TODAY’S S&P 500 SET-UP – September 20, 2012

As we look at today’s set up for the S&P 500, the range is 25 points or -0.82% downside to 1449 and 0.89% upside to 1474.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 09/19 NYSE 473

- Increase versus the prior day’s trading of -341

- VOLUME: on 09/19 NYSE 643.72

- Increase versus prior day’s trading of 1.71%

- VIX: as of 09/19 was at 13.88

- Decrease versus most recent day’s trading of -2.12%

- Year-to-date decrease of -40.68%

- SPX PUT/CALL RATIO: as of 09/18 closed at 1.53

- Up from the day prior at 1.49

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 26.93

- 3-MONTH T-BILL YIELD: as of this morning 0.11%

- 10-Year: as of this morning 1.74%

- Decrease from prior day’s trading of 1.77%

- YIELD CURVE: as of this morning 1.49

- Down from prior day’s trading at 1.51

MACRO DATA POINTS (Bloomberg Estimates)

- 7:44am: Fed’s Rosengren speaks in Massachusetts on economy

- 8:30am: Init Jobless Claims, Sept. 15, est. 375k (prior 382k)

- 8:58am: Markit U.S. PMI Prelim, Sept. est. 51.5 (prior 51.5)

- 9:30am: Fed’s Lockhart speaks at Kansas City Fed conference

- 9:45am: Bloomberg Consumer Comfort, Sept. 16 (prior -42.2)

- 9:45am: Bloomberg Economic Expectations, Sept. (prior -22)

- 10am: Philadelphia Fed, Sept. est. -4.5 (prior -7.1)

- 10am: Freddie Mac mortgage rates

- 10am: Leading Indicators, Aug. est. -0.1% (prior 0.4%)

- 10:30am: EIA natural-gas change

- 11am: Fed to sell $7b-$8b notes due 6/15/2015-8/31/2015

- 11am: U.S. to announce auction sizes for 2-yr, 5-yr and 7-yr auctions

- 12pm: Federal Reserve Flow of Funds Report

- 1pm: U.S. to sell 10-yr TIPS (reopening)

- 1:30pm: Fed’s Kocherlakota speaks in Michigan

- 5pm: Fed’s Pianalto speaks in Ohio

- 6:30pm: Fed’s Bullard gives lecture at U. Notre Dame

GOVERNMENT:

- House, Senate in session

- Tax treatment of capital gains debated at joint hearing of Senate Finance, House Ways and Means, 10am

- House Small Business hearing on likely effects of sequestration on government contractors 1pm

- House Oversight panel holds hearing on Afghanistan, 2pm

- House Oversight panel holds hearing on Medicare, 2pm

- House Judiciary holds hearing on regulations, jobs, 10am

- Senate Homeland Security panel holds hearing on offshore profit shifting and the U.S. tax code, 2pm

- Senate Commerce releases results of investigation into consumer abuses by moving and storage industry, 10am

- SEC holds closed hearing on enforcement matters, 2pm

- FERC holds monthly meeting, 10am

WHAT TO WATCH:

- Chinese manufacturing survey points to 11th month of contraction

- Nike to spend $8b buying back shares over 4 years

- Liberty Global offers to buy remaining 50% of Telenet for $2.54b

- Spain sells EU4.8b of bonds, most since January

- BOJ scraps requirement for regular purchases of govt. debt

- CIC-led group said to pay $2b for 5.6% of Alibaba

- Norfolk Southern sees 3Q earnings at $1.18-$1.25 vs est. $1.63

- Bain Capital said to be in advanced talks to buy Apex Tool for $1.5b-$1.8b

- UBS more cautious on U.S. banks; cuts MS, Citigroup, Goldman

- Peugeot to sell Gefco stake for $1.04b to help cut debt

- SEC’s Gallagher says retail bond investors fighting headwinds

- Billabong bidder drops out leaving A$694m sale to TPG

- KBW ordered to face lawsuit by trustee for Guaranty Financial

- Capital Bank raises $180m in IPO, pricing below range

- GM said to plan bid for Ally Financial’s Europe, Latam ops

- American Airlines cancels 300 flights on maintenance delays and sick pilots

EARNINGS:

- IHS (IHS) 6am, $1.01

- Scholastic (SCHL) 7am, $(1.05)

- Rite Aid (RAD) 7am, $(0.07)

- ConAgra Foods (CAG) 7:30am, $0.35

- CarMax (KMX) 7:35am, $0.52

- Jefferies Group (JEF) 8am, $0.26

- Oracle (ORCL) Aft-mkt, $0.53

- Tibco Software (TIBX) 4:10pm, $0.27

- Cintas (CTAS) 4:15pm, $0.59

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

OIL – does Dollar UP matter? We don’t need an opinion on that; fact is that this is the 1st UP wk for the US Dollar Index in the last 7 and oil just got smoked for an -8% drop from the Bernanke Policy to Inflate SEP top; we continue to think that the Bernanke Bubble in Commodities is in the process of popping; long-term tops are processes, not points.

- Fed Stimulus Fading as Forecasters Say Best Is Over: Commodities

- Bakken Gain Triples Brent as Trains Oust Pipes: Energy Markets

- China, India Show Gold Is Expensive Insurance: Chart of the Day

- Gold Drops as Strengthening Dollar Erodes Demand; Platinum Falls

- Oil Falls to Six-Week Low on China Slowdown, U.S. Supply Surge

- Copper Falls Most in a Month on Concern About Global Slowdown

- Corn Falls as Record Brazilian Harvest May Ease Supply Concerns

- Sugar Rises as Demand May Rebound After Drop; Cocoa Declines

- Indonesia Will Relax 2014 Ore Ban to Increase Time for Smelters

- Rebar Drops Most in 11 Months as Chinese Manufacturing Shrinks

- China Overtakes U.S. as Largest Crop Importer, WTO Data Show

- Lonmin Pact With Illegal Strikers Sets ‘Dangerous’ Precedent

- Cosco May Order Supertankers Amid Rising China Oil Imports

- Copper to Extend Gain as Resistance Breached: Technical Analysis

- Chinese, Indians Buy Pink Diamonds as Rarity Clicks, Rio Says

- Shell Leads LNG Competitors Out to Sea With Biggest Ship: Energy

CURRENCIES

EURO – if $1.29 EUR/USD doesn’t hold, watch out below for the Euro (no immediate-term TRADE support to $1.26); this is the #1 issue we had w/ Bernanke Expectations, Spread Risk – it’s as obvious b/t the Euro and USD as it is USD and CRB; wicked correlated in the short-term, so stay disciplined with your risk management levels here.

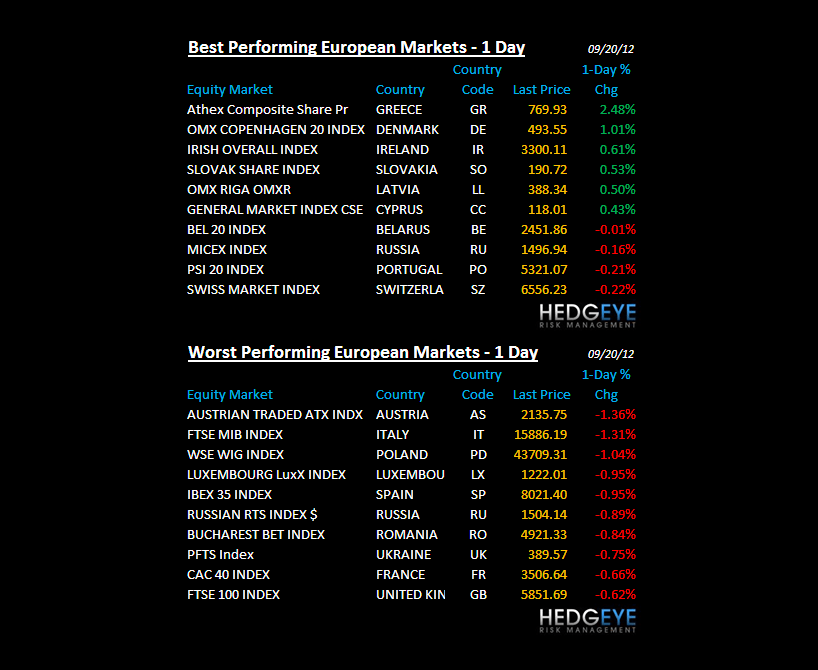

EUROPEAN MARKETS

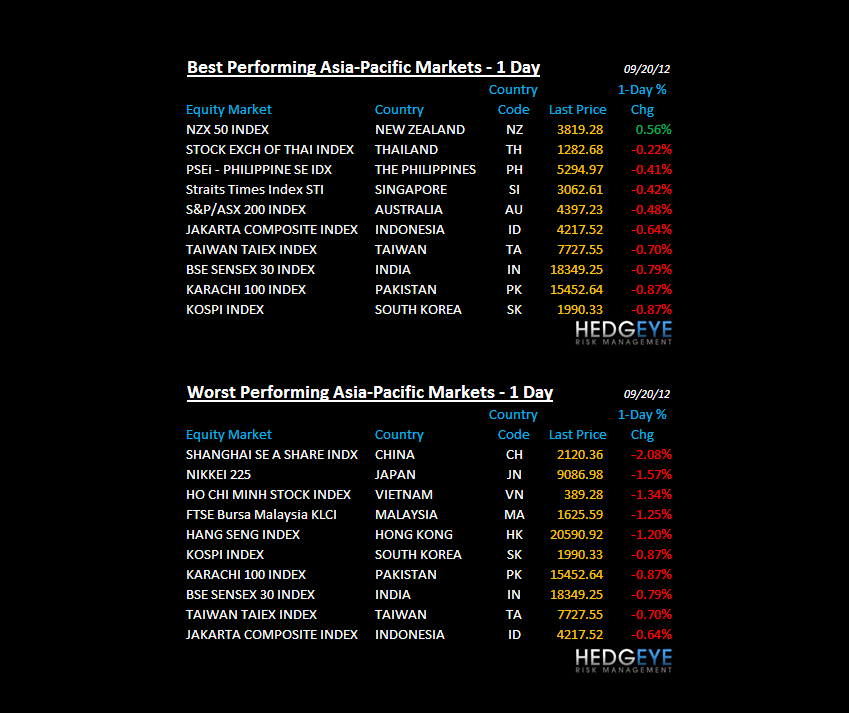

ASIAN MARKETS

CHINA – never mind what NSC surprised people with (bulk commodity volumes slowing), Chinese stocks have been pounding this into our craws since May (Qe commodity inflation is not demand); Shanghai Comp -2.1% last night to a fresh YTD low (-18% since May); Japan’s attempt to play the Bernanke card was good for a 1-day rally, then Nikkei straight back down -1.6%.

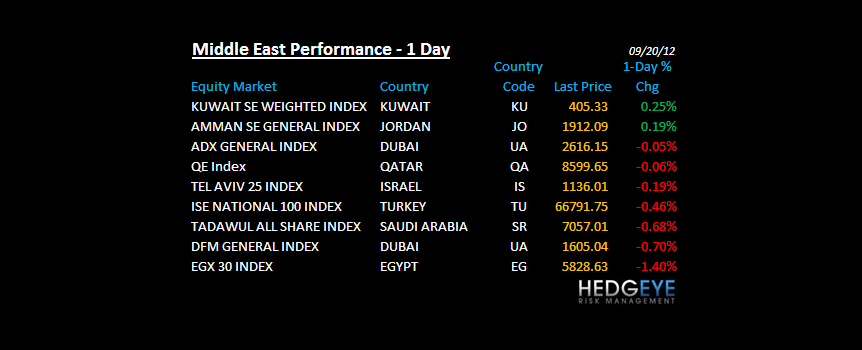

MIDDLE EAST

The Hedgeye Macro Team