Carnival will report F3Q earnings on Tuesday. We believe the company will maintain FY 2012 yield guidance and give a solid 2013 yield outlook. Not surprisingly, the FY 2012 EPS guidance range may be lowered slightly due to a 16% rise in bunker costs since the end of June. We’re forecasting $1.86 for FY 2012 EPS and $2.64 for FY 2013 EPS, in-line and 6% above the Street, respectively.

CCL should reiterate the tough yield comps in the Caribbean, particularly in F1Q 2013, but stress that early European summer pricing is picking up due to easy comps. Given that CCL has risen 11% since F2Q earnings and trading at 14x forward earnings (close to 20 year average), we think bullish expectations are mostly priced in the stock.

SEPTEMBER PRICING TRENDS

Weakness in Caribbean pricing for some last minute bookings is dragging down F4Q performance but that is offset by further improvements in European pricing. While it’s too early to make a call given the limited summer 2013 itineraries, Costa pricing looks like it is rebounding strongly. For the most part, 2013 pricing looks solid, which is expected given easy comps in Europe after two years of substantial price discounting.

Here are some other conclusions from our cruise pricing survey. The charts below track pricing trends on a relative basis—i.e. prices relative to that seen on the last earnings call i.e. RCL - July 20 and CCL - June 22.

CCL

- Caribbean continues to be a concern. With some newcomers entering the market in 2013 (e.g. Carnival Valor, Princess ships, Norwegian Breakaway), pricing looks weak. Caribbean pricing is down 3% in F1Q 2013, F2Q 2013 pricing is flat, and very early F3Q pricing is also down slightly. F4Q 2012 is also being dragged down by Caribbean weakness. The good news is that the trend in September saw sequential improvement from a month ago.

- Europe pricing continues to improve in F4Q 2012. However, Cunard Europe pricing continues to lag, particularly in F1Q 2013.

- Mexico pricing is trending modestly higher in F4Q 2012 and F1Q 2013.

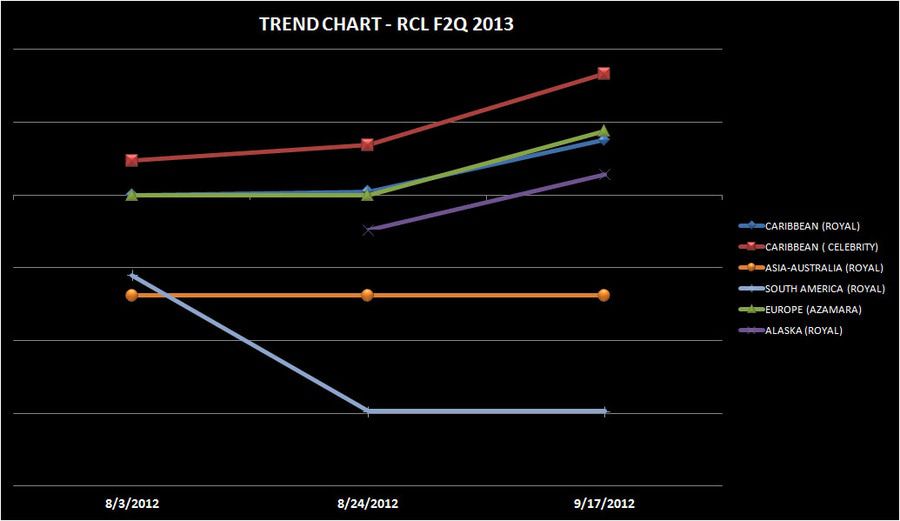

RCL

- F4Q 2012

- In the Caribbean, modest discounting is seen for some last minute bookings by Royal brands. Celebrity pricing remains robust YoY but trend is deteriorating.

- Europe is looking better though remain much lower YoY.

- Asia pricing is solid.

- While sparse in itineraries, South America pricing continues to weaken.

- Caribbean pricing is slightly up in F1Q 2013 but down modestly in early F2Q 2013. Like CCL, trend is improving.

- Asia pricing is higher in F1Q 2013.