“A dog is not considered a good dog because he is a good barker.”

-Buddha

There are a lot of things I love about Eastern culture. One of them is the deep simplicity of their quotes. If I need to channel my inner-Buddha this morning to make a buy call, so be it.

Back to the Global Macro Grind…

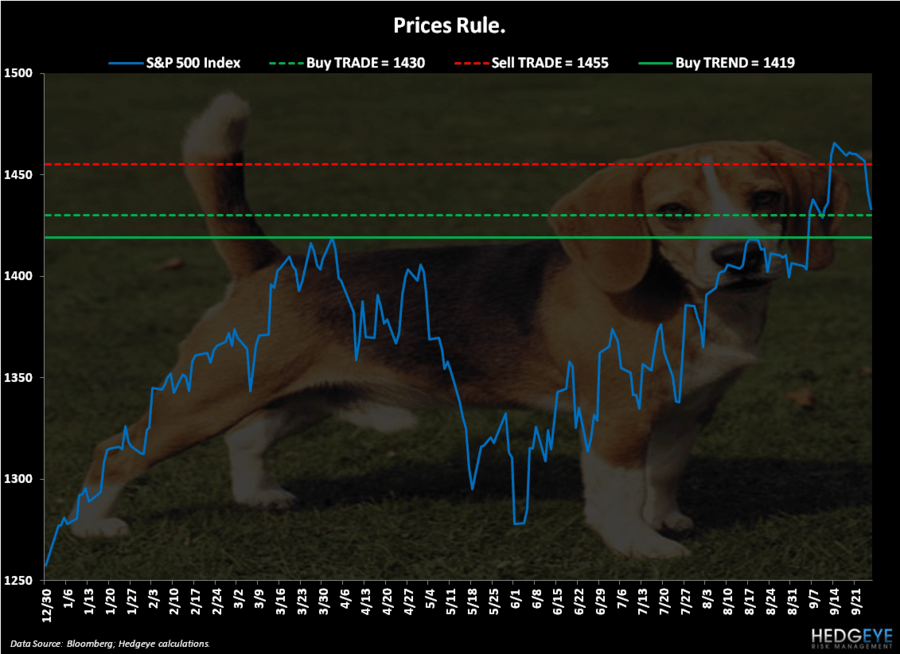

So, after a 41 handle (-2.8%) drop in the SP500 from the Bernanke “Buy Everything” top, US stocks have been down for 7 out of the last 8 days. I heard more crickets than I heard bulls yesterday. Weird.

Sometimes I like to bark. And sometimes that means my cage gets kicked by my central planning overlords too. But that’s ok. I’m just that dog in your life that never goes away. I have big teeth. And when I say “Buyem!” (with a smile), I kind of look like a little bull too.

“Buyem!”

That’s what my intraday note at 11:18AM EST was titled yesterday. In addition to the list of 7 long ideas I listed in yesterday’s Early Look note, we made the following moves:

- Covered Gold (GLD) at immediate-term TRADE oversold

- Bought Taiwan (EWT) at immediate-term TRADE oversold

- Covered Discover Financial (DFS) at immediate-term TRADE oversold

- Bought Consumer Discretionary (XLY) at immediate-term TRADE oversold

- Covered Burger King (BKW) at immediate-term TRADE oversold

In other words, when I start barking buy/cover or sell/short, it’s always based on the same repeatable process. Infrequently do I get all of my Global Macro signals at the same time as I get my bottom-up (single stock) signals. But when I do, that’s when I lean long or short. The process works both ways.

This is where I can get a lot better at this game, and I will. With more reps, mistakes, and successes, I’ve learned the game by playing it. Sure, some of my lovers out there will say “he does it with a paper portfolio”, and that’s fine. I hear them barking too. But I highly doubt they’d have the guts to show the entire world every move they’ve made for the last 5 years anyway.

From the day that I started this company, I’ve believed in one very simple set of Canadian-American principles: Transparency, Accountability, and Trust. I care less about the tone of my barking than I do the results. This game can be loud and it can get messy. Anyone who wants me to hold some high level of Ivy League gravitas wants me to be someone I am not.

Back to the why…

- Immediate-term TRADE oversold is as oversold does

- Immediate-term TRADE overbought in both Bonds (UST) and the Buck (USD), complimented that equity oversold signal

- Immediate-term TRADE overbought at VIX 17.37 was another critical intraday risk management signal

US Equity Volatility’s (VIX) inverse correlation to the SP500 is as relevant (some of the time) as SPY versus USD is. Never mind the pooch metaphors, those signals were yelling at me yesterday.

With my Correlation Risk signal in hand, I then looked forward at my Global Macro Calendar Catalyst playbook, which had the following bullish catalysts:

- Q2 US GDP report (this morning) will only add fuel to the Bernanke Bailout fire

- Both month and quarter-end markups for Q3 2012 are in play in between today and Monday

- China’s Golden Week (and 18th Party Congress) is pending for the next 2 weeks

That last one only matters in terms of the manic media’s perma-perpetuating of rumors about China “stimulus.” All it takes is for Chinese stocks to stop going down and they’ll say it’s because something big is coming. The Shanghai Composite got just that overnight, having one of its biggest bounces (off the lows) in weeks (+2.6%).

We have 12 LONGS and 3 SHORTS for this morning’s open. It’s probably fair to stop calling me a bear now – just call me a dog. You can pet and feed me with bullish data points. I won’t bite.

My immediate-term risk ranges for Gold, Oil (Brent), US Dollar, EUR/USD, 10yr UST Yield, and the SP500 are now $1, $106.41-111.44, $79.22-79.98, $1.28-1.30, 1.62-1.71%, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer