-- For specific questions on anything Europe, please contact me at to set up a call.

Positions in Europe: Long German Bonds (BUNL); Short EUR/USD (FXE)

Asset Class Performance:

- Equities: The STOXX Europe 600 closed up +1.3% week-over-week vs +2.3% last week. Top performers: Cyprus +17.8%; Russia (RTSI) +7.4%; Greece +7.1%; Ukraine +7.0%; Hungary +4.8%; Finland +4.7%; Austria +4.3%; Sweden +4.1%; Poland +3.7%. Bottom performers: Denmark -1.6%; Slovakia -1.5%; Estonia -0.7%. [Other: France +1.8%; UK +2.1%; Germany +2.7%].

- FX: The EUR/USD is up +2.37% week-over-week. W/W Divergences: RUB/EUR +1.50%; HUF/EUR +1.14%; PLN/EUR +0.81%; CZK/EUR +0.79%; DKK/EUR -0.06%; CHF/EUR -0.48%; GBP/EUR -0.98%; NOK/EUR -1.67%; SEK/EUR -1.78%; TRY/EUR -2.15%.

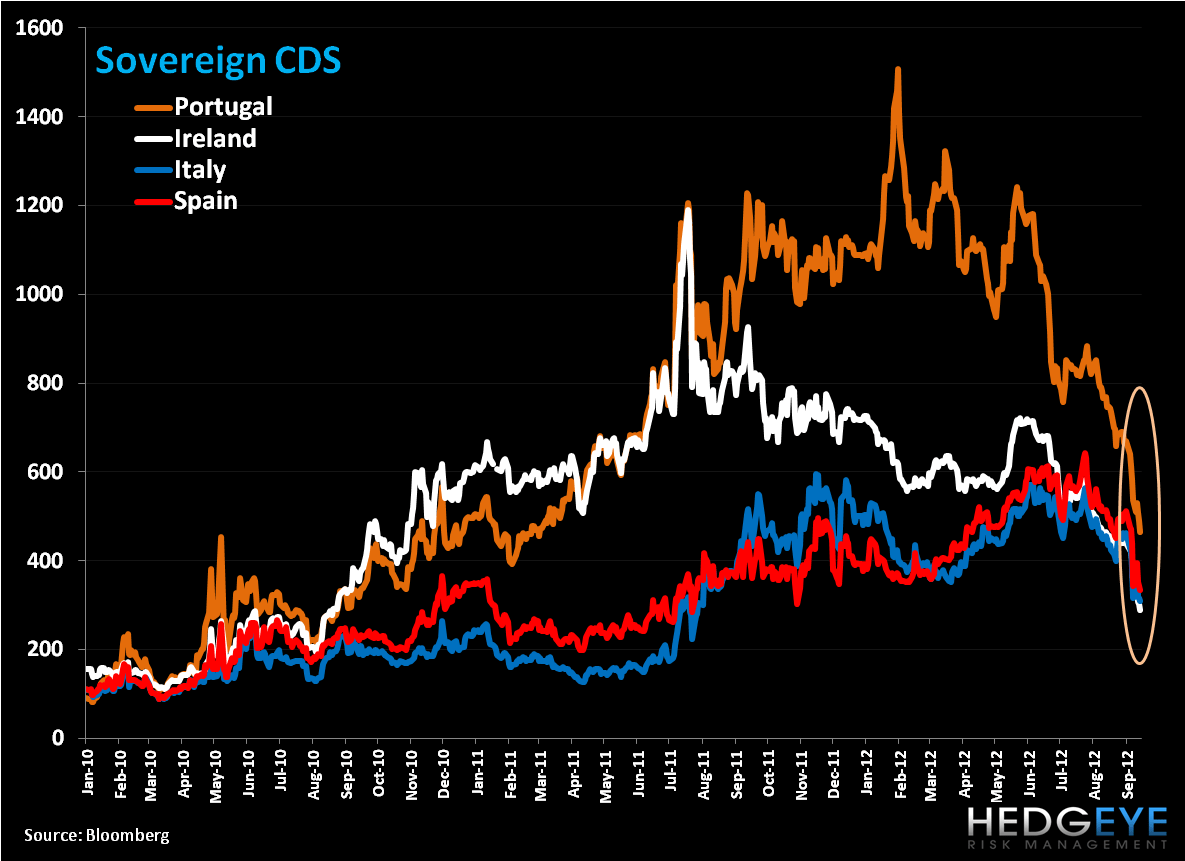

- Sovereign CDS: Sovereign CDS followed yields with all main countries we track down on the week. On a week-over-week basis Portugal fell the most, down -72bps to 464bps, followed by Italy -148bps to 315bps, Portugal -133bps to 536bps, Ireland -97bps to 343bps, and France -25bps to 115bps.

- Fixed Income: The 10YR yield for sovereigns fell dramatically across the board for peripheral countries, while the core gained on the week, for a second straight week. Greece saw the largest decline, -83bps to 20.79%, followed by Portugal’s -16bps move to 8.09%; Italy fell -15bps to 4.97% and Spain dropped -11bps to 5.64%. Germany was up +8bps to 1.70% and France gained +2bps to 2.26%.

Central Bankers Make Waves

The last two weeks of market trading have been dominated by the policy moves of Draghi and Bernanke. Period. Draghi’s “unlimited” bond purchasing program, named Outright Monetary Transactions (OMTs), and Bernanke’s further monetizing of MBS and push of the zero interest rate bound out to 2015 have stoked most global markets and the EUR (see price moves above), irrespective of the underlying fundamentals.

Specific to Europe, Germany’s Constitutional Court decision on Wednesday to uphold the ruling on the ESM and fiscal union added a further boost to capital markets, however we remain very cautious on the underlying weakness of these regional economies, and firm in our belief that a transition, if it is possible at all, to a united Europe (or at least Eurozone) under a monetary and fiscal union, is a long, challenging road.

A few broader challenges that stand in the way of a fiscal union are:

- The unevenness of economies.

- The strong cultural differences (namely language) that prevent frictionless labor moment.

- The inability of states to willingly give up their fiscal sovereignty to Brussels or Frankfurt. Example: this week Spanish PM Rajoy, in response to talk about his country taking bailout monies said: “I will look at the conditions. I would not like, and I could not accept, being told which were the concrete policies where we had to cut.”

This week there was much talk about the formation of a European banking union. The European Commission (EC) delivered its proposal on a “single supervisory mechanism” of all banks in the Eurozone supervised by the ECB. Importantly, Germany is reluctant to cede control of its banking sector and wants the new regulator to concentrate only on the region's biggest banks, perhaps an estimated 20-25 banks.

While Germany's private-sector banks, including Deutsche Bank, have embraced the commission's proposal, the country's public-sector banks oppose it, saying their lower-risk business models should allow them to avoid the new layer of pan-European supervision. Certainly creating an FDIC of the Eurozone is an important step in the path to a fiscal union, however we see challenges arising from striping existing national supervisors to a new ECB supervisory board.

Taken together, we are fully aware of the powers of Central Bankers to drive markets. That said, the fundamental data keeps us grounded in our opinion that despite best efforts from Eurocrats to craft rescue programs, we think the structural flaws inherent in creating a Eurozone will continue to present challenges that should negatively impact markets; we expect the biggest challenge to be a protracted period of slow growth that misses expectations as Europe works through the debt trap it has amassed over the last ten years. Finally, in the near term, the impact of high commodity prices as well as sticky to rising inflation (broadly), will add further negative economic pressures.

Call Outs:

France - The French 2013 budget is to be introduced on September 28th. French Finance Minister Pierre Moscovici said that it needs to find €30-€35B in additional revenue from spending cuts. It plans to seek as much as €20B from new taxes (including the 75% on annual income over €1M, which President Hollande said this weekend could be dropped after around two years in place) and €10B from spending cuts to meet its pledge of reducing the budget to 3% of GDP next from a projected 4.5% in 2012. He also said that the government expects GDP to be 0.8% in 2013, down from its earlier forecast of 1.2%.

Portugal - Troika agreed to ease Portugal’s deficit goal from 4.5% to 5% of GDP this year.

Italy - Prime Minister Monti hinting that he would be open to remaining in his position after elections next year.

Eurozone Banks - JPM sees another 15% upside in the group.

Netherlands - The Liberal Party of caretaker Prime Minister Mark Rutte was headed to victory in the Dutch parliamentary vote. The Liberals took 41 of the 150 seats (up from the 31 in the last vote in 2010); the Labor Party of Diederik Samsom won 40 seats (up from 30); D66 rose to 12 from 10; the Christian Democrats lost eight seats to 13; and Geert Wilders’ anti-immigrant Freedom Party lost 11 seats to 13. It appears likely Rutte, with the strongest international profile, will remain premier.

Spain - Cinco Dias, citing unidentified sources at the Budget Ministry, reported in its Wednesday Internet edition that the Spanish government is planning to increase the tax rate on short-term capital gains to as much as 52% in 2013. The paper pointed out that the highest tax rate on short-term capital gains currently stands at 27%. It added that move is intended to boost tax revenues and dampen market speculation and volatility.

EUR/USD:

Our immediate term TRADE range for the cross is $1.27 to $1.30. In the second chart below we look at CFTC data for net contracts of Euro non-commercial positions. Interestingly, since a high in short position in the Euro on 6/5/12 (-213.060 contracts), investors have been less bearish (and covering). Week over week, contracts are 10% less bearish, -95,080 as of the most recently reported data on 9/11 versus -105,433 as of 9/4.

Data Dump:

Eurozone Sentix Investor Confidence -23.2 SEPT vs -30.3 AUG

Eurozone Industrial Production -2.3% JUL Y/Y vs -2.1% JUN

Eurozone CPI 2.6% AUG Y/Y vs 2.6% JUL [0.4% AUG M/M vs -0.5% JUL]

Germany CPI Final 2.2% AUG Y/Y (UNCH)

Germany Wholesale Price Index 3.1% AUG Y/Y vs 2.0% JUL [1.1% AUG M/M vs 0.3% JUL]

UK ILO Unemployment Rate 8.1% JUL vs 8.0% JUN

UK Jobless Claims Change -15.0K AUG vs -13.6K JUL

France CPI 2.4% AUG Y/Y vs 2.2% JUL

France Q2 total payrolls -0.1% Q/Q (exp. -0.1%) vs -0.1% in Q1

Bank of France Business Sentiment 93 AUG vs 90 JUL

France Industrial Production -3.1% JUL Y/Y (exp. -3.7%) vs -2.5% JUN

France Manufacturing Production -2.8% JUL Y/Y (exp. -4.2%) vs -2.9% JUN

Italy Q2 GDP Final -0.8% Q/Q (exp. -0.7%) vs -0.7% initial [-2.6% Y/Y (exp. -2.55) vs -2.5% initial]

Italy Industrial Production -7.3% JUL Y/Y vs -7.9% JUN

Italy CPI Final 3.3% AUG Y/Y (initial 3.5%) vs 3.6% JUL

Spain CPI Final 2.7% AUG Y/Y (UNCH)

Spain House Transactions -2.5% JUL Y/Y vs -11.4% JUN

Spain House Prices -14.4% Y/Y in Q2 vs -12.6% in Q1

Portugal CPI 3.2% AUG Y/Y vs 2.8% JUL

Switzerland Producer & Import Prices -0.1% AUG Y/Y vs -1.8% JUL

Austria CPI 2.2% AUG Y/Y vs 2.1% JUL

Netherland Retail Sales -4.0% JUL Y/Y vs 1.0% JUN

Denmark CPI 2.6% AUG Y/Y vs 2.1% JUL

Norway CPI 0.5% AUG Y/Y vs 0.2% JUL

Finland CPI 2.7% AUG Y/Y vs 2.9% JUL

Sweden Q2 GDP Final 1.3% Y/Y (initial 2.3%) vs 1.3% in Q1

Sweden Unemployment Rate SA 7.8% AUG vs 7.5% JUL

Sweden CPI 0.7% AUG Y/Y vs 0.7% JUL

Sweden PES Unemployment Rate 4.8% AUG vs 4.6% JUL

Sweden Industrial Production -0.4% JUL Y/Y vs 1.2% JUN

Ireland CPI 2.6% AUG Y/Y vs 2.0% JUL

Ireland New Vehicle Licenses 5341 AUG vs 7944 JUL

Greece CPI 1.2% AUG Y/Y vs 0.9% JUL

Greece Unemployment Rate 23.6% in Q2 vs 22.6% in Q1

Poland CPI 3.8% AUG Y/Y (exp. 3.8%) vs 4.0% JUL

Czech Republic CPI 3.3% AUG Y/Y vs 3.1% JUL

Czech Republic Unemployment Rate 8.3% AUG vs 8.3% JUL

Estonia Exports 12% JUL Y/Y vs 8% JUN

Estonia Imports 14% JUL Y/Y vs 14% JUN

Hungary CPI 6.0% AUG Y/Y vs 5.8% JUL

Romania CPI 3.9% AUG Y/Y vs 3.0% JUL

Romania Industrial Output 1.9% JUL Y/Y vs 1.4% JUN

Slovakia CPI 3.7% AUG Y/Y vs 3.7% JUL

Turkey Q2 GDP 1.8% Q/Q vs -0.1% in Q1 [2.9% Y/Y vs 3.3% in Q1]

Turkey Industrial Production 3.4% JUL Y/Y vs 3.1% JUN

Interest Rate Decisions:

(9/13) Switzerland SNB 3M Libor Target Rate UNCH at 0.00%

(9/13) Latvia Refinancing Rate CUT 25bps to 2.50%

The European Week Ahead

Sunday: Sep. UK Rightmove House Prices

Monday: Jul. Eurozone Current Account, Trade Balance; 2Q Eurozone Labour Costs; Jul. Italy Trade Balance

Tuesday: Sep. Eurozone ZEW Survey Economic Sentiment; Aug. Eurozone New Car Registrations; Sep. Germany ZEW Survey Current Situation and Economic Sentiment; Jul. UK ONS House Price; Aug. UK CPI, Retail Price; Jul. Greece Current Account

Wednesday: Jul. Eurozone Construction Output; BoE Minutes

Thursday: Sep. Eurozone Consumer Confidence – Advance, PMI Composite, Manufacturing and Services; Sep. Germany PMI Manufacturing and Services - Advance; Aug. Germany Producer Prices; Sep. UK CBI Trends Total Orders, CBI Trends Selling Prices; Aug. UK Retail Sales; Sep. France PMI Manufacturing and Services – Preliminary; Jul. Italy Industrial Orders and Sales

Friday: Aug. UK Public Sector Net Borrowing, Public Sector Finances; 2Q France Wages – Final; Jul. Spain Mortgages-Capital Loaned, Mortgages on Houses, Trade Balances

Matthew Hedrick

Senior Analyst