“Pain plus reflection equals progress.”

-Ray Dalio

As a hedge fund analyst, turned Portfolio Manager, turned Canadian-American Entrepreneur, there are very few quotes that resonate with me more than that one. Ray Dalio remains, The Man.

In order to really learn how to win, I need to feel the pain of my mistakes. If I’m not making mistakes, that means I’m probably not pushing myself hard enough to try something new. John Cage frames that thought about risk taking another way: “I can’t understand why people are frightened of new ideas. I’m frightened of the old ones.”

As you watch the bull market crowd cheer on 10 million iPhone5 sales this weekend but, at the same time, beg for more of what has not worked (Spain Bailouts), remember that in order to foster Apple like innovation, we can’t incubate an American culture of socializing losses.

Back to the Global Macro Grind…

For me at least, last week’s pain was this week’s gain. With the US Dollar Index having its 1st up week in the last 7, the CRB Commodities Index has had its long-term TAIL spanked for a -4.4% wk-to-date move.

Within the parameters of our Multi-factor, Multi-duration Risk Management Model, we focus on 3 key durations of risk (TRADE, TREND, and TAIL). We define TAIL risk on a bi-partisan basis; it works both ways (up and down).

Across the Global Macro waterfront, here are some key TAIL duration risks (3 years or less) for long-term risk managers to consider:

- US Dollar Index long-term TAIL support = $78.11

- CRB Commodities Index long-term TAIL resistance = 309

- Oil (Brent) long-term TAIL resistance = $111.44/barrel

- US 10yr Treasury Yield long-term TAIL resistance = 1.91%

- EUR/USD long-term TAIL resistance = $1.31

The first and last TAIL risks are the mirrors of one another. One up, one down. That’s why I’ve been saying for a while now that if you get the US Dollar right, you get a lot of other things right. That’s where most multi-duration Correlation Risks associated with Policies To Inflate live.

The other thing that you need to get right is economic growth. Put another way, if you’ve had US and Global Growth right in 2012, you’ve had Treasury Bonds right (long). Despite all of the broken promises from Bernanke on delivering you the elixir of a centrally planned life, the bond market continues to make a series of higher-lows, as the 10yr yield’s TAIL resistance remains intact.

When you get both A) the biggest Ball Under Water Macro trade of the last decade (US Dollar) and B) US Growth (demand) right, you have a tremendous opportunity to get the holy grail of investing right – timing. Personally, I’ll always have room to improve on that.

But does Ben Bernanke? Who holds this man accountable? With a lack of progress, is America’s economy about to experience the most amount of pain yet? If we go back into the soup, what will he do next? Is he out of bullets?

If you know the answer to these critical long-term questions, tweet me.

In the meantime, here’s what you get for your Burning Bernanke Bucks:

- Unemployment: US Jobless Claims Rising on a 4-wk rolling average basis to 378,000 (382,000 reported for this wk)

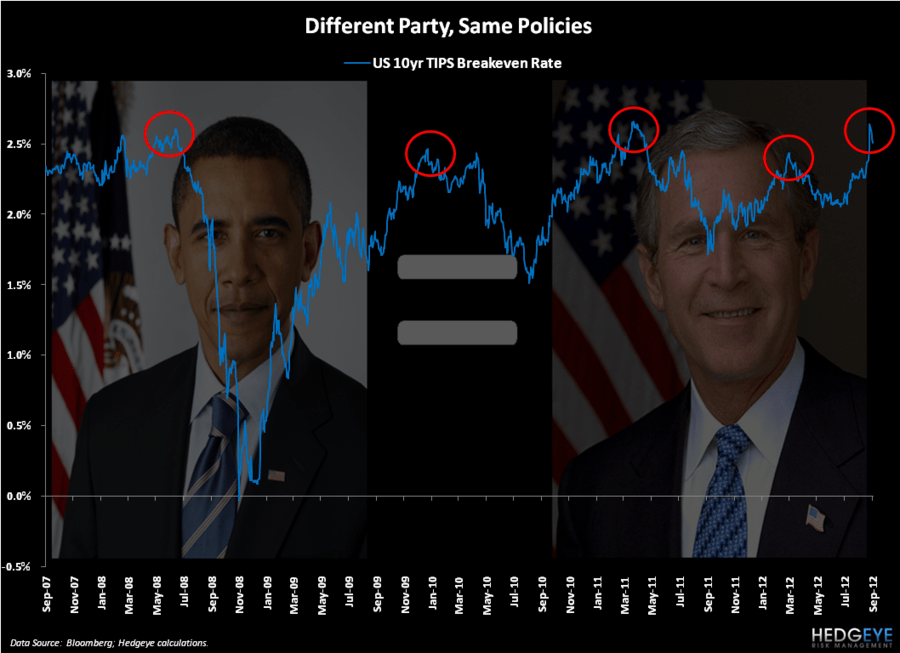

- Inflation Expectations: 10yr Breakevens testing all-time highs immediately following Bernanke’s decision last Thursday

- Fund Flows: ex-ETFs, US Equity Fund Flows were negative (again) at -$1.9B wk-over-wk (outflows)

In other words, at 4.5 year highs in the US stock market, this is what multiple “Quantitative Easings” and countless “communication tools” about the pending Qe-upon-prior-Qe got us:

- Higher US unemployment than we had in 2009 (unemployment rate in January 2009 was 7.8%)

- The 3rd of 3 Greenspan/Bernanke Asset Bubbles (Commodities) that every money manager is dared to chase

- No trust and/or volume in what used to be America’s beacon of free-market capitalism (the US stock market)

Great job, dude.

Both Bush and Obama signed off on this guy. See the Chart of The Day (10yr Breakeven Inflation Expectations 2007-2012) and you tell me how much longer he can keep America’s Purchasing Power (US Dollar) down, Savings Rates on hard earned moneys at 0%, and show zero reflection on his academic dogma’s mistakes, never mind progress.

My immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, EUR/USD, 10yr UST Yield, and the SP500, are now $1, $108.03-111.44, $78.61-80.43, $1.29-1.31, 1.72-1.87%, and 1, respectively.

Best of luck out there today and enjoy your weekend,

KM

Keith R. McCullough

Chief Executive Officer