Germany on terms of a banking union, and expect push back if and when countries are required to give up their fiscal sovereignty to Brussels.

In the wake of Draghi’s unlimited announcement (9/6), this week has shown an increase in Eurozone sovereign yields (and CDS spreads). We expect that the markets and the EUR/USD cross could get a lift (but likely just a short-term one) from the inevitable announcement of the ECB to engage the OMTs program to buy sovereign bonds from such countries as Spain and Italy. However, market movement will largely depend on the severity of the conditions demanded in return for the buying. Yet our hunch is that the ECB will have loose and/or forgiving terms in any case, which would likely set us up to fade any Eurozone equity market and EUR/USD strength.

Matthew Hedrick

Senior Analyst