Last week we held a conference that outlined our key scenarios for the upcoming Presidential and Congressional elections. We based these scenarios on a multifactor analysis of polls, electronic markets, and economic models. Our key conclusions were that the highest probability outcomes in order were:

- Democratic President, Republican House, and Democratic Senate

- Democratic President, Democratic House, Democratic Senate

- Republican President, Republican House, Republican Senate

Since our call last week, President Obama’s chances of re-election have only increased on Intrade and are now north of 70%. This is Obama’s highest level on Intrade this electoral cycle. Intuitively, this makes sense as Intrade typical trades off of the national polls and the positive spread for Obama has been widening.

In our national poll aggregate, the race was effectively tied on September 6th 2012 at 46.7 to 46.7. This coincided with the end of the Republican convention. Since then Obama has widened out his margin and currently has a lead of +3.7. This is beyond the margin of error in most polls. Currently, the benefit of a convention bounce is now likely out of Obama’s numbers, which suggests, in theory, that he has now opened a sustainable edge over Romney.

Historically, the polling at this point of the election cycle has been very accurate for assessing a final outcome. Since 1936, of the 19 candidates who led in the polls at the point, 18 won the popular vote and 17 won the electoral college (Al Gore was the lone exception here). As well, as Nate Silver touched upon in his insightful blog today, there is typically no tendency for races to shift to the challenger at this point in a Presidential election.

At face value, the state of the race does not look great for the Republican faithful as an Obama victory appears increasingly likely. This, of course, assumes one thing, namely that polls are an accurate reflection of the actual electorate. Increasingly, there is a view that many polls are skewed based on abnormally high Democratic turnout in 2008.

Based on the exit polls in 2008, there were approximately 7% more Democrats in the electorate. This is really no surprise given the disenchantment with the Bush years and the excitement around then Senator Barack Obama’s candidacy. Given that most voters vote along party lines, this edge in Democrats ultimately equated very closely to Obama’s edge in the popular vote at +7.6 in 2008.

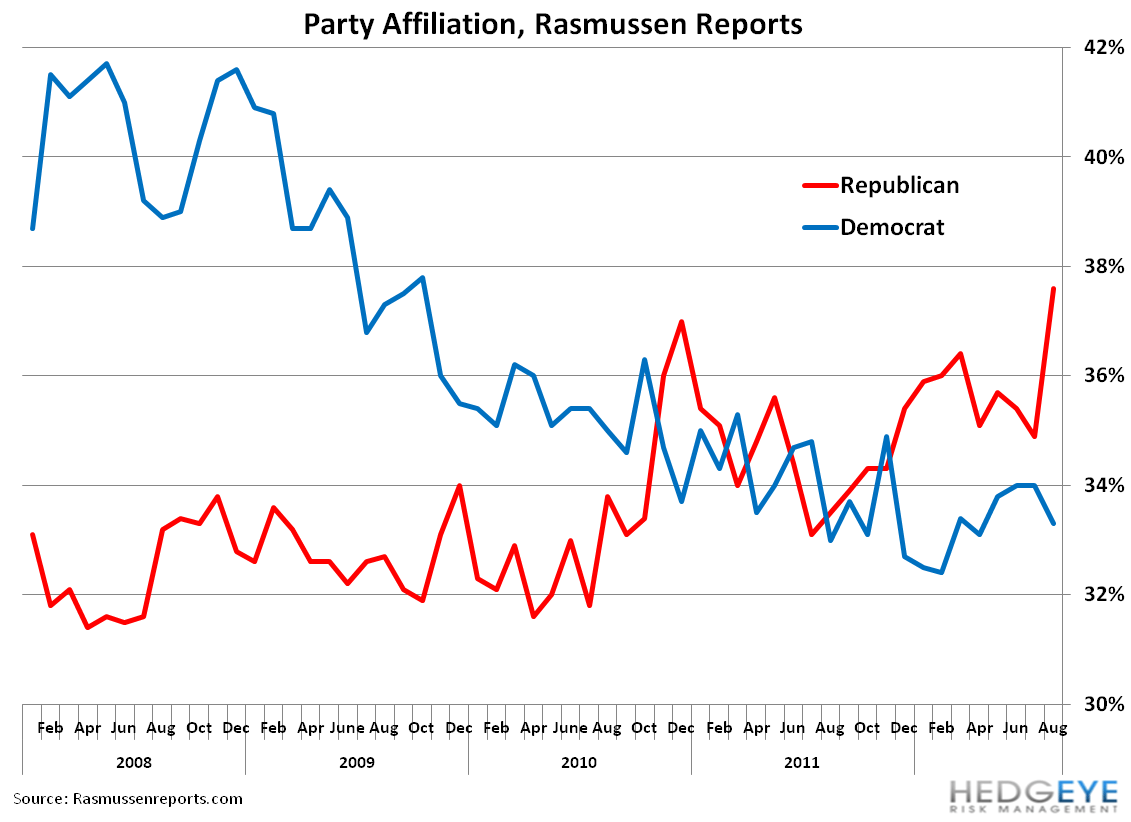

As we mentioned last week, there is some evidence that turnout this election could favor the Republicans and that more of the electorate identifies themselves as Republicans versus 2008. Rasmussen actually runs a monthly poll on voter identification and in the September 1st release found that 37.6% of Americans consider themselves Republicans. This is the highest reading in this poll since it began in 2002. In November of 2008, this poll had a +7.6% edge for Democrats over Republicans.

An example of recent poll that utilizes skew towards Democrats is the Reason-Rupe public opinion survey released on Friday. The poll found that 48% would vote for Obama and 43% would vote for Romney. Interestingly, the poll also found that 28% of those polled viewed themselves as Republicans and 36% polled viewed themselves as Democrats for a staggering 8% advantage for the Democrats. Assuming the Rasmussen party ID poll is accurate, the Reason polls and other polls may potentially be overstating voter turnout by party. By non-skewing the Reason poll, Romney basically takes an almost 3 point lead.

In the most recent national poll from Politico, 43% of those polled identify themselves as Democrats and 40% identify themselves as Republicans. The Obama edge in the poll is . . . you guessed it . . . +3. The nature of the sample and the weighting it gives either party is ultimately consistent with the outcome and headline number of the poll.

In the table below, we’ve highlighted a break out of voter ID from the Associated Press poll which shows this point in detail. The Likely Voter survey showed that Democrats had an edge of +1 over Republicans in poll, probably a reasonable sample. This breakdown effectively matched the results of the poll which gave Obama a +1 edge. In the registered voter category, Democrats had a +7 point edge. To the extent that a pollster, such as Gallup, is still using registered voters it is likely to overstate the results for Obama.

If Republicans maintain their edge in voter ID polls and national polls continue to oversample Democrats, the ultimate surprise in November could well be failure of polls and a surprise showing by the Republicans versus the expectations of pollsters. The aforementioned poll from Rasmussen will be a key tell in this regard given its predictive ability on voter ID in 2008 and 2010.

Daryl G. Jones

Director of Research