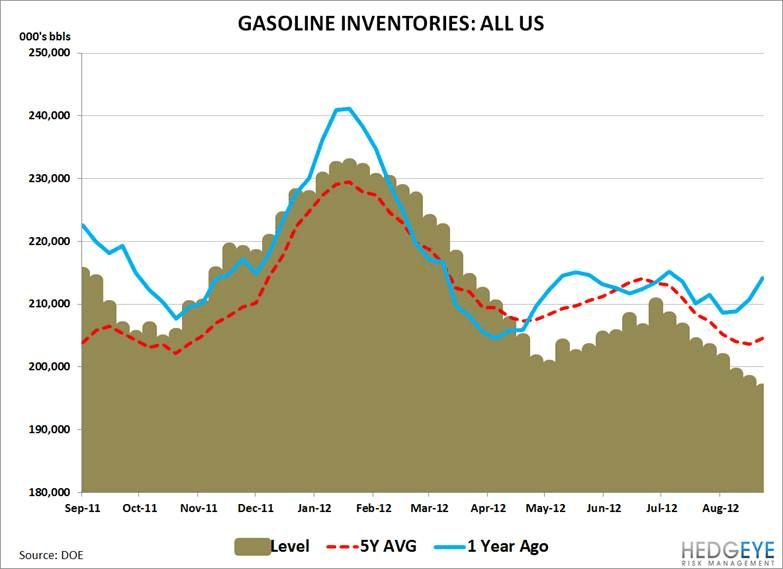

US energy product inventories are low, particularly gasoline and diesel fuel. Despite US refineries cranking at full speed and utilizing a high level of capacity, there are several reasons why we’re running low on gas and diesel. First, we’ve been increasing exports of fuel, sending diesel to Europe and gasoline to South America. We’ve also undergone a drop in refined product exports. Lastly, we’ve had weak domestic demand for refined products. People are busy trying to conserve gas when it’s $4 a gallon.

Provided the export market stays open, we expect product stocks to remain depressed relative to prior levels, which is positive for refining margins.