TODAY’S S&P 500 SET-UP – September 14, 2012

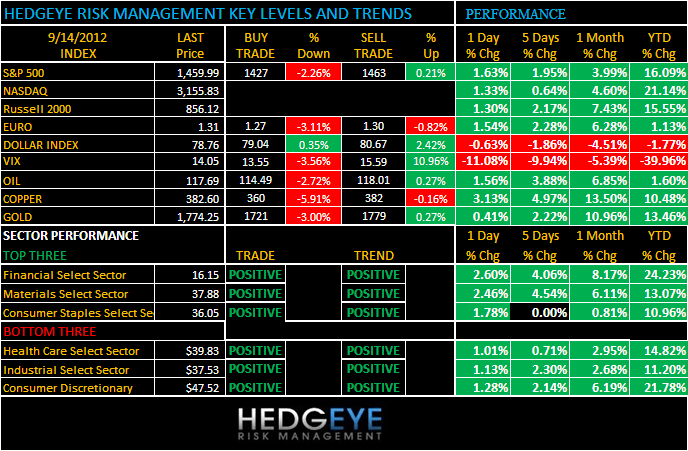

As we look at today’s set up for the S&P 500, the range is 36 points or -2.26% downside to 1427 and 0.21% upside to 1463.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 09/13 NYSE 1701

- Increase versus the prior day’s trading of 778

- VOLUME: on 09/13 NYSE 802.31

- Increase versus prior day’s trading of 20.86%

- VIX: as of 09/13 was at 14.05

- Decrease versus most recent day’s trading of -11.08%

- Year-to-date decrease of -39.96%

- SPX PUT/CALL RATIO: as of 09/13 closed at 1.11

- Down from the day prior at 1.12

CREDIT/ECONOMIC MARKET LOOK:

Qe USA – never, in US economic history, has a > $4 national avg at the pump NOT slowed US economic growth; never is a long time; see our Qe note from yesterday showing you the 3 most powerful ramps in gas prices and what the US economy immediately did next (mid-2008, mid-2011, and Q1 of 2012). Its only not obvious to the willfully blind.

- TED SPREAD: as of this morning 29.21

- 3-MONTH T-BILL YIELD: as of this morning 0.09%

- 10-Year: as of this morning 1.81%

- Increase from prior day’s trading of 1.72%

- YIELD CURVE: as of this morning 1.58

- Up from prior day’s trading at 1.49

MACRO DATA POINTS (Bloomberg Estimates)

- 8:30am: Consumer Price Index M/m, Aug., est. 0.6% (prior 0.0%)

- 8:30am: Advance Retail Sales, Aug. est. 0.8% (prior 0.8%)

- 9:15am: Industrial Production, Aug., est. -0.1% (prior 0.6%)

- 9:15am: Capacity Utilization, Aug., est. 79.2% (prior 79.3%)

- 9:55am: University of Michigan Consumer Sentiment, Sept. preliminary, est. 74.0 (prior 74.3)

- 10am: Business Inventories, July, est. -0.3% (prior 0.1%)

- 11am: Fed to buy $1.5b-$2b notes due 2/15/2036-8/15/2042

- 1pm: Baker Hughes rig count

- 1pm: Fed’s Lockhart at employment conference in Atlanta

- 1:45pm Fed’s Raskin speaks in Michigan on economy

GOVERNMENT:

- Washington Day Ahead agenda

- SEC holds a public hearing on ways to promote stability in markets reliant on highly automated trading systems; will focus on how market participants design, implement and manage trading technology after glitches disrupted Facebook’s initial public offering and pushed Knight Capital to brink of bankruptcy, 10am

- ITC Judge releases findings in patent-infringement case that Samsung filed against Apple over smartphone features and ways to transmit data, after 9am

- Treasury Undersecretary for Domestic Finance Mary Miller speaks at American Banker conference. Arlington, Va. 2:15pm

- Transportation Secretary Ray Lahood, FTA Administrator Peter Rogoff make transit funding announcement, 12:30pm

- Congressional Robotics Caucus holds briefing on National Robotics Initiative, 12:30pm

- House, Senate in session

WHAT TO WATCH:

- Germany’s Schaeuble cautions Spain against a full bailout

- U.S. retail sales probably improved in Aug. on auto demand

- Western Digital cuts rev. view, begins div. and $1.5b buyback

- Peregrine’s Wasendorf released on bails after guilty plea

- Visteon said to consider Leuliette as CEO while eyeing electronics unit

- Time CEO Lang seeks to unify web and print advertising

- Japan tells China to withdraw ships near disputed islands

- Italian 10y yields fall below 5% for first time since March

- California Attorney General investigates doctor-hospital deals: WSJ

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Corn Bulls Retreat as Near-Record Costs Curb Demand: Commodities

- Beef Premium Spurring Demand for Cheaper Pork: Chart of the Day

- Oil Rises to $100 for First Time Since May After Fed Stimulus

- Commodities Post Longest Rally Since 2010 as Fed Boosts Outlook

- Platinum Heads for Longest Winning Run in 25 Years; Gold Rallies

- Aluminum Heads for the Longest Rally in at Least 25 Years

- Wheat Rises on Egyptian Purchase of French Grain, U.S. Drought

- Coffee Headed for Longest Rally in Four Months; Cocoa Advances

- Japan Draws Curtain on Nuclear Energy Following Germany: Energy

- Rebar in Shanghai Gains to Three-Week High on Fed Stimulus Plan

- Aluminum Backwardation Looms as Warehouse Backlog Limits Supply

- Pemex’s Missing Oil Surges to All-Time High: Chart of the Day

- Oil May Fall on Projected Supply Gain After Isaac, Survey Shows

- Sugar Bulls Ascend as Rain Returning to Top Producer Brazil

- Copper Jumps, Heads for Highest Close Since May on Fed Stimulus

- Storm Effect on Oil Prices Waning as Shale Booms: Energy Markets

CURRENCIES

EUROPEAN MARKETS

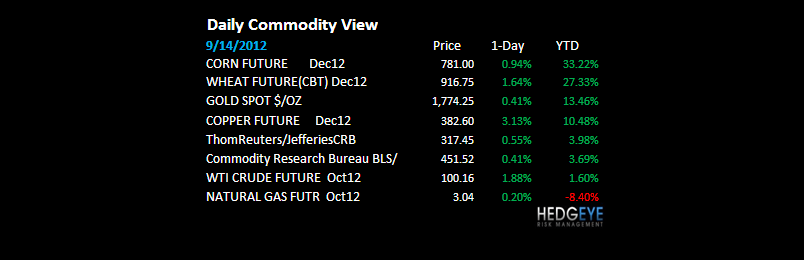

Qe EUROPE – ok, when you have economic stagflation (zero to negative growth + inflation), what you really need (if you have a growth problem) is another rip in food/energy prices; that’ll get things fixed! $117.35 Brent Oil last, +33% since June.

ASIAN MARKETS

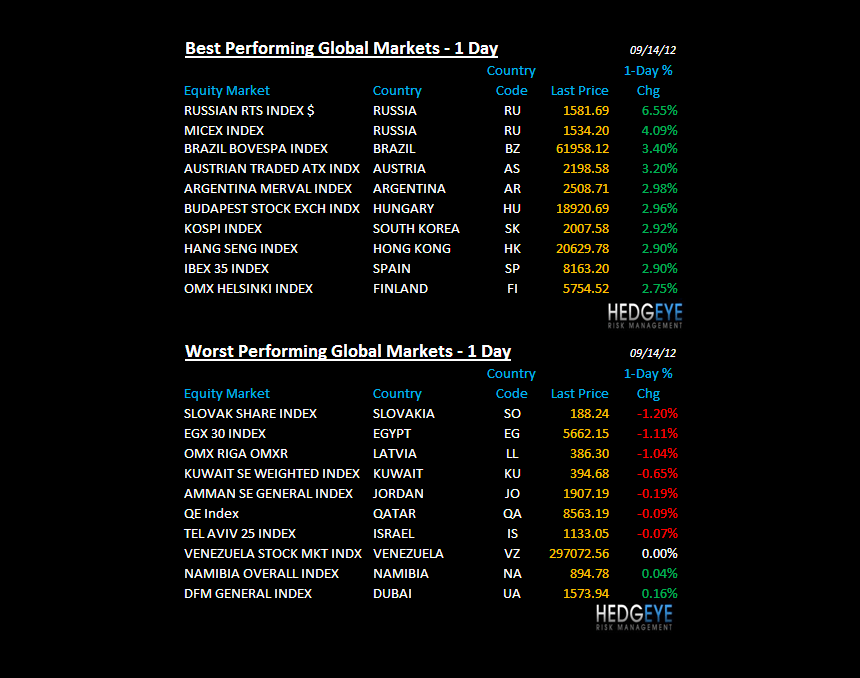

Qe ASIA – straight up moves in the KOSPI +3.2%, Hang Seng +2.9%, and Nikkei +1.8%, but all to lower-highs vs Feb-March; no idea how the math works on commodity demand slowing as prices are rising for Asian export producers; Bernanke doesn’t care.

MIDDLE EAST

The Hedgeye Macro Team