“Free-Market capitalism offers the most efficient and just way to order an economy.”

-George W. Bush

While it’s a shame that when short-term politics met economic gravity that neither Bush nor Obama gave anything other than lip service to one of America’s greatest economic ideals, that doesn’t mean all is yet lost. Arresting the un-American trend of centrally planned markets may very well be our greatest opportunity.

While I’ve had some big market calls wrong in the last month, I haven’t been wrong on the fundamental realities born out of Big Government Interventions. First, Policies To Inflate slow growth. Then they slow corporate earnings. Bernanke Bailout Bulls can blame Europe for yesterday’s decline, or they can pull up a chart of Caterpillar (CAT). Markets don’t lie; politicians do.

To give the aforementioned quote the appropriate context, it comes from a book I’ll be critically reviewing in the coming weeks: The 4% Solution. Bush wrote the Foreword and admirably prefaced his comment about American Liberty by holding himself accountable. He admits that “market-distorting government policies” played a big part in the 2008 crisis. God help our children if we can’t learn from that.

Back to the Global Macro Grind…

At the top of the market’s performance chasing squeeze (September 14th), we didn’t hide from our Q2 2012 Macro Theme, The Last War: Fed Fighting. We dug in our heels and stayed true to our process. Commodity inflation is not economic growth. It slows growth.

Headline this morning from Bloomberg: “Fed’s Plosser Says QE3 Risks Fed Credibility, Won’t Boost Jobs”

Agreed.

I’ll get to why I started covering shorts and buying stocks more aggressively yesterday in a moment, but first let’s rewind the tapes on what just happened after Bernanke pinned market prices at their YTD highs on no-volume:

- US stocks are down for 6 of the last 7 days (down -2.2% from the intraday high of 1474 Friday September 14th)

- CRB Commodities Index has lost -4.3% of its value in a straight line; Oil snapped TAIL risk support of $111.44 (Brent)

- US Treasury Bonds (10yr yield) just ripped a +13% move (yields down from 1.9% to 1.65% this morning)

I think Bernanke calls this something like “price stability.”

To their credit, a Perma-Bull might say, “a 2.2% correction is nothing.” Agreed. It’s only something if you bought the 1474 SP500 top in the Big Beta Sectors, with leverage. Underneath the beta-chasing hood, here’s what’s happened from the September 14th high:

- Financials (XLF) = down -4.2%

- Basic Materials (XLB) = down -4.2%

- Energy (XLE) = down -4.0%

While bulls sounded more like crickets into yesterday’s close, I can assure you that buying high and selling low, if done repeatedly for no other reason than chasing a benchmark, will leave a short-term performance mark.

What did we do? It’s all #timestamped, so you don’t have to take my word for it, but I’m encouraged that I didn’t meet my pre-September 14th mistakes with more mistakes-upon-mistakes. During the 1.5 week correction we sucked +1.71% of alpha out of the long side of Utilities (XLU) and, instead of buying a US Index into yesterday’s oversold close, we bought Apple.

Bought APPL? Yep. Not my 1st rodeo riding beta – it’s all about managing the risk of the immediate-term range. In a world where both Growth and #EarningsSlowing are going to dominate fundamental news-flow, I think investors will buck up for the growth that they can find.

Under the current US central planning regime of Obama, Bernanke, and Geithner, I think there’s a better chance of my becoming an adjunct professor of charlatan Economics at Yale than the USA seeing a 4% GDP print anytime soon. That’s what makes growth stocks attractive when A) you can find them, and B) they are on sale.

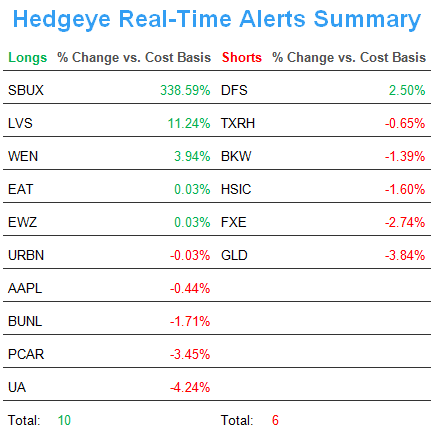

To review our Real-Time Positions, we have 10 LONGS and 6 SHORTS. On the long side, the best long-term Growth Ideas are:

- Las Vegas Sands (LVS)

- Apple (AAPL)

- Paccar (PCAR)

- Starbucks (SBUX)

- Under Armour (UA)

- Urban Outfitters (URBN)

- Brinker (EAT)

We also bought Brazil (EWZ) on red yesterday. While the government is moving towards making up its inflation numbers like Japanese, US, and European governments do, Brazilian economic growth looks ready to slow at a slower-rate. On the margin, that’s better than bad.

Unlike in the USA, where the manic media is attempting to tell you that yesterday’s Consumer Confidence print of 70.3 for September is bullish (see Chart of The Day for the historical context of US confidence – it’s lower than where it was in the 1970s), Brazilian Consumer Confidence clocked a 122.1 for September! That’s the kind of confidence we need.

To Review: during the only 2 sustainable +4% US GDP Growth runs of the last 40 years:

- 1 (Reagan, Strong Dollar) = US Consumer Confidence tracked between 90-120

- 1 (Clinton, Strong Dollar) = US Consumer Confidence tracked between 100-140

In other words, USA is not Brazil. Today’s American Consumer Confidence (oscillating between 40-70 during Bush & Obama Dollar Debauchery Administrations) reflects, precisely, what the zeitgeist in America feels like. Brazil's confidence tracked between 95 and 120 from 2005 to 2010. That's the kind of confidence we need.

This is not the country I came to in the mid-1990s. This is not a “free-market” either. This needs to change, just like my positioning did.

My immediate-term risk ranges of support and resistance for Gold, Oil (Brent), US Dollar, EUR/USD, UST 10yr Yield, AAPL, and the SP500 are now $1, $105.74-111.44, $79.15-80.59, $1.28-1.30, 1.63-1.72%, $671-693, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer