TODAY’S S&P 500 SET-UP – September 25, 2012

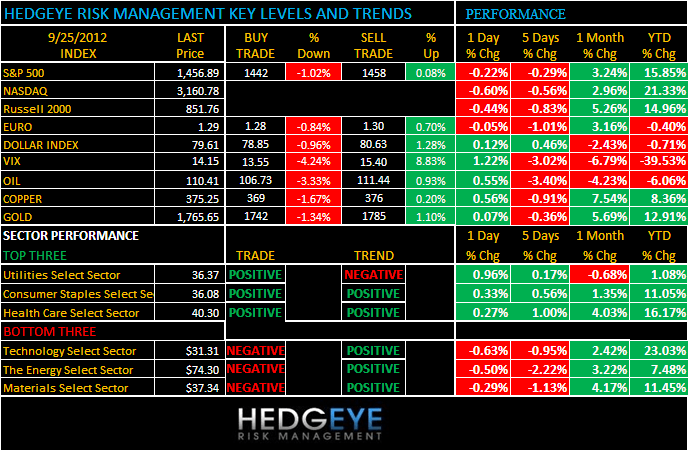

As we look at today’s set up for the S&P 500, the range is 16 points or -1.02% downside to 1442 and 0.08% upside to 1458.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 09/24 NYSE -586

- Decrease versus the prior day’s trading of 526

- VOLUME: on 09/24 NYSE 625.57

- Decrease versus prior day’s trading of -65.42%

- VIX: as of 09/24 was at 14.15

- Increase versus most recent day’s trading of 1.22%

- Year-to-date decrease of -39.53%

- SPX PUT/CALL RATIO: as of 09/24 closed at 2.59

- Up from the day prior at 1.21

CREDIT/ECONOMIC MARKET LOOK:

TREASURIES – as wrong as we were that Bernanke couldn’t go to infinity is as wrong as his market call looks all of a sudden, especially in the eyes of who has had #GrowthSlowing nailed for all of 2012 (the bond market); 10yr UST yield literally straight down since peaking post Bernanke Sept13 day from 1.89% to 1.69% last (Yield Spread at 2wk lows).

- TED SPREAD: as of this morning 27.09

- 3-MONTH T-BILL YIELD: as of this morning 0.11%

- 10-Year: as of this morning 1.69%

- Decrease from prior day’s trading of 1.71%

- YIELD CURVE: as of this morning 1.43

- Down from prior day’s trading at 1.45

MACRO DATA POINTS (Bloomberg Estimates)

- 7:45am/8:55am: ICSC/Redbook weekly sales

- 9am: S&P/Case-Shiller 20 City (M/m) SA, July, est. 0.8%

- 10am: Conference Board Consumer Conf. Index, Sept., est. 63.2

- 10am: Richmond Fed Manuf. Index, Sept., est. -6 (prior -9)

- 10am: House Price Index (M/m), July, est. 0.6% (prior 0.7%)

- 11am: Fed to purchase $4.5b-$5.5b notes due 11/15/2020-8/15/2022

- 11:30am: U.S. to sell $40b 4-week bills

- 1pm: U.S. to sell $35b 2-year notes

- 4:30pm: API inventories

GOVERNMENT:

- Obama set to speak at United Nations

- IMF releases portions of Global Financial Stability Report, including “The Reform Agenda: An Interim Report on Progress Towards a Safer Financial System,” 10:30am

- DARPA program manager Richard Ridgway discusses military’s use of mobile hotspot technology at Military Antennas Summit, 8am

- FCC Chairman Julius Genachowski discusses broadband challenges at Vox Media event, 10:30am

WHAT TO WATCH:

- Apple’s use of thin display seen driving iPhone 5 supply shortfall

- Spain sells EU4b of bills meeting maximum traget

- Schaeffler sells $2b stake in Continental to cut debt

- Billionaire Ellison increases Oracle credit line to $4.5b

- Digital Domain sale to Chinese-Indian venture approved by court

- Diego in talks to buy United Spirits stake: WSJ

- Nasdaq, Amazon to partner on cloud storage of financial data

- Foxconn resumes production at China plant after worker brawl

- Warner Music says Cohen resigns as CEO of recorded music

- Providence Equity Partners sells stake of under 10%: WSJ

- BAE CFO Lynas said to hold same role in proposed EADS merger

- AT&T to market business mobile security to consumers in 2013

- Chevron under EPA probe for avoiding refinery monitors in 2009

- California offers lowest interest rate in $1.75b bond sale

EARNINGS:

- FactSet Research Systems (FDS) 7am, $1.17

- Vail Resorts (MTN) 7:30am, $(1.56)

- Carnival (CCL) 9:15am, $1.43

- Synnex (SNX) 4pm, $0.93

- Jabil Circuit (JBL) 4:02pm, $0.58

- Copart (CPRT) Post-Mkt, $0.33

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

OIL – getting a +0.5% bounce this morn, but remains a bearish TAIL risk situation in our signaling model as long ast $111.44 Brent remains resistance; interesting that the US equity futures aren’t up w/ oil up; EUR/USD down again trumping that, as it should.

- Oil Rises in New York on Speculation Last Week’s Drop Overdone

- Pork Supply Shrinks to Lowest Since 1975 on Drought: Commodities

- Copper Stockpiles in Shanghai Bonded Warehouses Seen at Record

- Silver in ETPs Set for Record as Central Banks Ignite Demand

- Soybeans Set to Rebound From Six-Week Low on Importer Purchases

- Kazakhstan Expands Gold Reserves as South Korea Buys 16 Tons

- Palm Oil Snaps Five Days of Losses as Declines Deemed Overdone

- Oil Supply Rises Third Week Post Isaac in Survey: Energy Markets

- Bearish Bets on Potash Decline at Fastest Pace Ever: Options

- Iron Ore’s Rebound Poised to Peter Out on Weak Demand, ANZ Says

- Western Europeans Munch the Most Chocolate Globally, U.K. Leads

- Einhorn’s Losing Gold-Miner Strategy Endorsed: Chart of the Day

- Japan’s Nuclear Exit Extending Record Profit for Golar: Freight

- Pork Supply Shrinks to Lowest Since 1975

- Copper Advances in London After Report of Stabilization in China

CURRENCIES

EUROPEAN MARKETS

GERMANY – the Germans, meanwhile, told the French to go fly a kite this weekend on timing and are “now losing patience with Spain”; Merkel comments have dominated my tweet-stream sources since 430AM EST as European stocks move back to their lows; ITALY is down -4.7% (MIB Index) since Bernanke’s Infinity & Beyond say (Sep13).

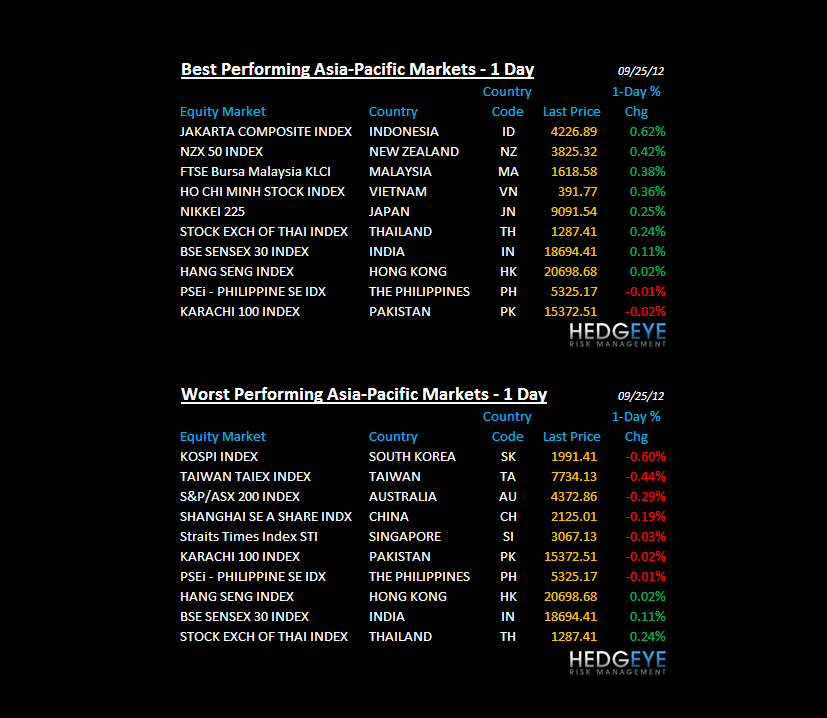

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team