SPLS used 10,155 characters in its mammoth press release. It would have been easier to simply say, ‘we’re changing everything’ and top out at 25. The risk embedded in this model is severe.

Struggling retailers are like people with severe obesity – it takes them a long time to get so ill. SPLS is now officially obese with its press release surrounding how it is going to change the company, but we’re astonished with how quickly it got there. After all, SPLS has already been known as having one of the best management teams in retail. Heck, I even sourced analytical talent on my own team from SPLS, and yes, I can say that there are a lot of very smart people there.

But those classic rock faithful (and no to our interns, Nirvana is not Classic Rock) will know that Keith Moon, drummer from ‘The Who’ told Jimmy Paige that his new band will go over like a Led Zeppelin. That’s what SPLS smells like here. But without the success of selling 200 million albums thereafter…

Think about it…when you put great people in a terrible industry – not only mass big box retail – but big box office supplies retail where they have two bleeding competitors in Office Max and Office Depot and compete with everyone from Wal Mart to Radio Shack, to Best Buy to Ikea, then the job will win 9 times out of 10 and the ‘great person’ will walk away a winner only 10% of the time. Not good odds.

Let’s look at what this company is trying to do

- integrate its retail and online offering,

- increase investment in its online businesses,

- reorganize its operations,

- implement senior leadership changes,

- initiate a multi-year cost savings plan, and

- restructure its International Operations

Let me just say that any ONE of these is an undertaking that is so incredibly risky. But to do all six simultaneously? There is absolutely no shot of this working out – at least not without some more severe pain before they see relief. There are two things that bother us the most.

- That they think they can do this while cutting costs. Mark our words, there has never been a retailer that has made changes like this to ‘accelerate growth’ while cutting costs and has had the strategy work. One of them is trying now. It rhymes with KC Blenney. And no, I’m not saying that to be sensationalistic. This could be another JCP. It’s business is actually less defendable than JCP’s is. The problem at JCP is that the model is so expensive. But the idea is a good one. Here, I’m not even sure what the idea value proposition is.

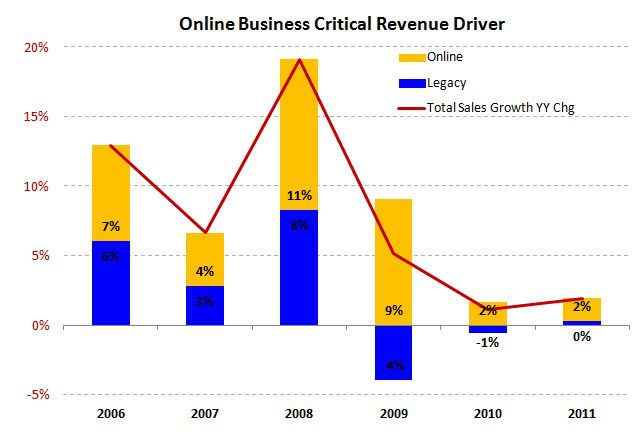

- We should have seen this, at least in part. When looking at the company’s percent of sales coming from on-line, 31% sales growth came from on-line in the four years ending calendar 2009. Despite the added boost from acquiring Corporate Express in 2008, the contribution of on-line to total growth slowed from an average of 8% per year over four years to only 2% in each of the last two topping out at 42% of sales vs. 40% 3-years prior and 27% 6-yrs ago. The company simply stopped spending on its fastest growing business. Hate to break it to them, but spending again now means they possibly benefit in 2 years. Not today.

- In the interim, these reorg costs will be steep, and very dynamic. All competitors will be salivating over this.

The stock looks so cheap. But valuation need not apply. They own less than 3% of their stores, and have little else to monetize a breakup value. Maybe an Ackman-type steps in and makes noise, but the company is already making a ton of noise on their own. You can hardly argue complacency to any sane Board member or sympathetic activist. But doesn’t 8x earnings look great? Not if the real multiple is 30x. Maybe they should move to Plano.