Darden are reporting earnings tomorrow and, while we expect management to put as positive a spin on things as possible, we would not be betting on many positives emerging tomorrow.

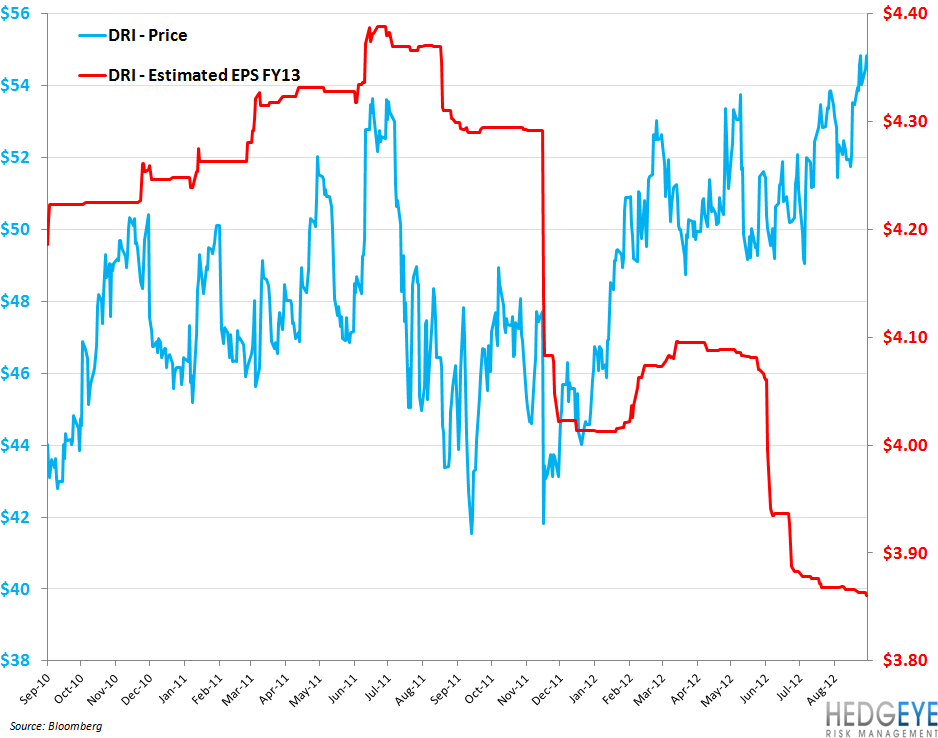

Darden earnings are due out before market open tomorrow and we remain bearish on the stock as price action has decoupled from the fundamental reality that drives earnings. Here is a quick update on our thoughts. They have not meaningfully changed since our 8/30 post, “DRI: EXPECTATIONS ARE THE ROOT OF ALL HEARTACHE” but the price of the stock has. We are expecting FY13 earnings to come in 3% below the Street’s expectations.

Same-Restaurant Sales

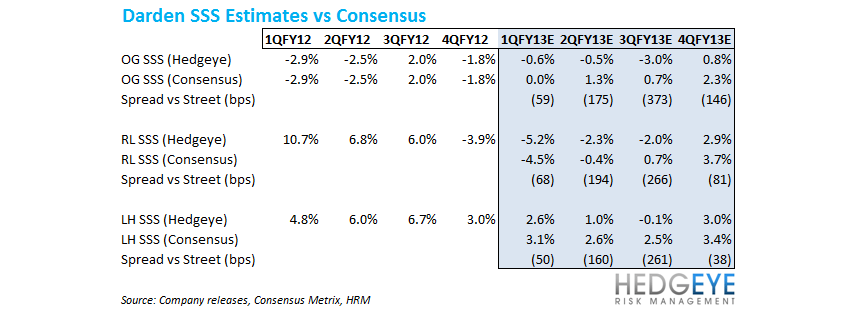

We believe that the Street is far too bullish on the same-store sales recovery at Olive Garden and Red Lobster and, by implication, the casual dining industry. As the Restaurant Value Spread continues to roll over and pressure the pricing power of the restaurant industry, we do not think the value proposition at Olive Garden and Red Lobster is appealing to consumers on an ongoing basis. We expect Darden to lag the industry from a same-restaurant sales perspective in 1QFY13 and believe that, as bad as that would be for the stock, there is likely worse to come as the year progresses.

Quantitative Levels

This is a stock that will feel it as the US consumer feels the squeeze from higher gas prices and still-stagnant job growth. We can only speculate as to the divergence between earnings expectations and the stock price, but our best guess would be that some safety- or dividend-seeking investors have been increasing exposure to Darden recently. As our Black Book (email for a copy) argues, Darden's dividend is far from secure with the company burning cash to maintain its profile as a growing company with a best-in-category dividend yield.

As the chart below highlights, Keith's quantitative levels show TREND support at $52.34 and TRADE support at $53.61.

Howard Penney

Managing Director

Rory Green

Analyst