This note was originally published at 8am on September 06, 2012 for Hedgeye subscribers.

“Rather than a gambler, he was a speculator with an eye for good risks.”

-Carl Sandburg

That’s a quote from one of the better opening chapters I have read in 2012, “God’s Chosen Instrument”, in Jay Cooke’s Gamble – “The Northern Pacific Railroad, The Sioux, and The Panic of 1873.” (by M. John Lubetkin)

Few in this profession want to admit that there is a degree of gambling in what they do. But what, per se, would you call what we have all been forced to do in the last 6 months? Even if you have perfect inside information on what Draghi is going to do this morning, the market could do the exact opposite of what you think it should do on that.

Inside information? If you don’t think someone always knows something, you need “more time” on the job too. That’s as old as Jay Cooke’s legend in becoming the “financier of the Civil War.” One of the market’s richest men (before it all crashed in 1873), “Cooke bought members of Congress, bribed 2 Vice Presidents, built churches…” (page 1) etc., but still blew up his unlimited capital bet, in the end.

Back to the Global Macro Grind…

#Unlimited – that’s what she said. As in the woman who wrote this morning’s manic media headline on why the US stock market futures were up 8 handles. “Stocks rise on possibility of unlimited ECB bond buying.”

Imagine that for 3 more minutes. Never mind the most money ever printed into a central planning event… ever… by 9AM EST, “unlimited” moneys will fall from the heavens, Gold will go to $3000 and Oil will go to $200?

The storytelling out there is just getting awesome.

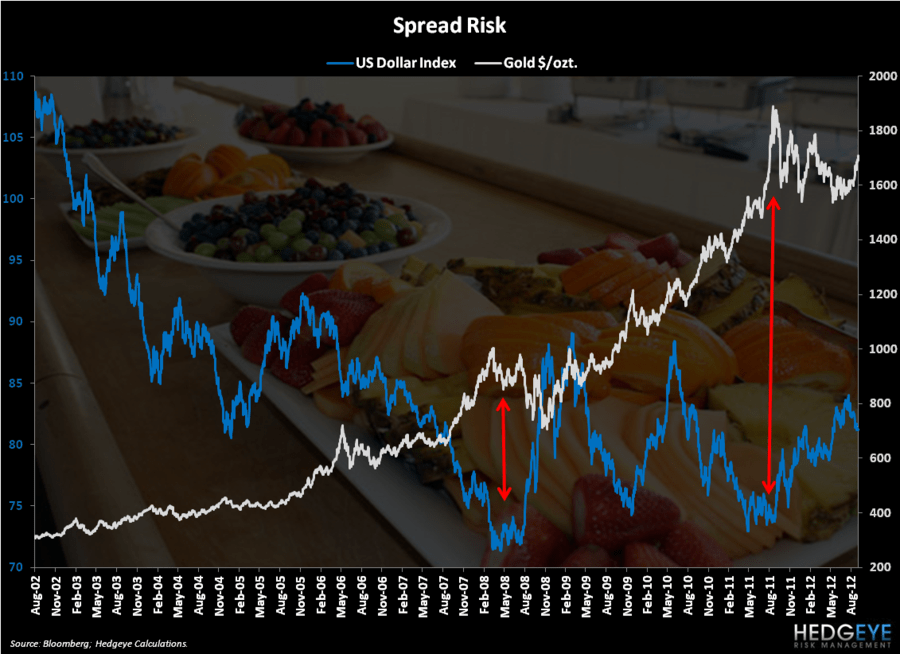

I’m short Gold here. On balance, until turning bearish on Gold in Q1 of 2012, I have been a Gold bull since 2003. I have #timestamped 35 long/short positions in the GLD since founding the firm in 2008 (been right 30x).

The more wrong I am on Gold (from here), the more right I’ll be on #GrowthSlowing.

Why?

- Inflation is not growth

- Inflation slows growth

So, if you are still hoping for economic growth, but at the same time want the Italian Eurocrat to go “unlimited”, Weimar-style, on the printing presses this morning, just be careful what you are cheering for.

Rather than roll the bones on what rumor is going to hit my tweet-stream next, this is what I am going to do on green this morning.

Drum-roll: sell.

That’s not my perma position (7 of my last 10 booked gains have been on the long side, and we’ve bought almost 50 tickers since the May-June 2012 lows). That’s just what I do (on green) at the high end of what we call our Risk Management Range.

When I give you my Risk Ranges at the bottom of the Early Look every morning, those are the immediate-term ranges of price risk that I am using to make my buy and sell decisions. Rather than a gambler, I’m just good at being disciplined, not swinging at outside pitches.

Since I wasn’t a good baseball player (I am Canadian), what other choice do I have? It’s hard enough to hit the big fat fastball of perfect information in this market when you feel like you see your pitch.

If markets haven’t humbled you yet, they will. If central planners think they have markets nailed now, they are about to get nailed.

With those long-term risk management realities vs. short-term rumors in mind, here are your risk ranges, across asset classes this morning:

- US Dollar Index = 81.11-81.89

- EUR/USD = 1.24-1.26

- US Treasury 10yr Yield = 1.54-1.63%

- CRB Commodities Index = 303-309

- SP500 = 1398-1414

- VIX = 16.91-18.92

- Russell2000 = 812-825

- Shanghai Composite = 2016-2089

- Nikkei (Japan) = 8532-8768

- EuroStoxx50 = 2407-2475

- DAX (Germany) = 6899-7065

- IBEX (Spain) = 7357-7611

- Oil (Brent) = $111.96-115.36

- Gold = $1675-1712

- Copper = $3.47-3.52

People can call me a gambler. They can call you a lover. They can call us “perma” whatever they want if the storytelling makes them feel certain about something that’s uncertain. The only thing I am certain about this morning is what my process is telling me to do next.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer